Is the MicroStrategy Bitcoin Strategy turning a software company into Wall Street’s most aggressive leveraged BTC proxy play?

Is MicroStrategy reshaping the Bitcoin proxy trade?

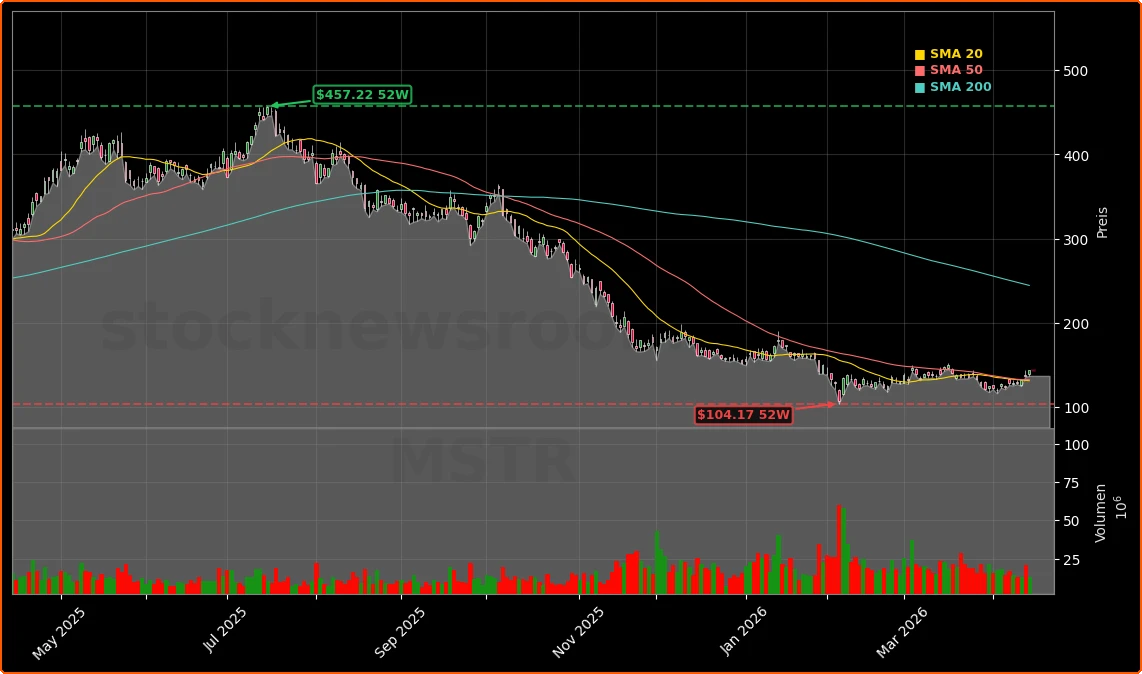

MicroStrategy Incorporated closed Wednesday at $143.54, up 4.45% on the day, with only a marginal move in after-hours trading. The stock remains highly correlated with Bitcoin, functioning for many U.S. traders as a high-beta proxy for BTC exposure on the NASDAQ rather than on a crypto exchange. The renewed rally in both Bitcoin and MSTR follows the latest leg of the MicroStrategy Bitcoin Strategy: a massive new accumulation of 13,927 BTC between April 6 and April 12 at an average price of $71,902 per coin, funded entirely through preferred stock.

That purchase, on top of a prior weekly buy of 4,871 BTC for about $330 million, has pushed the company’s total holdings to 780,897 BTC at an average cost of roughly $75,577. When Bitcoin bounced back to around $75,600 on April 14, the position moved back into the green on paper for the first time since early January, erasing a large portion of the roughly $14.46 billion unrealized loss reported for Q1 2026.

How is MicroStrategy funding its BTC buying spree?

The most controversial evolution in the MicroStrategy Bitcoin Strategy is how the company is raising capital. Instead of issuing new common stock and diluting existing shareholders, the latest $1 billion tranche of Bitcoin was financed through the sale of 10 million shares of STRC, a preferred stock paying an 11.5% annual dividend and trading around $100 par. Investors in STRC receive high-yield income, while MicroStrategy channels the proceeds almost directly into additional Bitcoin purchases.

