Can Meta Earnings convince investors that record AI spending and fresh layoffs will ultimately boost long-term profits instead of crushing margins?

Can Meta Earnings justify record AI capex?

The near‑term debate around Meta Earnings centers on how much profit pressure investors are willing to tolerate as the company retools its infrastructure for an AI‑heavy future. Management has signaled capital expenditures of roughly $115 billion to $135 billion in 2026, up sharply from about $72.2 billion in 2025 when including lease payments. That step‑up is driven by data centers, custom Meta Training and Inference Accelerator (MTIA) chips, and partnerships with cloud players like Amazon Web Services and component suppliers such as Corning.

In its last reported quarter, Meta posted revenue of $59.9 billion, up 24% year over year, and guided Q1 sales to a range of $53.5 billion to $56.5 billion. The midpoint implies around 30% growth and still roughly 26% growth after adjusting for foreign‑exchange tailwinds. Daily active users reached 3.58 billion in December, rising 7% year over year, underscoring the scale of Facebook, Instagram, WhatsApp, Messenger and Threads as ad platforms.

Yet free cash flow is already feeling the strain. Street forecasts point to around $4 billion of Q1 free cash flow, the weakest in nearly four years, as AI and data‑center investments accelerate. For many portfolio managers, the core Meta Earnings question is whether management can prove that this capex surge will translate into sustainably higher earnings power rather than just lower margins.

How is Meta Platforms balancing jobs and margins?

To offset the impact of record investment, Meta has launched another efficiency drive. Reports indicate the company plans to cut about 10% of its workforce—roughly 8,000 employees—and close around 6,000 open roles. That follows earlier cost‑cutting that turned 2023 and 2025 into “years of efficiency” for the company.

CEO Mark Zuckerberg is positioning these layoffs as a way to keep operating expenses in check without derailing the AI roadmap. Management has told investors it still expects 2026 operating income to be above 2025 levels despite the capex surge. If the upcoming Meta Earnings release shows that operating margins are holding up better than feared, the market may read the job cuts as evidence of discipline rather than distress.

Analysts have generally treated the workforce reductions as a net positive for the equity story. Recent commentary from Wall Street desks framed the layoffs as an attempt to protect profitability while redirecting resources toward AI and data‑center build‑outs. That narrative helped support the stock’s rally earlier this month even as headlines about job losses temporarily weighed on tech sentiment.

What do Meta Earnings mean for AI rivals?

Meta’s aggressive infrastructure plan ripples across the broader AI and mega‑cap landscape. The company is a core member of the “Magnificent Seven” alongside NVIDIA, Tesla, Apple, Microsoft and Alphabet, a group that has driven much of the NASDAQ and S&P 500’s rebound since late March. Shares of Meta are now up more than 25% from the S&P 500’s March 30 low, putting fresh pressure on laggard names and on investors who are underweight big tech.

At the same time, Meta is deepening ties with hardware and utilities suppliers. Corning has signed a multi‑year, multi‑billion‑dollar agreement to provide fiber‑optic and AI data‑center solutions, helping power the next wave of Meta’s infrastructure. Vistra has locked in a 20‑year nuclear‑energy supply deal that should deliver clean power for the company’s expanding data‑center footprint. These arrangements give Meta some visibility into long‑term capacity and energy costs, but they also underscore how capital‑intensive its AI ambitions have become.

Competitively, Meta is battling Alphabet and Amazon in both digital ads and AI platforms. Google’s recent move to commit up to $40 billion to Anthropic is a clear shot at narrowing perceived AI gaps and defending Google Cloud as Meta’s ad growth accelerates. Amazon is partnering with Meta on AI systems processors through AWS, tying the fortunes of two major NASDAQ components together as they ramp data‑center silicon.

How expensive is Meta stock into Meta Earnings?

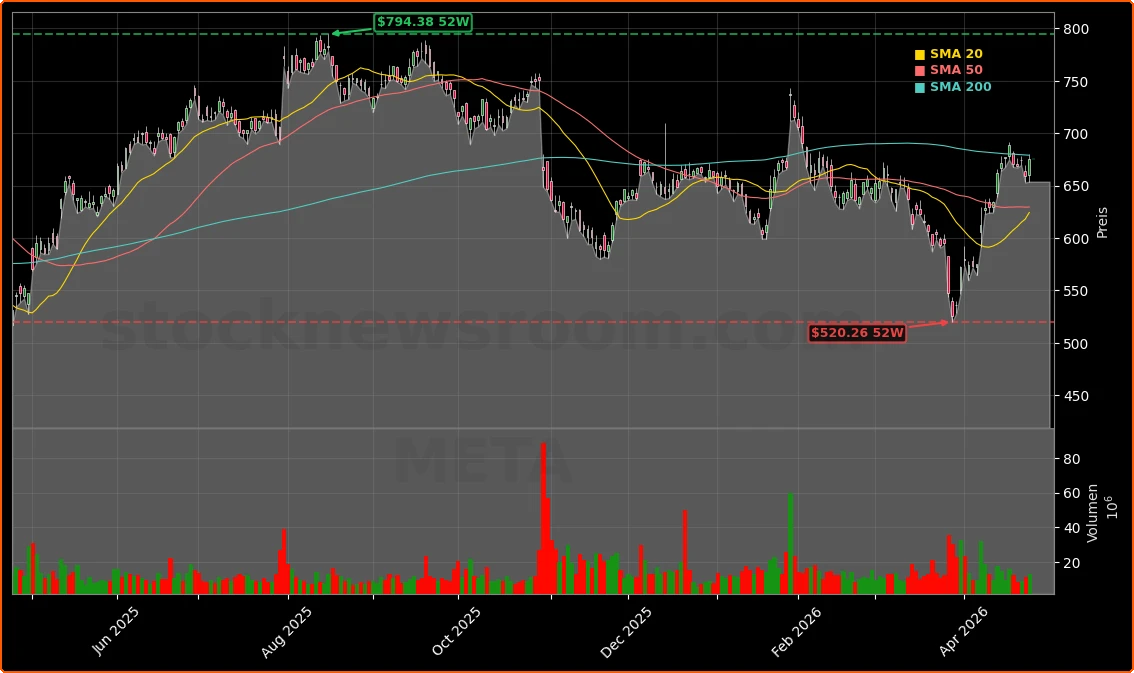

At about $675 per share, Meta trades near 29 times trailing earnings, a premium multiple for a social‑media‑anchored business but less stretched for a platform growing revenue north of 20% annually. Some institutional investors estimate a more normalized 2025 earnings base around $29 per share, adjusting for one‑off tax charges rather than the reported $23.49. If Meta can compound that base at 15% to 18% annually over the next five years, earnings per share could land between $58 and $66, implying potential stock prices above $1,100 at a 20x multiple.

Even bullish forecasts, however, hinge on Meta Earnings demonstrating that AI investments are already improving monetization. Management has pointed to better ad targeting, higher engagement and new automation tools like Meta Advantage+ as examples of AI‑driven gains. For now, most of Meta’s AI payoff is still flowing through its core advertising engine rather than new standalone AI products, which leaves the company exposed to cyclical ad spending and ongoing regulatory scrutiny.

Related Coverage

We are now seeing a major AI acceleration. Our vision is building personal superintelligence.— Mark Zuckerberg, CEO of Meta Platforms

For a deeper dive into how job cuts fit into the investment story, readers can explore our analysis of Meta layoffs and record AI spending, which examines whether the latest efficiency push is a smart reset or a warning sign for future growth. Together with the upcoming Meta Earnings report, these developments will shape how investors recalibrate expectations for profits, capex and long‑term returns.