Can Meta’s aggressive AI chip deals with Broadcom and AMD turn massive capex into a durable competitive edge in the AI race?

How is Wall Street reacting to Meta’s AI push?

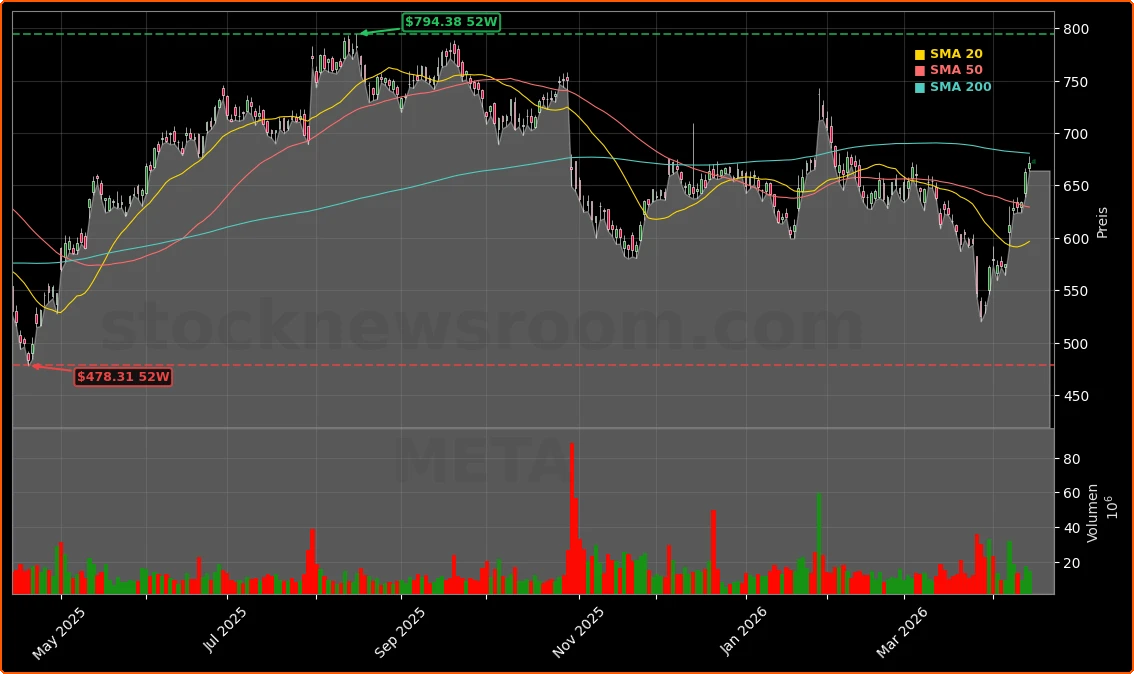

Meta shares have rebounded sharply from their late‑March lows, gaining roughly 28% since March 27 and closing Wednesday at $671.58, with a modest after‑hours uptick to $673.80. The stock’s recovery comes as investors reassess concerns about Meta’s aggressive hiring of AI talent and soaring capital expenditures. The company’s new Muse Spark model, the first output from its Meta Superintelligence Lab led by Alexandr Wang, is a key proof point that the spending is starting to ship product. While Muse Spark generally trails the very best models from OpenAI, Anthropic and Alphabet’s Google on benchmarks, Meta’s ability to control both the model and the hardware stack is central to the Meta AI Strategy.

Broadcom, a critical partner in that stack, rallied 4.20% on Wednesday to $396.72 before easing slightly after hours. The jump reflects growing confidence that hyperscaler AI spending by Meta, Apple, Microsoft and others will increasingly favor custom silicon over off‑the‑shelf GPUs from incumbents such as NVIDIA.

How crucial is Broadcom to Meta’s AI infrastructure?

Meta and Broadcom have extended their existing AI chip partnership through 2029 in a multi‑year, multi‑generation deal focused on Meta Training and Inference Accelerator (MTIA) processors. These custom accelerators will form the backbone of Meta’s next‑generation AI data centers, powering features across WhatsApp, Instagram, Facebook and Threads. The initial commitment exceeds 1 gigawatt of AI compute, with a roadmap to scale to multiple gigawatts over time, underlining how capital‑intensive the Meta AI Strategy has become.

Broadcom will not only supply accelerator technology—targeting cutting‑edge 2‑nanometer process nodes—but also advanced Ethernet networking to connect MTIA clusters at massive scale. Morningstar reiterated its bullish view on Broadcom after the announcement, arguing that the Meta deal reinforces its thesis of rapid XPU (accelerator) growth through 2030. Deutsche Bank’s Ross Seymore kept a buy rating and a $430 price target on Broadcom, while Bernstein’s Stacy Rasgon maintained an outperform rating with a $525 target, both highlighting the strategic value of long‑term AI supply agreements with Meta, Google and Anthropic.

