Is Arm Holdings’ bold Physical AI push enough to justify sky-high valuations after another year of 20%+ growth?

Is Arm’s post-earnings pullback justified?

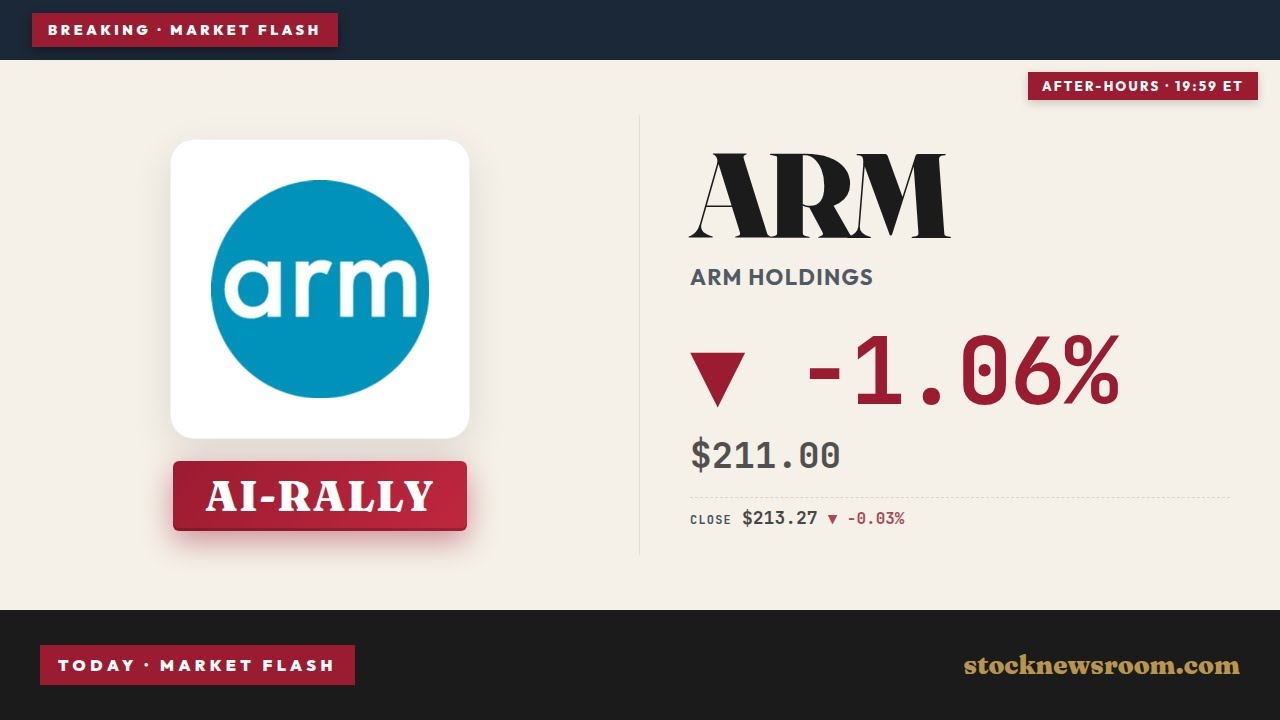

Shares of Arm Holdings plc have been explosive in 2026, up roughly 90% year to date, but the latest earnings reaction shows how fragile sentiment has become. The stock now changes hands around $213 during Friday’s U.S. session, down marginally on the day, and slips another 1% to roughly $211 in after-hours trading. That fade comes even after Arm delivered fiscal 2026 revenue of about $4.92 billion, up 23% year over year, with a third straight year of 20%-plus top-line growth.

Licensing revenue rose 29% to approximately $819 million in the latest quarter, while royalty revenue climbed 11% to around $671 million, supported by rapid AI adoption in data centers and smartphones. Data center royalties more than doubled, underscoring Arm’s growing footprint in AI servers dominated by NVIDIA accelerators. Yet at a trailing P/E near 280 and a price-to-sales multiple in the mid‑50s, even solid execution is not always enough to satisfy a market that has priced in years of perfection.

How are Wall Street analysts reacting to Arm Holdings?

