Can Nvidia’s aggressive CPU push turn Arm’s AI story into a much bigger royalty machine than investors expected?

Why is Arm Holdings CPU Forecast jumping?

Arm Holdings plc was one of the standout AI-infrastructure winners on Thursday, extending gains after Nvidia’s quarterly update highlighted a much bigger CPU opportunity than many investors had modeled. Nvidia said it now sees a path to $20 billion in CPU revenue this year, with much of that tied to Vera, a custom CPU design built on Arm technology. That was enough to ignite a fresh rerating in the Arm Holdings CPU Forecast, especially because royalty economics improve when newer Arm designs gain share in data centers.

The stock’s move also reflected relative positioning. While Intel and AMD traded lower after Nvidia’s commentary sharpened competitive pressure in server CPUs, Arm was seen as a platform beneficiary rather than a direct volume loser. For Wall Street, that distinction matters: Arm sells architecture and collects royalties, so it can benefit when partners win share without taking on manufacturing risk.

How important is NVIDIA for ARM?

NVIDIA’s latest messaging added a concrete framework to Arm’s upside case. Vera is based on custom Arm cores, and Nvidia said the chip offers 1.5 times faster performance per core and four times more rack density than x86 alternatives. If those claims hold in broad deployment, Arm could capture a larger slice of the data center buildout now being driven by AI inference and agentic workloads.

That supports a more bullish Arm Holdings CPU Forecast because the company has already said data center revenue more than doubled in its most recent quarter and may soon surpass smartphones as its largest business. Investors are also focused on Arm v9, which carries higher royalty economics than older versions. Nvidia’s CPU ramp therefore matters not just for unit growth, but for mix and monetization.

Even so, not everyone on Wall Street is chasing the move. Jim Cramer said he likes Arm “very much” but called the idea that it was the biggest winner from Nvidia’s call “a little silly.” That caution fits the backdrop: Arm’s valuation already reflects major AI expectations, so execution will need to keep pace.

What does ARM mean for rivals?

The market reaction highlighted a growing divide in the CPU landscape. Nvidia’s push into standalone CPUs raises the stakes for x86 incumbents while strengthening Arm’s position as an ecosystem enabler. That is one reason ARM led gainers in the Nasdaq 100 during Thursday trading, outperforming many semiconductor peers.

For US investors, the appeal is strategic exposure. Arm sits at the center of smartphone chips, cloud silicon, automotive compute, and increasingly AI servers. Partners such as Apple and Tesla have already shown how Arm-based designs can win on power efficiency and vertical integration. If hyperscalers adopt more Arm-compatible server designs, the company could benefit across multiple customer sets rather than relying on one flagship program.

No fresh analyst note from Citigroup or RBC Capital Markets was attached to Thursday’s move in the available reporting, but the setup is exactly the kind of catalyst those firms typically watch: a partner-driven demand signal that could translate into estimate revisions for royalty growth. That makes upcoming commentary from major banks especially relevant after such a sharp price response.

Can Arm Holdings CPU Forecast keep rising?