The closer business ties also prompted governance changes: Broadcom CEO Hock Tan is stepping off Meta’s board to avoid conflicts as the commercial relationship deepens, while remaining closely involved on chip strategy in an advisory role.

Where does AMD fit into the Meta AI Strategy?

Meta is also diversifying away from single‑vendor dependence by committing to advanced GPUs from AMD. Under recently signed agreements, AMD will provide Meta and OpenAI with up to 6 gigawatts of GPU capacity, starting with its upcoming MI450 accelerators. For AMD, long seen as lagging NVIDIA on AI software, the deals force Meta and OpenAI to integrate its ROCm software stack deeply into their ecosystems, a critical step toward closing the CUDA gap.

These arrangements include warrants for up to 10% of AMD’s equity for each partner, vesting only if the stock reaches pre‑agreed thresholds. That structure directly aligns Meta’s incentives with AMD’s long‑term success: if Meta can successfully scale AMD hardware alongside Broadcom’s MTIA chips, it gains leverage over pricing while potentially benefitting from appreciation in AMD’s share price. For investors, the takeaway is that the Meta AI Strategy is explicitly multi‑vendor, using both custom accelerators and merchant GPUs to secure capacity in an environment where AI demand frequently outstrips supply.

Does Muse Spark change the earnings equation?

Muse Spark, the flagship model from Meta’s Superintelligence Lab, may not be the most powerful model globally, but management claims it delivers comparable capabilities to Meta’s prior Llama 4 Maverick with over an order of magnitude less compute. In practical terms, Meta says it can match previous performance using roughly 10% of the inference cost. That efficiency is crucial when the company is already spending tens of billions of dollars per year on capex and aims to scale AI features to billions of users.

The model is expected to drive better ad targeting, higher engagement and new automation tools, including a “full‑service” advertising agent for small businesses. The concept: a bakery or local retailer can let AI handle creative, copy and optimization across Meta’s apps with minimal human input. Similar to the AI Overviews rollout that helped accelerate ad revenue growth at Alphabet, more capable and cheaper models could allow Meta to expand AI‑powered surfaces without crushing its margins.

Jim Cramer and other market commentators have argued that the strong share‑price rebound suggests investors are increasingly comfortable that the AI hiring spree and capex surge can translate into higher free cash flow once these systems are scaled. At around 21.5x forward earnings estimates, Meta’s valuation still looks reasonable compared to fast‑growing AI peers in the NASDAQ 100.

How is the EU challenging Meta’s WhatsApp AI plans?

Regulatory pressure is the main counterweight to the Meta AI Strategy. The European Commission signaled plans to impose interim measures ordering Meta to roll back a WhatsApp business policy that effectively banned third‑party, general‑purpose AI chatbots from interacting with users on the messaging platform starting January 2026. Brussels argues that Meta may be abusing its dominant position in messaging by restricting rival AI assistants, potentially harming competition in the broader AI assistant market while favoring Meta’s own bots and models like Muse Spark.

Meta recently proposed allowing rival AI assistants onto WhatsApp for a fee, but EU officials indicated that does not fully address their concerns. A WhatsApp spokesperson pushed back, warning that forcing free access could leave small paying businesses effectively subsidizing large AI labs such as OpenAI. For investors, the probe underscores that any attempt by Meta to tightly integrate proprietary AI into WhatsApp and Messenger will be closely watched—and possibly constrained—by regulators in Europe and other key markets.

Related coverage

For a deeper dive into how Meta’s capex explosion underpins its broader AI agenda, including the Muse Spark rollout and data center buildout, read Meta AI Strategy Boom: $135B Capex Bet Shocks Wall Street. The piece explores whether this unprecedented spending cycle can transform short‑term margin pressure into long‑term growth. To put Meta’s valuation and risk profile into a broader AI context, see Palantir AI Valuation +4.9% Surge: Bubble or Justified?, which analyzes how far investors are willing to stretch multiples for high‑growth AI names compared with mega‑caps like Meta and Tesla.

As we roll out more than 1GW of our custom silicon to start and then multiple gigawatts over time, this partnership will give us greater performance and efficiency for everything we’re building.— Mark Zuckerberg, CEO of Meta Platforms

Overall, the Meta AI Strategy now rests on three pillars: custom MTIA chips with Broadcom, scaled GPU partnerships with AMD and more efficient in‑house models like Muse Spark, all while regulators test the limits of its power in messaging. For long‑term investors, the key will be whether these infrastructure bets can keep driving ad revenue and new AI services faster than capex and compliance costs rise. The next few quarters of product launches, regulatory decisions and capex guidance will show whether Meta can convert today’s billion‑dollar AI commitments into tomorrow’s durable earnings streams.