Can Arm Holdings AI Strategy justify a sky-high valuation as agentic AI demand accelerates faster than management expected?

Why is Arm Holdings AI Strategy moving shares?

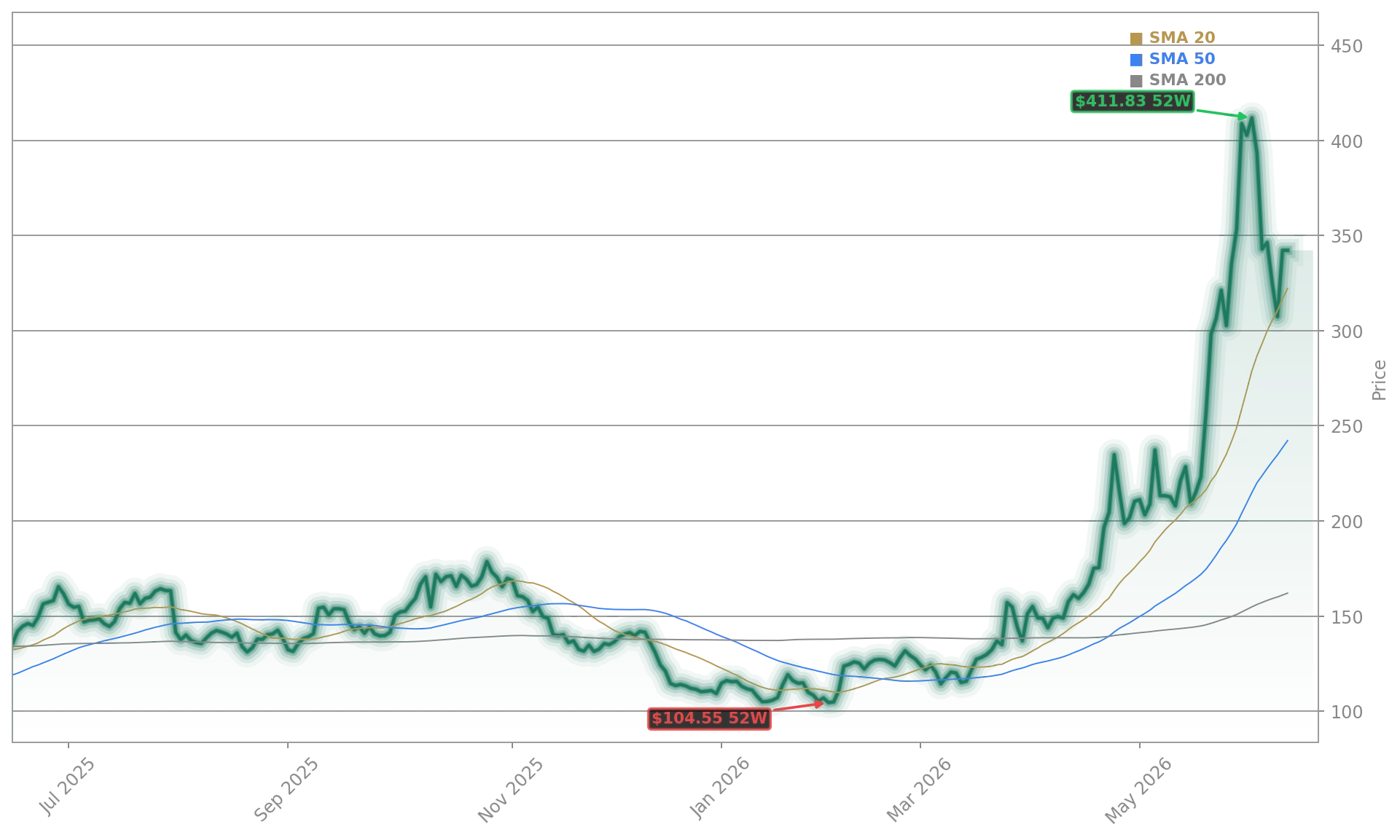

Arm Holdings plc remains one of Wall Street’s most closely watched AI names after a huge May rally, but the stock turned volatile on Wednesday despite fresh optimism from management. ARM closed at $402.71 versus a previous close of $397.87, then pointed 0.84% higher in pre-market activity at $406.11. That reaction shows investors are weighing two forces at once: exceptional AI momentum and a valuation that already reflects very aggressive growth assumptions.

