Can Meta’s latest round of global layoffs really finance its massive AI ambitions without breaking investor confidence in the stock?

How do Meta Platforms Layoffs hit the stock today?

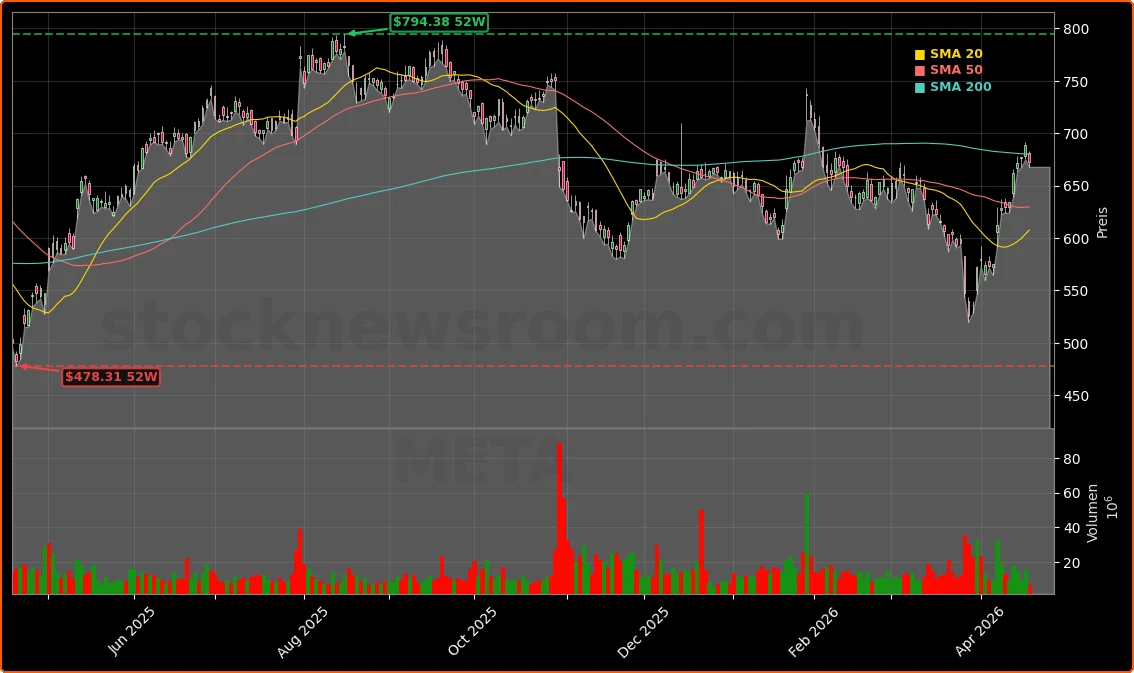

Meta (META) traded lower on Monday, recently changing hands around $672.62, down about 2.3% from Friday’s close of $686.80. The pullback comes as investors digest fresh reports that the company will eliminate around 10% of jobs worldwide by late May and pursue further cuts later this year. After a powerful rally in 2025 and early 2026, the stock remains one of the most closely watched names on the NASDAQ and in the S&P 500’s technology cohort.

The latest Meta Platforms Layoffs arrive against a backdrop of record capital expenditures on AI. Management has already signaled sharply higher spending to expand data centers, secure long-term energy supply and deploy the Meta Training and Inference Accelerator (MTIA), its in-house AI chip. While the stock still trades at a forward P/E near the low 20s, below its historical average, investors are increasingly sensitive to any sign that AI spending might erode operating margins in 2026–2027.

Why is Meta doubling down on AI now?

The primary rationale behind the Meta Platforms Layoffs is to fund an aggressive AI buildout without losing discipline on profitability. Meta is racing alongside hyperscale peers like Alphabet, Microsoft and Amazon to train larger models, improve recommendation engines and deliver generative AI tools to billions of users. Its AI-powered Advantage+ ad platform is already lifting performance, helping drive a 22% year-over-year increase in advertising revenue to about $196 billion in 2025.

For Q1 2026, Meta has guided to revenue between $53.5 billion and $56.5 billion, ahead of Wall Street’s current consensus. Bank of America recently trimmed its price target to $820, but still expects a strong quarter with earnings per share potentially around $7.44 versus prior estimates near $6.64 and revenue of roughly $56 billion. That optimism rests on the assumption that AI-driven engagement and better ad targeting can more than compensate for higher depreciation and energy costs tied to new infrastructure.

