Are soaring AI ambitions turning Meta Earnings into a long-term jackpot or a costly misstep that Wall Street is suddenly doubting?

How did Meta Earnings land versus expectations?

In its most recent quarterly update, Meta Earnings comfortably cleared analyst estimates on both revenue and earnings per share. Sales climbed to roughly $56 billion, up about 33% year over year, while net income surged into the mid‑$20 billion range. Operating margins compressed modestly as AI‑related costs accelerated, but overall profitability remained robust enough that Meta continues to generate tens of billions in annual earnings and to fund both a dividend and buybacks.

Daily active people across Facebook, Instagram, WhatsApp and Messenger came in at 3.56 billion, a tiny sequential dip that management linked to WhatsApp restrictions in Russia and internet outages in Iran rather than weakening engagement. Revenue per user continues to benefit from better ad targeting, recommendation algorithms and higher time spent. For now, the ad engine that underpins Meta Earnings is not the problem; it is strong enough that several analysts still see the stock as undervalued on roughly 20x forward earnings.

Why are AI capex plans spooking investors?

The controversy around the latest Meta Earnings centers squarely on spending. Management lifted its full‑year capital expenditure outlook to $125–$145 billion, up from an already aggressive $115–$135 billion range. CFO Susan Lee pointed to higher component and storage costs and expanded data‑center build‑outs as key drivers, as Meta races to build out GPU clusters, networking and power for next‑generation AI models and “personal superintelligence” agents.

This hyperscale budget puts Meta in the same spending league as cloud giants like NVIDIA customers, Alphabet and Amazon, despite Meta lacking a stand‑alone cloud platform to monetize AI capacity. Some skeptics argue Meta is acting like a cloud provider without the same direct revenue channels, effectively pushing most of its free cash flow into long‑duration, uncertain payoffs. Others note that Meta recently raised $25 billion in investment‑grade bonds across six tranches, underlining how capital‑intensive its AI roadmap has become.

What is the strategy behind Meta’s AI push?

Management insists the AI wave is already helping Meta Earnings, even if the full upside is still ahead. CEO Mark Zuckerberg highlighted how AI‑driven recommendations are boosting engagement on Reels and the main Facebook and Instagram feeds, which in turn lifts ad inventory and pricing. The new Muse Spark model, developed in Meta’s superintelligence lab, now powers Meta AI features inside its apps and has already driven higher usage.

Strategically, Meta wants to embed AI agents across its social graph: consumer assistants inside messaging apps, tools for creators, and business agents that can automate customer support and commerce. Zuckerberg also emphasized that Meta is not prioritizing coding agents in the same way some competitors are, arguing that simply generating code is only one component of model self‑improvement. At the same time, the company is trimming headcount—about 8,000 jobs, or 10% of the workforce—to offset part of the AI investment ramp and to redeploy talent from legacy and metaverse projects toward AI infrastructure and models.

How does Meta stack up against rivals?

For US investors comparing Big Tech names, the latest Meta Earnings highlight a key divergence. Alphabet and Amazon are showing clearer, faster monetization of AI through their cloud businesses, where every new AI workload directly drives infrastructure revenue. Microsoft is following a similar playbook with Azure and its Copilot ecosystem. By contrast, Meta’s AI spending is funneled primarily into better ads and user experiences, benefits that are more diffuse and harder to measure quarter to quarter.

This gap in perceived visibility is starting to matter for relative performance on the NASDAQ and within the S&P 500. JPMorgan Chase & Co. downgraded Meta from “overweight” to “neutral” with a $725 price objective, citing limited visibility into the AI product pipeline and big spending commitments with uncertain near‑term payback. On the other hand, Royal Bank of Canada reiterated an “outperform” rating and set an $810 target, while KeyCorp kept an “overweight” call with a $760 target, arguing that Meta has earned the right to invest aggressively as long as advertising growth stays north of 20–30%.

What do Meta Earnings mean for the stock now?

