Is Arm’s data center AI push finally turning the chip designer into a true hyperscaler winner?

Why is Arm Holdings Data Center AI moving ARM?

The latest move in ARM reflects more than momentum chasing. Bernstein initiated coverage with an Outperform rating and a $300 price target, arguing that Arm is a structural winner in the CPU renaissance tied to agentic AI because of its energy efficiency. That call landed as investors were already re-rating the stock after fiscal fourth-quarter results showed that Arm’s business is increasingly tied to cloud and AI infrastructure rather than just smartphone royalties.

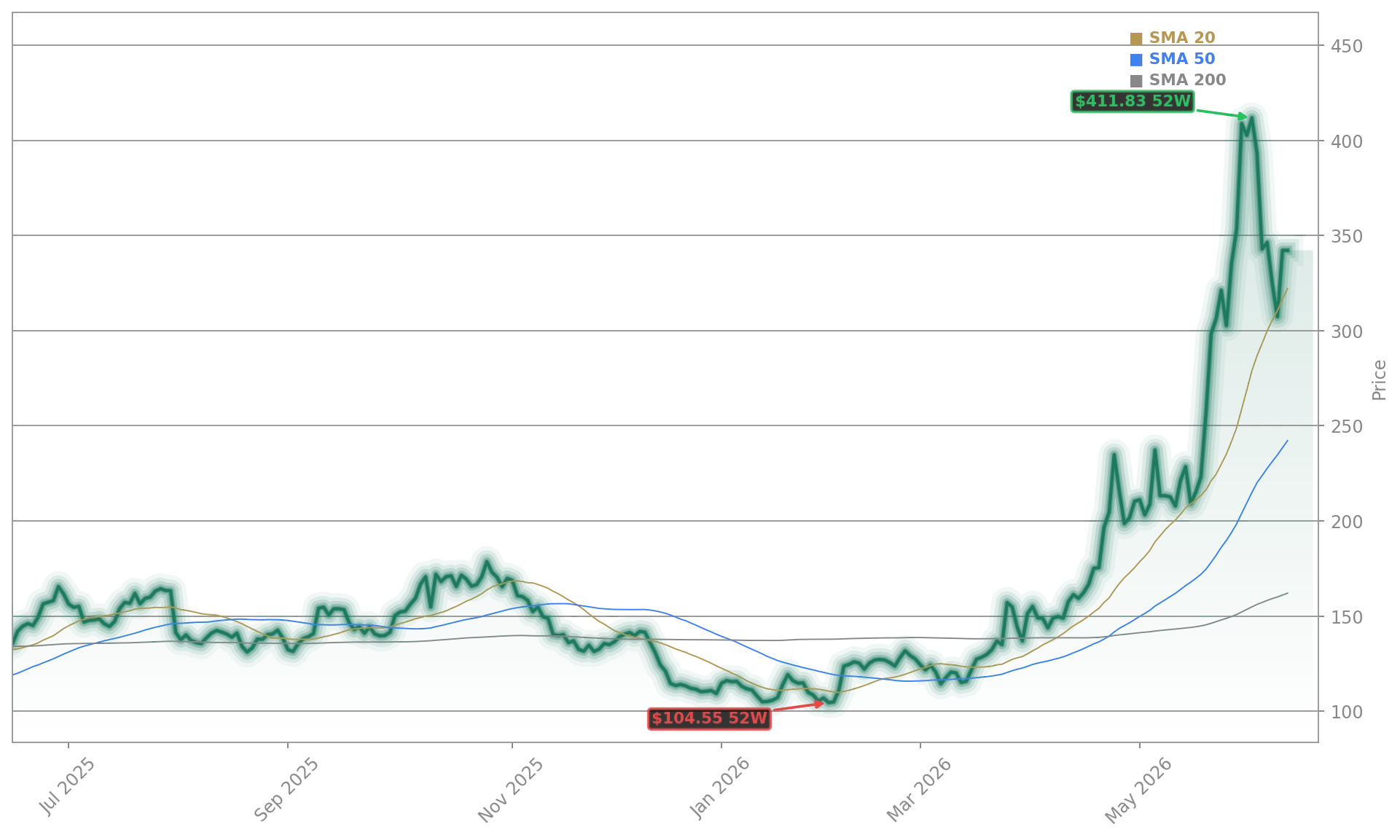

At $252.55, the stock is now well above the $223.15 levels discussed earlier this week and has extended its breakout. That also means shares are above the previously cited 52-week high of $239.50, so Wednesday’s move marks a fresh 52-week high based on current market data. The rally also stands out in a strong semiconductor tape that has supported names such as NVIDIA and other AI-linked chip companies.

Can ARM justify the new valuation?

Arm’s recent earnings gave bulls fresh material. Q4 FY2026 revenue rose 20.06% to $1.49 billion, while non-GAAP EPS of $0.60 beat consensus near $0.58. More importantly, data center royalty revenue more than doubled year over year, and annual contract value climbed 22% to $1.66 billion. Chief Executive Rene Haas said demand for the Arm AGI CPU, the company’s first data center chip, has exceeded expectations as AI workloads become more agentic.

The growth case behind Arm Holdings Data Center AI is increasingly tied to hyperscalers. Customer commitments for the AGI CPU reportedly jumped from $1 billion to more than $2 billion across FY2027 and FY2028 in roughly six weeks. Meta is a lead co-development partner, Google is using Arm-based Axion designs in next-generation TPU infrastructure, Microsoft is expanding Cobalt inside Azure, and NVIDIA is launching its Vera CPU on Arm architecture.

That said, valuation remains the central pushback. Arm has been trading around a trailing P/E near 250 and a forward P/E near 98, while non-GAAP operating margin slipped from 52.8% to 49.1% as research and development spending jumped 43% to $1.91 billion. Investors also still have to watch litigation involving Qualcomm-Nuvia, SoftBank’s controlling stake, and China-related exposure.