Trading activity shows strong demand for this structure: STRC reached about $1.156 billion in daily trading volume on April 13, closing near par with virtually no price volatility. As long as STRC trades at or above $100, MicroStrategy can continue issuing new preferred shares and scaling its Bitcoin bet without further diluting common equity. That design is central to why some on Wall Street see MSTR as a structured Bitcoin fund wrapped inside an enterprise software company.

Does the MicroStrategy Bitcoin Strategy have more firepower?

Management has signaled an ambition to reach 1 million BTC by the end of 2026. With 780,897 BTC already on the balance sheet, that implies acquiring another ~219,000 BTC over the next eight quarters. The company still has about $21.6 billion of STRC and roughly $27.1 billion of authorized but unused MSTR common stock it could tap, giving it theoretical capacity to deploy close to $49 billion into Bitcoin at current market levels.

That scale makes MicroStrategy one of the most aggressive corporate treasury players in global markets, drawing comparisons with crypto-heavy strategies at firms like Tesla and, on a different asset base, NVIDIA’s AI-driven capital allocation in chips. However, unlike Apple or other mega-cap tech names that prioritize cash flexibility and buybacks, MicroStrategy is effectively transforming its balance sheet into a leveraged Bitcoin ETF with operating software revenue attached.

How are analysts and insiders reacting?

Not all on Wall Street are convinced this ends in shareholder value creation. TD Cowen recently cut its price target on MSTR by 20% to $350, reflecting growing concern over volatility, balance sheet risk, and the sustainability of double-digit preferred dividends if Bitcoin stagnates or enters a prolonged bear market. Trade ideas on platforms like TradingView highlight that MSTR remains a high-risk, high-reward vehicle, with technicians pointing to sharp drawdown potential if BTC revisits recent lows near $60,000.

Insider activity has also drawn attention. Multiple Form 144 filings in late March and early April detail proposed and completed open-market sales of Class A shares by insider Jarrod M. Patten, involving several thousand shares across multiple sessions. While such transactions are often tied to compensation and diversification, they serve as a reminder that senior insiders are trimming exposure even as the corporate balance sheet doubles down on Bitcoin.

What does this mean for U.S. investors?

For American investors, the MicroStrategy Bitcoin Strategy effectively offers leveraged, equity-based exposure to Bitcoin with additional layers of risk and reward. Unlike spot Bitcoin ETFs, MSTR carries operating business fundamentals, preferred dividend obligations, and equity dilution levers. The stock’s sharp swings, coupled with substantial unrealized gains and losses tied to BTC, mean position sizing and risk management are critical.

ETF screens on NASDAQ-listed funds show MSTR appearing as a concentrated position in several thematic and high-beta vehicles, further amplifying its influence on crypto-linked equity baskets. For traders accustomed to speculative growth names like Tesla or high-volatility chip leaders such as NVIDIA, MSTR fits naturally into a satellite allocation rather than a core S&P 500-style holding.

Related Coverage

For a deeper dive into how the preferred stock structure underpins recent BTC purchases, readers can review “MicroStrategy Bitcoin Financing Soars +5.3% on STRC Boom”, which analyzes whether STRC-fueled buying can continue without destabilizing the balance sheet. Investors interested in how aggressive crypto-treasury bets can backfire may also want to examine “BitMine Ethereum Treasury burns billions: $3.8 billion quarterly loss shocks crypto investors”, a cautionary case study of a leveraged Ethereum strategy gone wrong.

In summary, the MicroStrategy Bitcoin Strategy has entered a new chapter, pairing a fresh $1 billion BTC purchase with an innovative preferred-stock funding model that protects common shareholders from further dilution. For U.S. investors, MSTR remains a speculative, high-octane way to play Bitcoin’s long-term trajectory, with TD Cowen’s reduced $350 target underscoring the tension between upside potential and downside risk. The next major moves in both Bitcoin and MicroStrategy’s capital-raising plans will determine whether this bold approach becomes a landmark success story or a warning for future corporate treasurers.