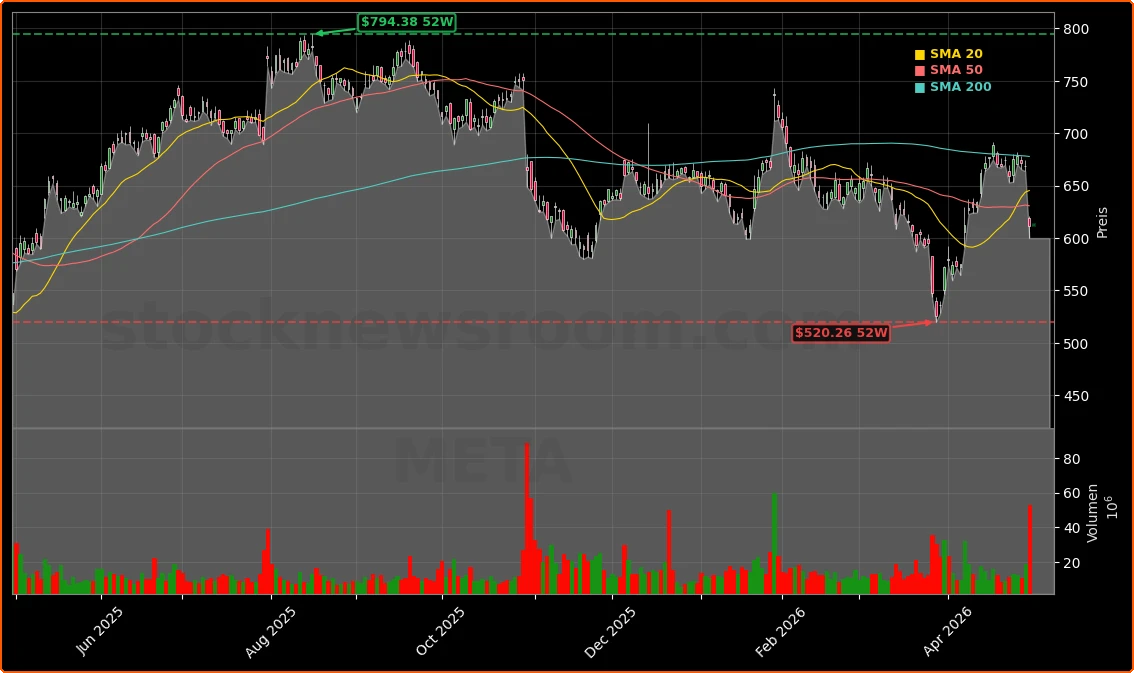

Meta shares recently dropped almost 9% in the wake of these Meta Earnings and the expanded capex guidance, and they now trade near $611.91, roughly flat in early pre‑market action and hovering around a technical support zone near $600. Some traders view this area as a potential bounce level but note that the name no longer trades like a pure momentum play as it did during earlier AI rallies. The stock is also lagging some AI hardware and infrastructure winners: chip suppliers like NVIDIA and Broadcom and ecosystem names such as Apple are perceived to be capturing near‑term AI dollars more directly.

Long‑only portfolio managers now face a familiar Big Tech trade‑off. Owning Meta means accepting a period where free cash flow is intentionally suppressed to fund a multiyear AI build‑out, with the payoff largely tied to improved ad economics, new consumer AI products and potentially business agents that do not yet exist at scale. For diversified US investors, that makes position sizing and time horizon critical: Meta looks inexpensive on earnings today, but those Meta Earnings will be reinvested heavily rather than returned to shareholders in the near term.

Related Coverage

For a deeper dive into the same quarter, including a detailed breakdown of the revenue beat and the immediate market reaction to the AI spending shock, readers can review Meta Earnings Q1: Revenue Record but AI Capex Shock. That analysis focuses on how the record top line collided with fresh concerns about free cash flow, and how options markets priced in the post‑report volatility.

We’re seeing more and more examples where one or two people can do in a week what used to take dozens of people months.— Mark Zuckerberg, CEO of Meta Platforms

In sum, Meta Earnings underscore a company firing on all cylinders operationally while deliberately trading current cash for future AI dominance. For US investors, the key question is whether they share Zuckerberg’s conviction that today’s $125–$145 billion capex bill will translate into a stronger, more defensible profit stream later in the decade. The next few quarters will show whether ad growth and early AI products can keep justifying that bet as Wall Street’s patience is tested.