Can Apple’s edge-focused AI strategy and new Mac designs really reignite growth, or is the latest rally running ahead of reality?

How does Apple’s rally fit into Big Tech’s AI trade?

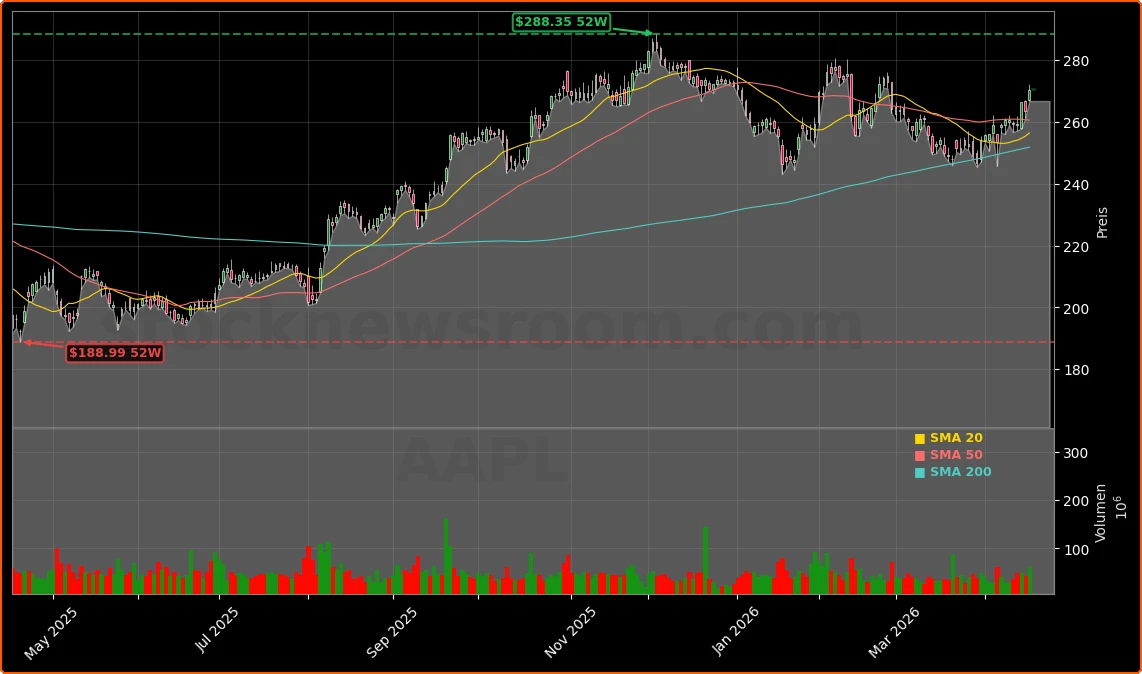

Apple Inc. closed Friday’s regular session at $270.23, up 2.59%, and inched higher after hours to $270.60. The move came alongside gains in the Magnificent Seven, with Tesla and others also pushing the major indexes higher. At this level, Apple trades roughly in the middle of its 52‑week band of $189.81 to $288.62, leaving room both to retest last year’s highs and to disappoint if the Apple AI Strategy fails to deliver visible monetization.

On the technical side, Apple is trading modestly above its 20‑day simple moving average and slightly below its 100‑day, while a positive MACD setup points to improving upside momentum. Analysts at Bank of America, led by Wamsi Mohan, reiterated a Buy rating and a $325 price target, calling Apple the “ultimate edge AI play” as its silicon and device ecosystem increasingly prioritize on‑device intelligence over pure cloud compute.

Institutional positioning remains heavy but mixed. Recent 13F filings show some managers trimming exposure while others add. For instance, Global Trust Asset Management and Cypress Funds have reduced stakes, while OAKMONT Corp, AdvisorNet Financial and C2P Capital Advisory Group have increased their Apple holdings, reflecting differing views on how quickly AI and new form factors can reaccelerate growth.

What defines the current Apple AI Strategy?