At the same time, Meta is working to reduce its dependence on NVIDIA by ramping MTIA deployments and broadening its relationships with chipmakers like AMD and Broadcom. Recent industry data shows AMD gaining share in AI accelerators thanks in part to multi-year deals with Meta and Alphabet, a trend also highlighted by bullish commentary from Wolfe Research on AMD’s data center outlook.

What do job cuts mean for Meta’s cost structure?

Meta Platforms Layoffs of roughly 8,000 employees globally would mark one of the largest headcount reductions among mega-cap tech firms this year. The company previously cut tens of thousands of roles in 2023, but the new round is more explicitly tied to freeing up room for AI-related capex rather than simply reversing pandemic-era overhiring. Severance charges will weigh on near-term results, but Wall Street will be focused on the run-rate savings flowing into 2027.

Meta’s AI strategy is capital- and energy-intensive. The company has been signing long-term power purchase agreements to secure reliable, often low-carbon electricity for its data centers, including interest in nuclear and natural-gas baseload to keep AI clusters running 24/7. These commitments, plus heavy investment in global fiber networks, mirror similar moves by Microsoft and Alphabet, but they magnify the importance of leaner operating expenses elsewhere in the business.

From an investor perspective, the key risk is execution: if layoffs disrupt product development or moderation, user experience and ad performance could suffer. So far, however, Meta’s scale advantage — with more than 3 billion daily active users across its family of apps — has allowed it to streamline back-office roles while continuing to ship new AI features on Facebook, Instagram, WhatsApp and the Quest ecosystem.

How does Meta stack up against rivals like Alphabet and Apple?

In the mega-cap AI race, Meta’s latest cuts underline how far the company is willing to go to defend its position. Alphabet continues to invest heavily in its own AI models and custom chips, while also deepening cloud partnerships with major customers. In 2026 comparisons of Alphabet versus Meta, some analysts argue that Meta offers the more attractive entry point on valuation, especially after factoring in the impact of Meta Platforms Layoffs on future margins.

Competition is also heating up in hardware. In smart glasses and AR/VR, Meta currently dominates many Western markets through its Quest platform and Ray-Ban Meta smart glasses. But Chinese players and US rivals are closing in. Huawei has just launched AI-powered glasses in China, and Apple is reportedly testing multiple designs for its own AI smart glasses, targeting a premium launch around 2027. These moves could chip away at Meta’s early hardware lead and force even more R&D spending just as the company is tightening headcount.

Beyond consumer devices, Meta faces intense competition for AI compute. Google is preparing new inference chips and expanding deals with AI developers and partners like Meta itself, attempting to challenge NVIDIA’s dominance. Chip suppliers such as AMD and Broadcom are enjoying surging demand as Meta, Alphabet and others lock in multi-year supply for next-generation accelerators.

Is the broader tech layoff wave intensifying?

The Meta Platforms Layoffs are part of a wider reset across big tech. More than 73,000 tech jobs were cut globally in Q1 2026 as companies including Snap, Disney, Meta and Oracle streamlined operations and reallocated budgets toward AI and cloud infrastructure. For investors in the NASDAQ and S&P 500, this trend suggests that labor-intensive growth is giving way to capital-intensive, automation-focused strategies.

While painful for employees, Wall Street typically welcomes such restructuring when it preserves growth while expanding margins. Notably, major hedge funds like Pershing Square have built large positions in Meta, arguing that the stock still underestimates the long-term upside from AI and that the core advertising franchise remains undervalued if losses from Reality Labs are stripped out. If Meta can sustain double-digit ad growth, scale MTIA and secure affordable power, the combination of higher revenue and lower headcount could drive significant earnings leverage over the next several years.

Related Coverage

For a deeper dive into how earlier workforce reductions reshaped sentiment, see Meta AI Layoffs +1.7% Surge as Efficiency Shock Hits, which explores whether prior cuts marked the start of a leaner AI supercycle. Investors interested in the broader AI hardware ecosystem can also read Intel AI Partnerships Rally With Google and Musk Shock, examining how new partnerships may reposition Intel against rivals in the data center market.

Overall, the new Meta Platforms Layoffs signal that management is determined to protect margins while funding one of the most ambitious AI investment programs in the S&P 500. For long-term shareholders, the balance between cost cuts and innovation will be crucial in determining whether Meta can turn today’s heavy AI capex into tomorrow’s profit engine. The upcoming April 29 earnings report should give Wall Street its first clear read on whether this strategy is working.