At Computex, CEO Rene Haas said Arm may hit its $15 billion revenue target for its own-branded chips earlier than expected because AI-driven demand has been stronger than projected. He also made a broader case for the Arm Holdings AI Strategy, saying CPUs are essential for agentic AI because token distribution, management, and orchestration still need central processors. That matters for US investors because Arm sits at the architecture layer of a wide swath of AI hardware, giving it leverage across multiple end markets instead of one product cycle.

How does ARM benefit from agentic AI?

The bullish argument is not only about smartphone heritage anymore. Arm is increasingly seen as a core enabler of AI inference, cloud computing, and next-generation data center workloads. Haas has also warned that memory remains the toughest supply bottleneck in the AI buildout, suggesting demand for compute is still outrunning available infrastructure. If that stays true, the Arm Holdings AI Strategy could benefit from long-duration spending by hyperscalers and semiconductor partners.

That thesis has been reinforced by NVIDIA. Its Grace Blackwell platform combines Arm-based CPUs with NVIDIA GPUs, and the upcoming Vera CPU uses custom Arm cores. NVIDIA has framed agentic AI and reinforcement learning as new growth opportunities for CPUs, expanding the total addressable market for this part of the stack. For Arm, that creates a compelling read-through: every successful Arm-based CPU deployment in AI servers can support royalty growth, broader ecosystem relevance, and stronger negotiating power with customers building custom silicon.

Wall Street has responded with increasingly bullish calls. Bernstein initiated coverage with a buy rating in May and helped spark a sharp rally. RBC Capital, Jefferies, TD Cowen, and Mizuho also lifted price targets recently as enthusiasm around AI licensing demand and data center royalties accelerated. Even so, some caution remains. 24/7 Wall St. recently argued that near-term upside may be limited after the stock’s massive run, highlighting how sensitive ARM has become to expectations.

What does ARM mean for rivals and partners?

ARM’s position is unusual because it can win alongside several industry leaders. Strong AI server demand helps partners like NVIDIA, while edge AI expansion can create indirect support from companies such as Apple and Tesla that rely on efficient compute designs. That diversification is central to the Arm Holdings AI Strategy: the company does not need to beat every chipmaker directly if its architecture becomes more deeply embedded across the ecosystem.

Recent financial guidance has added to the optimism. Arm previously guided for fiscal first-quarter revenue of about $1.26 billion, up 20% year over year, with adjusted earnings per share of $0.40, up 14%. Analysts also expect earnings growth to accelerate in fiscal 2028 after a strong fiscal 2027. Still, investors should remember that the stock’s huge 2026 gain leaves little room for execution misses, especially if supply constraints in memory or wafer capacity delay customer rollouts.

Related Coverage: Investors looking for the latest catalyst behind the recent surge can also read this breakdown of Arm Holdings Computex momentum and NVIDIA-driven PC optimism. That report explains how Computex excitement, Arm-based PC chips, and AI demand combined to push the stock sharply higher, while also asking whether the rally is starting to outrun fundamentals.

The distribution, management and orchestration of tokens can only be done by CPUs.— Rene Haas

Arm Holdings AI Strategy now hinges on whether management can convert AI enthusiasm into durable royalty and chip revenue growth. For investors, the story remains powerful because Arm sits at the center of the CPU role in agentic AI, but the next few quarters will need to justify the premium. If execution keeps matching the narrative, Arm Holdings AI Strategy could remain one of the semiconductor market’s most influential themes in 2026.