Can Arm’s new AI CPU push justify a soaring valuation, or is Wall Street getting ahead of execution?

Why Did TD Cowen Raise Arm Holdings Forecast?

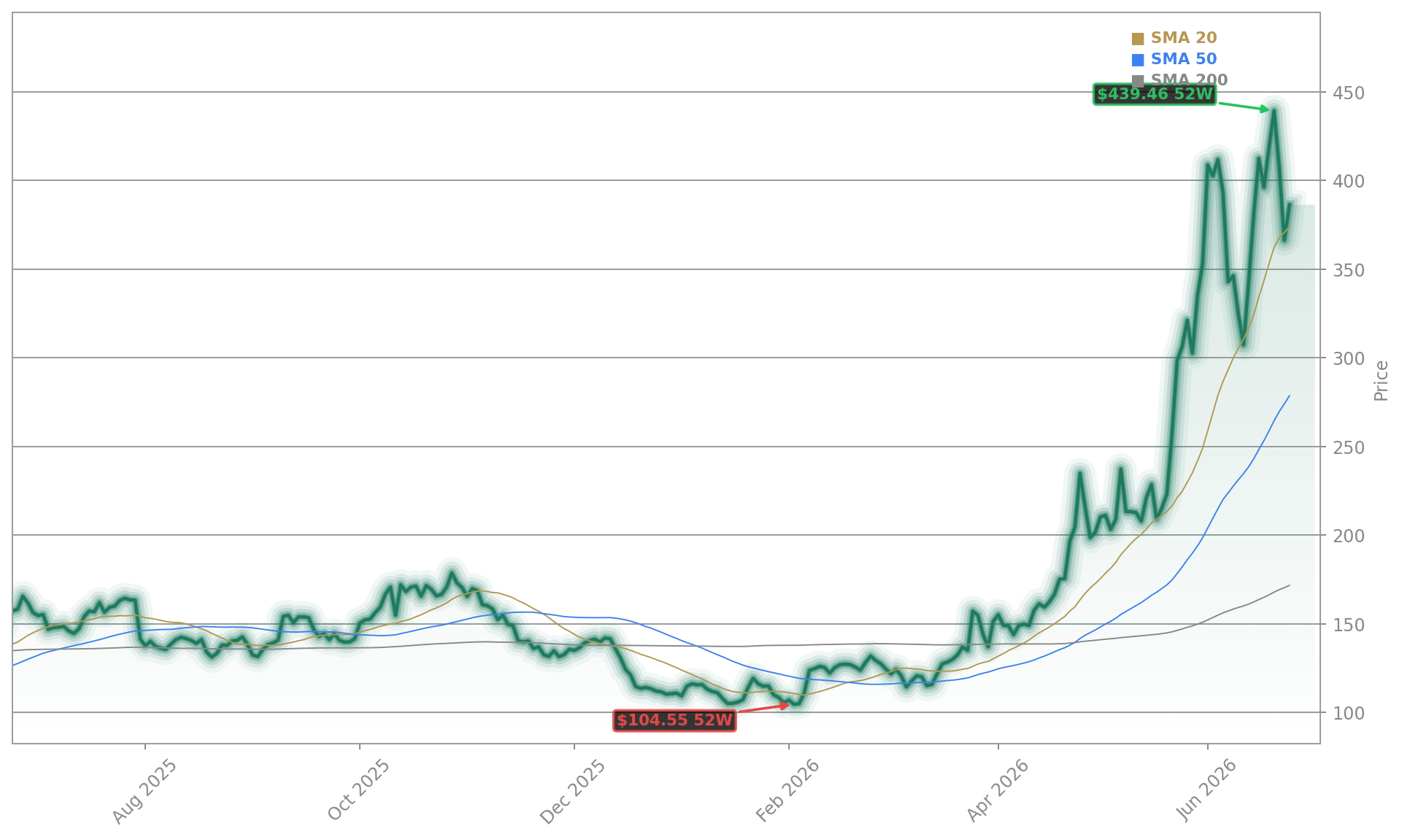

TD Cowen analyst Krish Sankar raised Arm Holdings plc’s price target to $475 from $265 — a 79% increase — citing robust demand for Arm’s first data center processor, the AGI CPU. The upgrade arrives just weeks after Arm reported Q4 FY2026 revenue of $1.49 billion, up 20.1% year-over-year, with data center royalty revenue more than doubling. Crucially, CEO Rene Haas confirmed that demand for the AGI CPU has “exceeded expectations,” with over $2 billion in customer demand already pipelined through FY28. That pipeline includes co-development with Meta — a strategic signal that Arm is no longer just enabling AI hardware, but co-designing it.

