Is Arm’s sharp selloff just a momentum shakeout, or the first real sign that AI valuations have gone too far?

Why Did Arm Holdings Plunge?

The Arm Holdings Plunge wasn’t triggered by earnings misses or guidance cuts — Arm Holdings plc reported record Q4 2026 revenue of $1.49 billion and full-year revenue of $4.92 billion, up 20%+ for the third consecutive year. Instead, the selloff reflects a sector-wide unwind of momentum positions. The iShares Semiconductor ETF (SOXX) dropped 4.5%, with Arm Holdings plc down 8.9% intraday — worse than Micron (-7.3%) and Marvell (-10.7%). According to Benzinga, Arm trades 130% above its 200-day moving average, the third-highest gap in the chip sector behind Marvell (250%) and Micron (160%). That extreme technical stretch, combined with a forward P/E near 159x, made Arm Holdings plc uniquely vulnerable when momentum stalled.

Is Arm Holdings Plunge a Buying Opportunity?

Yes — if investors focus on fundamentals over froth. Mizuho upgraded Arm Holdings plc to Outperform on June 4 and raised its price target to $500 from $425, citing accelerating agentic AI adoption across Oracle and ByteDance. The firm projects $15 billion in agentic AI infrastructure CPU revenue by fiscal 2031. Crucially, Arm Holdings plc delivered record full-year royalty revenue of $2.61 billion, with data center royalties more than doubling year-over-year — a direct proxy for cloud AI chip deployment. That growth remains uncorrelated to near-term SOXX volatility and reinforces Arm’s structural advantage versus integrated rivals like Tesla and NVIDIA in the AI infrastructure stack.

How Does Arm Compare to Chip Peers?

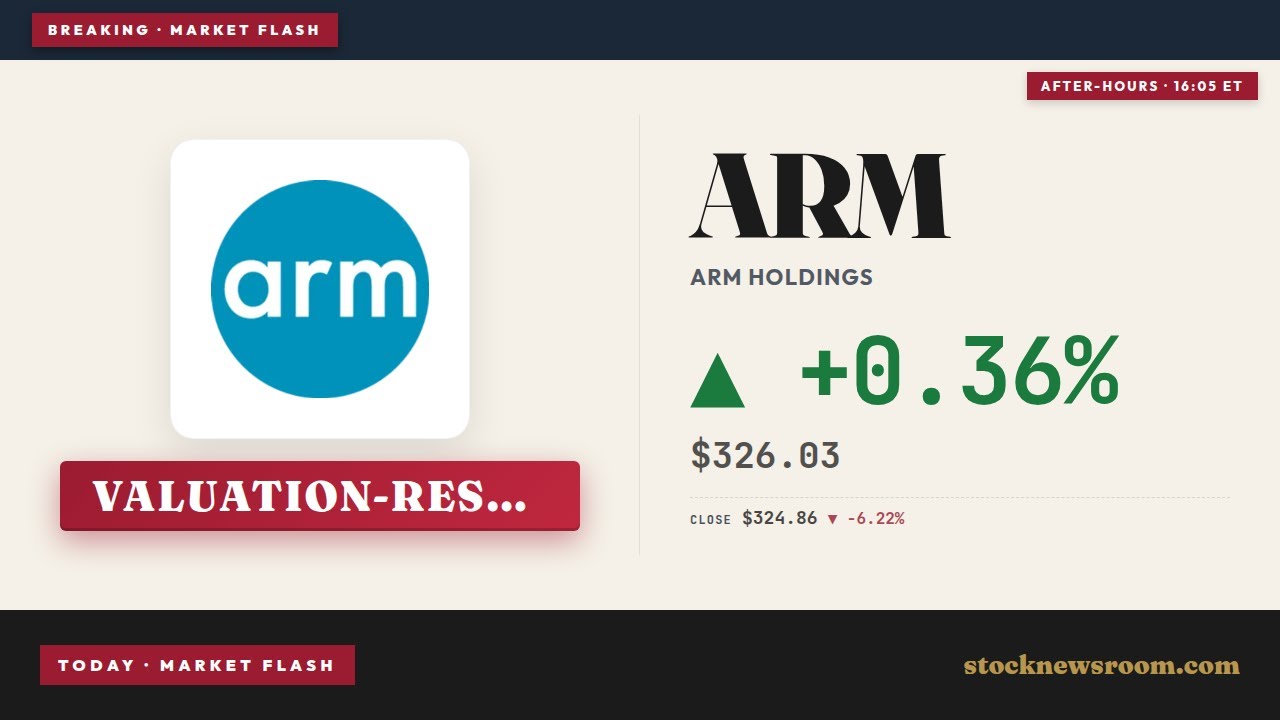

Arm Holdings plc is the most expensive major chip stock by forward P/E — 159x — dwarfing Intel (104x), Marvell (63.7x), and Micron (9.8x). Yet unlike Intel or Marvell, Arm doesn’t manufacture chips or bear fab costs. Its royalty-based model delivers 92% gross margins and near-zero inventory risk — a structural moat amid cyclicality. That explains why even amid the Arm Holdings Plunge, after-hours trading saw shares rebound 0.36% to $326.03. In contrast, Intel’s valuation premium has eroded as its foundry losses mount, and Marvell’s exposure to networking hardware leaves it more sensitive to capex cycles. Arm’s exposure is pure AI adoption — and that trend shows no signs of reversal.

What Do Analysts Say About the Arm Holdings Plunge?

Mizuho isn’t alone in doubling down. Citigroup reaffirmed its Buy rating last week and raised its fiscal 2027 revenue estimate by 8%, citing stronger-than-expected Edge AI licensing in automotive and robotics. RBC Capital Markets upgraded Arm Holdings plc to Outperform in early May, citing ‘unmatched scalability in heterogeneous AI compute.’ Goldman Sachs maintains a $480 price target, emphasizing Arm’s role as the de facto architecture for AI inference chips across smartphone, cloud, and physical AI use cases. All three banks explicitly cited the Arm Holdings Plunge as a tactical entry point — not a fundamental inflection — given the company’s royalty visibility, multi-year design wins, and lack of balance sheet risk.

Where Is the Next Catalyst?

The next catalyst arrives in early August with Arm Holdings plc’s Q1 2026 earnings — the first full-quarter reflection of its expanded cloud AI partnerships with Oracle and ByteDance. Analysts expect royalty revenue to grow 32% year-over-year, driven by new data center deployments and a 40% increase in licensed AI chip designs. Meanwhile, the broader semiconductor sector remains in a technical correction, but SOXX’s 65% premium to its 200-day moving average — down from 85% in early June — suggests stabilization is near. For Arm Holdings plc, the Arm Holdings Plunge may prove to be the last major valuation reset before the next leg up in AI infrastructure spend.

Related Coverage: Is Arm’s sharp drop just overheated AI trade profit-taking, or the first real warning that valuation finally matters again? Arm Holdings Semiconductor Selloff: Why ARM Fell 8.6% analyzes the technical triggers and contrasts Arm’s royalty model with traditional chipmakers’ capital intensity.

Arm’s agentic AI tailwinds are accelerating as its platform expands with Oracle and ByteDance.— Mizuho Research

Arm Holdings plc remains a core AI infrastructure holding for long-term portfolios — the Arm Holdings Plunge reflects market-wide momentum fatigue, not deteriorating fundamentals. For investors, the valuation reset creates a higher-conviction entry point ahead of accelerating agentic AI adoption. The next quarterly earnings will confirm whether cloud and edge AI royalties continue to outpace expectations — and whether the Arm Holdings Plunge marks the end of the first AI chip valuation phase.