Is Arm becoming the real winner of AI’s shift from GPU hype to CPU-heavy infrastructure demand?

Why Is Arm Holdings CPU Renaissance Reshaping AI Infrastructure?

Arm Holdings plc is no longer just the silent engine behind Apple’s M-series chips — it’s emerging as the central nervous system for next-generation AI deployments. As Bernstein noted in its June 17, 2026 client note, the shift from AI 1.0 (chatbot inference) to AI 2.0 (autonomous agentic workflows) has dramatically increased CPU workload density. Where AI training previously relied on GPU-heavy clusters with a CPU-to-GPU ratio of 1:4–1:8, agentic AI now demands near 1:1 or even CPU-heavy configurations. Arm’s power-efficient, scalable architecture — licensed across smartphones, servers, and edge devices — is uniquely positioned to capture this structural shift. That’s why Arm’s royalty growth accelerated to 20% annually, even amid smartphone unit softness, as higher-end device mix and infrastructure adoption lifted per-unit revenue.

How Are Wall Street Analysts Reacting to Arm’s Momentum?

Bernstein isn’t alone — but it’s the most aggressive voice validating the Arm Holdings CPU Renaissance. The firm raised Arm Holdings plc’s price target to $500 from $300 and maintained its Outperform rating. Meanwhile, Deutsche Bank and Citi have lifted Micron Technology’s targets on parallel AI infrastructure tailwinds, reinforcing the broader semiconductor rebound. Arm’s forward P/E of 191x may appear stretched, but Bernstein’s revised $22 billion revenue forecast for 2030 — up from $15 billion — reflects confidence in Arm’s transition from IP licensor to full-stack CPU platform provider. With 25 Buy ratings dominating the consensus, the Street is betting Arm’s structural advantages in power efficiency, licensing leverage, and hyperscaler adoption (including Apple, NVIDIA, and Meta) will sustain premium valuation.

What Does This Mean for the S&P 500 and NASDAQ?