How Is Arm Disrupting the CPU Market?

Arm Holdings plc is executing a structural shift — from licensing chip blueprints to delivering complete, high-performance CPUs optimized for AI inference. Unlike NVIDIA, which dominates AI training with GPUs, Arm is capturing the next layer: the CPU backbone that manages memory, orchestrates workloads, and delivers power efficiency at scale. Amazon’s Graviton now powers over half of newly added server capacity; Microsoft’s Cobalt and Google’s Axion are scaling rapidly; and NVIDIA’s Grace CPU is built on Arm architecture. UBS estimates Arm-based chips could capture 40–45% of server CPU shipments by 2030 — directly challenging Intel and AMD. The advantage isn’t theoretical: Arm’s smartphone-born architecture delivers superior performance-per-watt, a critical metric as hyperscalers face $30+ billion annual power and cooling costs.

Arm Holdings Forecast vs. AMD’s Execution Edge?

Arm Holdings Forecast optimism must be weighed against near-term execution risk — and AMD’s contrasting momentum. While Arm posted 20.1% revenue growth, AMD delivered 37.9% growth in Q1 2026, with data center revenue surging 57% to $5.78 billion. AMD’s fabless model generates $2.57 billion in free cash flow — more than triple last year — and its MI450 Series ramp is gaining traction with Meta and OpenAI. Arm’s gross margin remains stellar at 92.5%, but R&D jumped 43% to $1.91 billion, compressing non-GAAP operating margin to 49.1%. At a P/E of 433, Arm’s valuation demands flawless AGI CPU delivery — a test investors will watch closely in H2 2026.

What Does This Mean for Wall Street Portfolios?

For U.S. investors, Arm Holdings Forecast upgrades signal broader portfolio implications across the S&P 500 and NASDAQ. Arm’s rise isn’t isolated — it’s part of a structural reallocation toward energy-efficient AI infrastructure. That benefits not just Arm, but also memory leaders like Micron Technology and chiplet enablers in the semiconductor supply chain. Meanwhile, traditional x86 players face margin pressure: Intel’s Xeon and AMD’s EPYC are losing design wins to custom Arm silicon. The NASDAQ Composite, heavily weighted toward tech and AI enablers, stands to gain from Arm’s expanding role — especially as it begins shipping full processors rather than just licensing IP. With Arm up 235% year-to-date, the stock is no longer a satellite play — it’s a core AI infrastructure holding.

Arm Holdings Forecast: What’s Next on the Roadmap?

The next major catalyst is AGI CPU volume shipment — expected in Q3 2026 — and confirmation of royalty rate expansion on data center sockets. Arm’s $2 billion demand pipeline includes multiple hyperscalers and AI-native firms, but execution timing will determine whether the $475 price target is achievable by year-end. Also watch for updates on SoftBank’s investment in Intel’s foundry, which could accelerate Arm’s direct-chip strategy without requiring capital-intensive fabs. With AI inference demand growing exponentially, Arm’s ability to monetize both licensing *and* silicon will define the next phase of its Arm Holdings Forecast trajectory.

Demand for Arm AGI CPU, Arm’s first data center chip, has exceeded expectations.— Rene Haas, CEO of Arm Holdings plc

Related Coverage: Arm’s AI CPU renaissance continues to gain momentum — read how the company surged 7.7% last week on widening infrastructure adoption in Arm Holdings CPU Renaissance: ARM Surges 7.7% on AI. Meanwhile, memory remains a key AI enabler — Micron’s record Q3 results and bullish Q4 outlook confirm its strategic role in the AI stack, as detailed in Micron Earnings +13.3% After Record Q3 and Q4 Outlook.