Are Meta AI Layoffs the start of a leaner, more profitable AI supercycle or a warning sign hidden behind record spending?

How do Meta AI Layoffs hit the stock story?

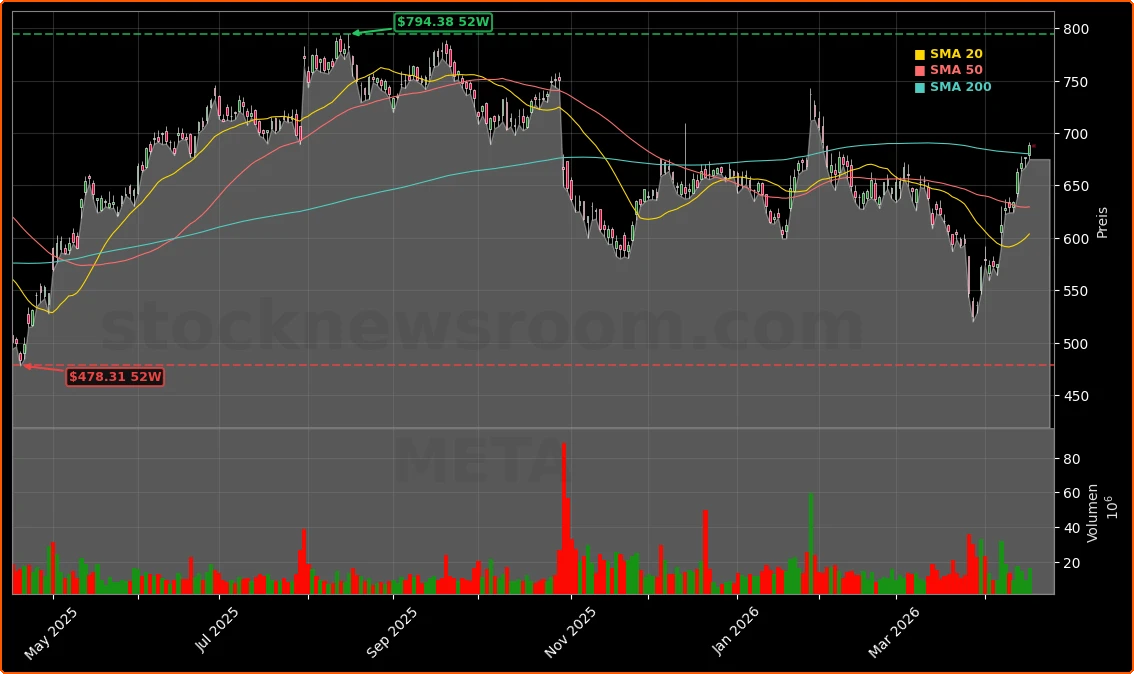

Meta shares closed Friday at $688.55, up 1.73% on the day and modestly softer in after-hours trading. The stock remains one of the strongest performers among the so‑called Magnificent Seven, helped by a rebound in large‑cap tech and renewed enthusiasm for AI infrastructure. With the Meta AI Layoffs, management is signaling that the next phase of upside will be driven less by headcount growth and more by capital-intensive AI bets and operating leverage.

Internally, about 10% of jobs – close to 8,000 positions worldwide – are expected to be eliminated starting May 20, with another wave of reductions possible in the second half of 2026. Executives are framing the cuts as part of a shift to flatter hierarchies and AI-augmented workflows rather than a reaction to financial stress. In 2025 Meta generated more than $200 billion in revenue and about $60 billion in profit, so the Meta AI Layoffs are about reallocation of resources, not survival.

For Wall Street, the message is clear: Meta wants to sustain high margins while plowing unprecedented capital into AI. That combination could support earnings per share even if AI revenue takes years to fully materialize.

How big is Meta’s AI spending pivot?

Zuckerberg is committing hundreds of billions of dollars over several years to build out AI infrastructure, including custom data centers, in‑house large language models and a superintelligence lab. Estimates around $600 billion in total AI-related capex underscore why the Meta AI Layoffs are being used to offset ballooning infrastructure costs.