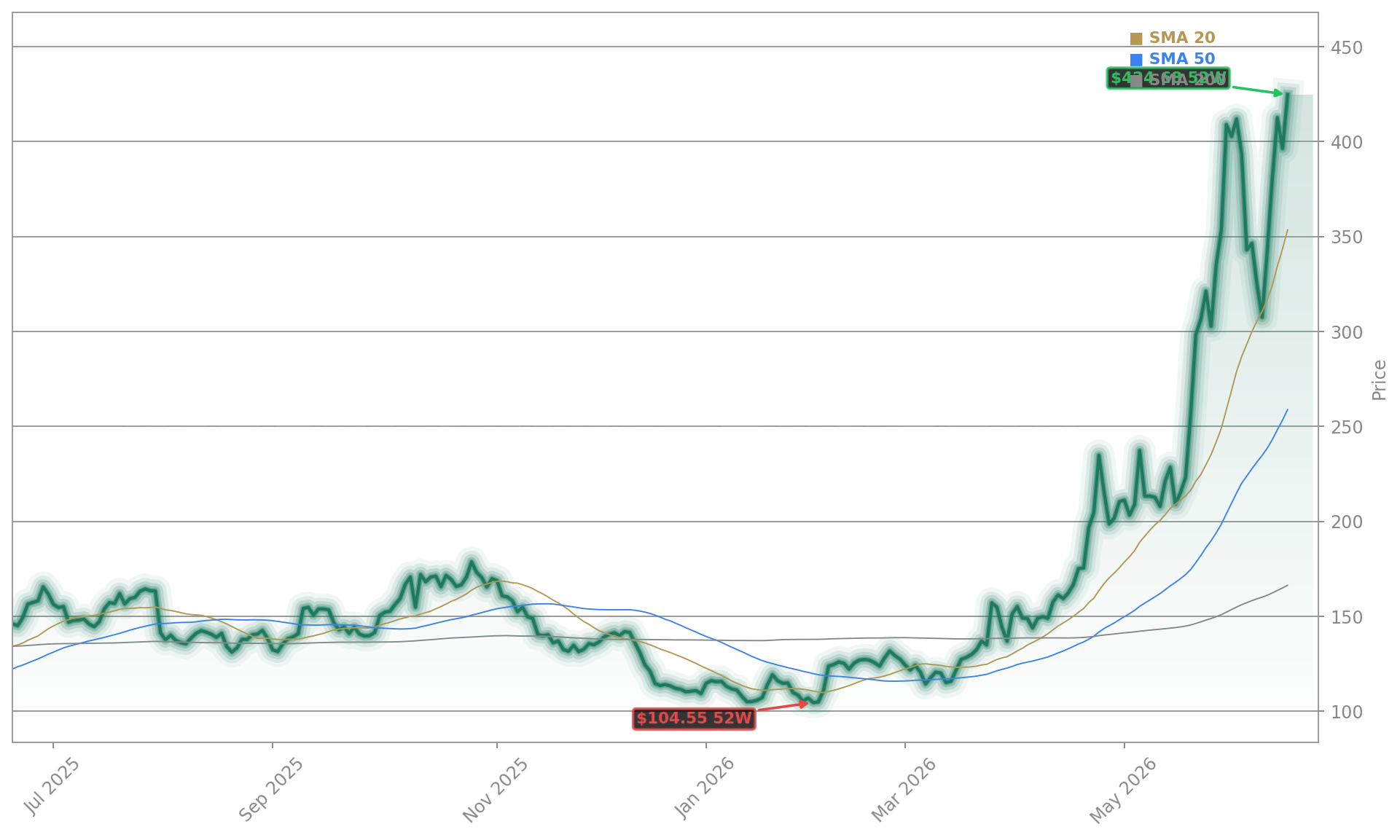

Arm Holdings plc’s 7.7% intraday jump on Wednesday — to $426.79 — contributed meaningfully to the Philadelphia Semiconductor Index’s (SOX) 3.2% rebound after Tuesday’s 5.7% selloff. That volatility underscores how tightly Arm’s trajectory is now linked to AI infrastructure sentiment across the broader tech complex. Unlike traditional chipmakers, Arm’s near-zero capex, 90%+ gross margins, and recurring royalty model make it a rare high-growth, high-quality compounder — a profile increasingly prized by U.S. institutional investors navigating geopolitical uncertainty and rising rate volatility. Its 52-week high — achieved just yesterday — signals growing acceptance that Arm Holdings CPU Renaissance isn’t cyclical, but secular. For S&P 500 tech-weighted ETFs and NASDAQ-100 holders, Arm is rapidly evolving from satellite exposure to core infrastructure holding.

How Does Arm Compare to AMD and Intel in the CPU Rebound?

Bernstein’s simultaneous price target hikes for AMD (to $600) and Intel (to $100) confirm a broad-based CPU renaissance — but Arm’s upside is structurally distinct. AMD and Intel sell physical chips; Arm licenses the foundational architecture, collects royalties on every chip shipped, and captures value across device tiers — from smartphones to AI servers. While AMD’s EPYC and Intel’s Xeon compete directly in data centers, Arm’s Neoverse and CSS platform enable hyperscalers like Meta and Tesla to build custom silicon optimized for AI orchestration. That flexibility — plus Arm’s dominance in mobile and embedded — gives it a wider total addressable market (TAM) of $223 billion by 2030, per Bernstein. In contrast, AMD and Intel remain capital-intensive, manufacturing-constrained, and exposed to GPU-centric AI cycles. For U.S. investors seeking asymmetric exposure to CPU-driven AI, Arm Holdings plc offers a differentiated, asset-light lever.

What’s Next for Arm Holdings plc’s Growth Trajectory?

With royalty growth reaffirmed at ~20% long-term and hyperscaler adoption expanding beyond smartphones into AI inference servers and autonomous systems, Arm Holdings plc is entering a multi-year inflection. The company’s shift toward higher-value, AI-optimized licensing — including its new AGI CPU architecture — positions it to outpace broader semiconductor growth. Bernstein’s $500 target implies 17% upside from current levels, but more importantly, signals Wall Street’s growing conviction in the Arm Holdings CPU Renaissance as a foundational shift — not a short-term trend. For U.S. portfolios, this isn’t just about one stock: it’s about recognizing that CPUs are reclaiming centrality in the AI stack, and Arm is the clear architectural standard.

Related Coverage: Arm Holdings’ AI strategy remains under intense valuation scrutiny — as highlighted in Arm Holdings AI Strategy: ARM Drops 2.3% on Valuation Warning. Meanwhile, Broadcom’s explosive Q2 AI revenue surge reinforces sector-wide momentum — see Broadcom AI Earnings +3.3% as Q2 AI Revenue Soars.

The shift (in the) AI paradigm from 1.0 (chatbot) to 2.0 (agent) greatly increases server CPU demand. Agentic AI involves heavily autonomous task orchestration and execution, which boosts the CPU workload vs. GPU.— Bernstein analysts

Arm Holdings CPU Renaissance is now a core pillar of Wall Street’s AI infrastructure thesis. For U.S. investors, Arm Holdings plc represents a high-conviction, high-margin compounder at the center of the next wave of AI deployment. The $500 price target from Bernstein isn’t just a number — it’s a vote of confidence in Arm’s irreplaceable role across mobile, cloud, and edge AI. The next catalyst will be Q2 2026 earnings, where royalty growth and hyperscaler design wins will confirm whether the Arm Holdings CPU Renaissance is accelerating — not peaking.