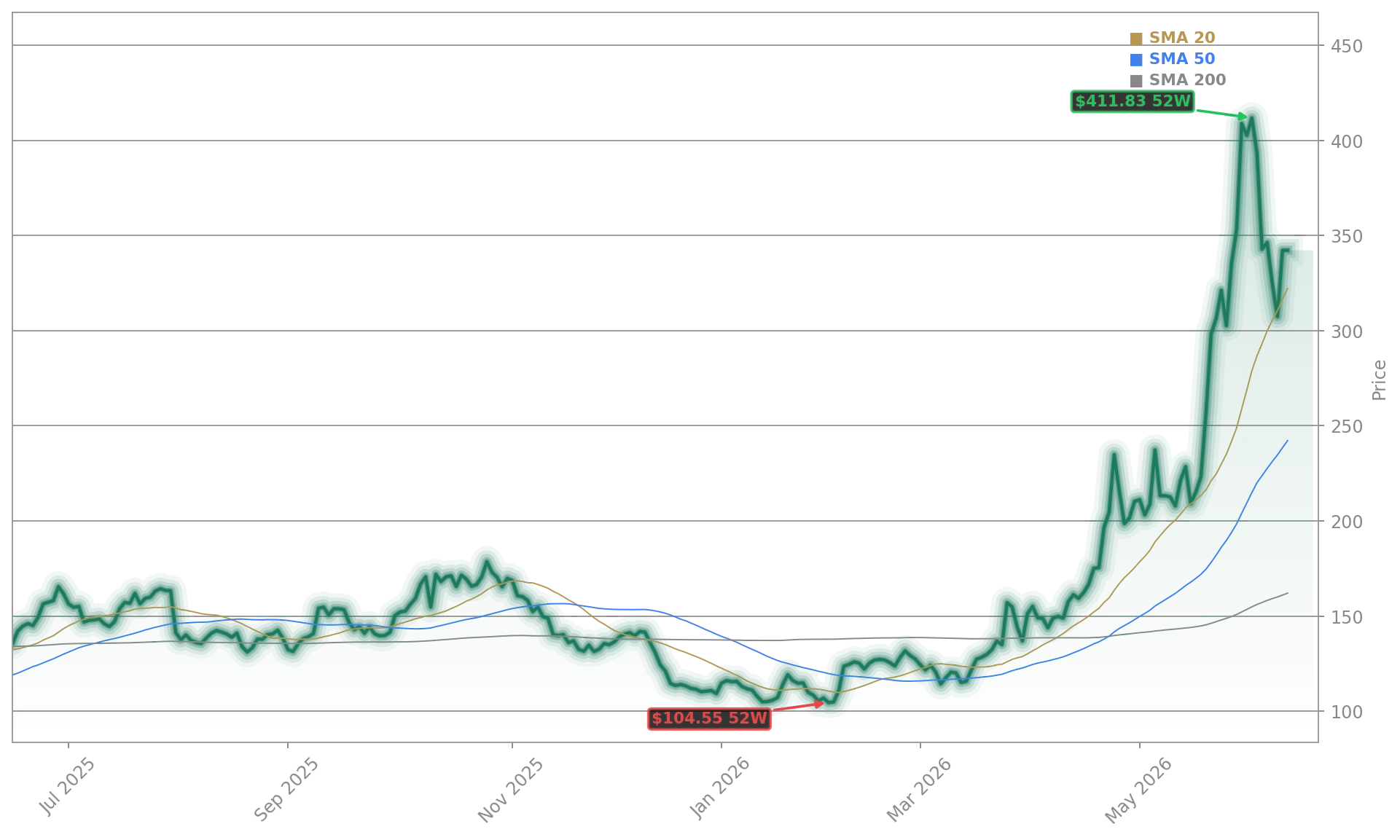

Momentum is clearly strong, but investors should separate narrative from near-term math. At $293.42, Arm has added another leg to an already powerful 2026 run, and the stock has significantly outperformed the broader Nasdaq this year. The bull case is that Nvidia’s CPU roadmap validates Arm’s architecture advantage in data centers just as AI workloads expand beyond training into inference-heavy deployment.

The risk is that expectations are now moving faster than measurable royalty recognition. Arm remains a premium multiple story, and even bullish investors will want clearer evidence that Vera shipments, broader server adoption, and v9 mix gains are translating into sustained upside. Related Coverage: Investors looking for a deeper read on Arm’s hyperscaler opportunity should also see Arm Holdings Data Center AI Jumps 13.2% on AGI Momentum. That report examines how agentic AI demand is reshaping the company’s data center narrative and why Arm’s server exposure is becoming more central to the long-term thesis.

We have a nice sized position in ARM and while I like it very much, it seems a little silly that it is last night’s BIGGEST winner off of the Nvidia call— Jim Cramer

The latest Arm Holdings CPU Forecast is bullish for a reason: Nvidia’s Vera push gives Wall Street a tangible new path to higher Arm royalties. For investors, the next step is watching whether partner momentum turns into durable revenue acceleration. If that happens, Arm could remain one of the market’s most important AI infrastructure enablers.