How broad is Arm Holdings support?

Wall Street support remains constructive, even if the stock has outrun older targets. The consensus target previously sat near $230.92, with 39 analysts split across 7 Strong Buy, 20 Buy, 10 Hold, 1 Sell, and 1 Strong Sell ratings. Bernstein’s new $300 target now raises the ceiling for bullish investors, while other recent positive notes and raised targets have reinforced confidence in ARM’s AI positioning.

Institutional interest also remains active. MarketBeat highlighted a new position from Partners Group Holding AG, while recent filings showed several insider transactions that were largely compensation-related. One notable exception was Chief Commercial Officer William Abbey, who sold 7,000 shares around $212.55 under disclosed arrangements. For most investors, however, the bigger issue is whether Arm can keep converting design wins into sustained royalty and silicon revenue.

What should investors watch next?

The next major test is execution. Bulls see Arm Holdings Data Center AI as the company’s bridge from IP licensor to AI infrastructure supplier, with management targeting a large share of a data center CPU market that could exceed $100 billion by 2030. Bears counter that Q1 FY2027 guidance of roughly $1.26 billion in revenue and $0.40 in EPS points to some sequential cooling after a strong quarter.

Related Coverage: Investors looking for a deeper read on the earlier setup can revisit this analysis of Arm Holdings Physical AI Boom: Revenue Jumps 23% Shock. That piece explored how Arm’s Physical AI and licensing strategy helped drive another year of 20%-plus growth, and it provides useful context for how the current data center narrative has intensified since earnings.

Arm Holdings Data Center AI is now the market’s core lens for ARM, and the stock’s breakout shows investors are willing to pay up for that transition. If AGI CPU adoption keeps accelerating across hyperscalers, Arm could keep separating itself from traditional semiconductor IP peers and become an even bigger name in AI infrastructure portfolios.

As AI becomes more agentic, demand for Arm AGI CPU, Arm’s first data center chip, has exceeded expectations.— Rene Haas

Fazit folgt.