Despite the wobble around results, analyst sentiment remains broadly favorable but cautious on valuation. TipRanks highlights at least one analyst maintaining a Buy rating with a $255 price target, implying upside from current levels but less than earlier in the year as the share price has run ahead of fundamentals. Wells Fargo recently lifted its target to $220, emphasizing Arm’s central role in the AI compute stack and the long tail of royalty revenues from its architecture.

UBS moved even more aggressively, raising its target to $245 and forecasting that Arm’s share of server CPU shipments could hit 40% to 45% by 2030 as agentic AI workloads proliferate. Across the Street, the consensus rating sits in “Moderate Buy” territory, but the average target remains well below the current quote around $213, reflecting lingering concerns that Arm’s premium multiples leave little margin of safety if AI spending normalizes or if competition from x86 and RISC‑V intensifies.

Why does Arm Holdings Physical AI matter for autos and robotics?

The most compelling long-term narrative is the emerging Arm Holdings Physical AI strategy, which focuses on embedding AI into physical systems such as autonomous cars, industrial robots, and consumer devices. Arm has reorganized its business around this opportunity, creating a dedicated Physical AI unit alongside its data center and mobile operations. CFO Jason Child estimates that Arm commands roughly 80% CPU share in automotive and robotics, a dominant position that gives it leverage as robotaxis and humanoid robots move closer to commercialization.

Arm-based designs already sit at the heart of electric vehicles from companies like Tesla, as well as robots from Tesla, Boston Dynamics, and several Chinese manufacturers. Arm cores also underpin NVIDIA’s Jetson Thor platform, widely viewed as a leading robotics chip. While Child cautions that a true ramp in robotics revenue may still be five to ten years away, the addressable market could be enormous as Physical AI turns transport, logistics, and manufacturing into software-like, data-driven businesses.

How does Arm’s new AGI CPU fit into the AI race?

At the same time, Arm is not content to remain only a licensor. The company is launching its first in-house chip, the Arm AGI CPU, designed to accelerate AI inference and general-purpose compute in data centers and at the edge. Management has already lined up more than $2 billion in customer demand for AGI across fiscal 2027 and 2028, a meaningful forward revenue indicator for a company still generating under $5 billion annually.

The AGI initiative strengthens the Arm Holdings Physical AI story because it gives Arm more control over performance, power efficiency, and software stacks in AI-heavy workloads. For U.S. investors comparing Arm with well-known AI winners like Apple in smartphones or Tesla in EVs, the AGI CPU offers a clearer monetization pathway beyond traditional licensing, but it also adds execution risk at a time when expectations are sky‑high.

How does Arm compare to other AI chip plays?

Compared with legacy chipmakers such as Intel and AMD, Arm sports far richer multiples. Intel, for example, trades at a far lower price-to-sales ratio around 11 and a substantially cheaper EV/EBITDA, even after a more than 200% year-to-date rally. Retirement-focused or capital-preservation investors may prefer Intel’s stronger asset backing and lower beta, especially as Arm’s stock still carries a beta north of 3, amplifying moves in both directions relative to the S&P 500 and NASDAQ.

On the flip side, growth-oriented portfolios targeting the next decade of AI may see Arm as closer in spirit to NVIDIA: a critical architecture provider that benefits from industry-wide AI demand. If Physical AI in cars and robots scales as management expects, Arm’s royalty-powered model could produce outsized operating leverage, albeit with higher volatility than more diversified mega caps.

Related Coverage

For a deeper dive into how Arm’s latest report moved the stock immediately after earnings and how the data center business feeds into the AI narrative, readers can review Arm Holdings Earnings +13.6% Rally as AI Bets Grow. That analysis looks closely at the initial double‑digit post‑earnings jump and tests whether the current AI enthusiasm is enough to support Arm’s premium valuation.

In summary, the Arm Holdings Physical AI opportunity in autos, robots, and edge devices is increasingly central to how Wall Street values the stock, even as near-term earnings headlines trigger sharp swings. For U.S. investors, the trade-off is between a richly priced but uniquely positioned AI architecture leader and cheaper, more mature chip names. The next few quarters of AGI CPU traction and progress in automotive and robotics design wins will be critical in proving whether the Physical AI thesis can justify today’s multiples and keep Arm at the forefront of the AI hardware cycle.