Meta has already rolled out its own large language model efforts and introduced early products such as its Muse Spark model, while reorganizing parts of the Reality Labs segment into an “Applied AI” unit. That group is tasked with building AI agents that can autonomously code and handle complex workflows, potentially shrinking the need for certain developer and support roles over time. Some staff are also being reassigned into a new Meta Small Business unit to commercialize AI tools for advertisers and merchants.

The company is not building this AI stack alone. Meta has inked sizeable chip and cloud deals with AMD and CoreWeave, mirroring how rivals like NVIDIA and Apple leverage specialized partners. Recent commentary from firms such as Bernstein on Advanced Micro Devices highlights Meta as a key demand driver for next‑gen AI accelerators, reinforcing that Meta’s capex plans are now central to the broader semiconductor and AI‑cloud ecosystem.

What do Meta AI Layoffs mean for AI partners?

The Meta AI Layoffs occur against a backdrop of intensifying AI collaboration. AMD’s deepening partnership with Meta, including custom accelerators for next‑generation data centers, has been cited by Wall Street analysts as a pillar of AMD’s long‑term growth. At the same time, CoreWeave has secured multibillion‑dollar agreements with Meta, Anthropic and Jane Street, underscoring a shift where demand for high‑performance AI compute is diversifying beyond traditional hyperscalers.

For investors in chip names and AI‑infrastructure plays, Meta’s job cuts are unlikely to be a negative. If anything, they reinforce the idea that internal operating expenses will be squeezed to protect – or even expand – multi‑year commitments to AI hardware and cloud partners. That dynamic supports the broader tech rally that has lifted mega‑caps such as Tesla and other AI leaders this month.

Still, there are risks. Any slowdown in ad spending or regulatory setbacks, including ongoing social‑media lawsuits over mental health and youth harm, could make the AI investment cycle look more stretched. In addition, recent insider selling – like director Robert Kimmitt’s sale of a small number of shares under a 10b5‑1 plan – reminds investors that even insiders are taking some profits after the stock’s powerful run.

Is Meta still a value play in big tech?

Despite its rally, Meta trades at around 21 times forward earnings, making it one of the cheaper names among the Magnificent Seven peer group. That valuation, combined with strong free cash flow and high historical return on invested capital (ROIC), is a core part of the bull case. Every prior downcycle in ROIC has eventually been followed by improving returns and renewed share price strength as new products such as Stories, Reels and messaging ads scaled.

Many institutional investors now see AI as the next iteration of that playbook. The Meta AI Layoffs are intended to protect margins while Meta spends heavily on data centers, custom chips and new AI‑powered ad formats that could raise pricing and improve targeting. If AI tools successfully boost advertiser ROI and if Meta monetizes its models through developer access and small business offerings, today’s investments could support another multi‑year leg of earnings growth.

Consensus on Wall Street remains broadly constructive. Large banks such as Goldman Sachs and Morgan Stanley have highlighted Meta as a key AI beneficiary in recent tech sector notes, even as they caution that volatility is likely during this build‑out phase. For long‑term portfolios, the combination of cost discipline, strong balance sheet and underappreciated AI optionality keeps Meta in the conversation as a core NASDAQ holding.

Related Coverage

For a deeper dive into how Meta’s chip partnerships with Broadcom and AMD fit into the broader capex story, read Meta AI Strategy Boom: Broadcom and AMD Bets Shake Up AI Chips, which examines whether these supplier bets can turn massive spending into a durable competitive edge. Investors interested in the wider AI defense and software landscape can also look at Palantir AI Defense +70% Boom: Can This 2.5% Surge Last? for context on how other high‑growth AI names are navigating valuation and growth expectations.

In summary, the Meta AI Layoffs underscore a deliberate shift from headcount-heavy growth to capital-heavy AI investment, with management betting that automation and infrastructure will drive the next wave of profitability. For investors, Meta remains a relatively inexpensive way to gain exposure to large‑scale consumer social platforms and the AI infrastructure boom. The coming quarters will show whether this new “efficiency 2.0” era can convert historic AI spending into sustained earnings growth and justify Meta’s central role in tech-heavy portfolios.