The Apple AI Strategy is tilting decisively toward edge AI, with the M5 chip family at the center. Bank of America’s Mohan describes the expanded M5 lineup as a “meaningful step” toward a self‑sustained AI compute stack, designed to run advanced models directly on iPhones, iPads and Macs. That approach contrasts with hyperscaler strategies from NVIDIA and cloud players, which monetize primarily via data center GPUs and services.

Rather than chasing headline‑grabbing chatbots, Apple is focusing on deeply embedding generative and predictive features into iOS, iPadOS and macOS. A refreshed Siri, context‑aware app suggestions, on‑device content creation and smarter notifications are expected to roll out in waves, likely showcased at upcoming WWDC events. The company is also pursuing a multi‑model approach, integrating external AI platforms such as Google Gemini and OpenAI tools where they add value, while still controlling the user experience at the OS level.

This hybrid stack — Apple silicon plus third‑party models — fits its long‑standing playbook: let competitors race ahead with early versions, then ship a more polished, privacy‑centric implementation at scale. For investors, the open question is how much incremental revenue these AI features can unlock in Services and hardware upgrades versus being treated as table stakes.

Can Macs and MacBook Neo turn design into AI advantage?

The new fanless MacBook Neo illustrates how Apple’s silicon and design philosophy can reinforce its AI ambitions. By pairing a highly efficient A18 Pro‑class chip with passive cooling, Apple is reviving Steve Jobs’s long‑held dream of silent, appliance‑like computing — a dream that failed dramatically with the overheating Apple III but is now technically viable.

The MacBook Neo’s architecture, closely aligned with the broader Apple silicon roadmap, should allow the same neural engines and acceleration blocks powering mobile AI features to appear in laptops. That consistency across devices matters as Apple looks to keep users inside its ecosystem for AI‑assisted workflows ranging from productivity and media editing to fitness and health. The company’s fast‑growing Services segment, including high‑margin offerings like Apple Fitness, stands to benefit if AI‑enhanced experiences drive higher engagement and cross‑selling.

At the same time, Apple continues to prioritize quality over low‑end volume. The Mac Neo underscores a willingness to sacrifice some market share in favor of margin‑accretive, premium hardware — a stance that could pay off if AI features become a primary differentiator in the high‑end PC and tablet market.

How do China and foldables factor into growth?

Despite a 4% year‑over‑year decline in China’s overall smartphone shipments in Q1 2026, Apple posted the fastest growth among major vendors there, helped by premium positioning, AI‑ready devices and trade‑in programs that encourage upgrades. More broadly, Apple has emerged as the leading global smartphone vendor in early 2026, the only top‑five manufacturer to increase shipments as the market contracted. That outperformance supports the thesis that AI‑enabled premium phones can still grow even when the mass market struggles.

Rising memory and component costs are pressuring mid‑range Android rivals and reshaping OLED demand, pushing OEMs to focus more on premium tiers. Apple and Samsung are leveraging this to consolidate share at the high end, where foldables and AI features command higher average selling prices.

On that front, expectations are mounting for a foldable iPhone, likely around 2026. Investors will be watching whether Apple can pair the new form factor with compelling AI‑driven experiences — such as dual‑screen productivity, advanced camera computation and spatial computing features — rather than simply matching hardware specs from Samsung, Motorola and Google. A successful foldable could extend the iPhone replacement cycle and deepen loyalty inside the Apple ecosystem.

What about regulation, leadership and competition?

Apple also scored a notable legal win as the U.S. International Trade Commission declined to revisit an earlier ruling that cleared redesigned Apple Watch models of infringing Masimo’s blood‑oxygen patents, ending the latest bid to reinstate an import ban. That removes a near‑term overhang on Apple’s wearables business, which will be another important surface for subtle, always‑on AI features.

Longer term, leadership transition looms in the background. Tim Cook, widely praised for his stewardship of margins, capital returns and supply chains, is expected by some observers to step down around 2028. The next generation of executives will be judged far more on product and AI innovation — from spatial computing to wearables and new input devices — than on financial engineering.

In the broader AI race, Apple faces intense competition from NVIDIA, Microsoft, Alphabet and others that monetize AI through cloud infrastructure and software. Where peers emphasize compute scale, the Apple AI Strategy leans into privacy, vertical integration and a 2‑billion‑device installed base. That difference could either prove a defensible niche or a missed opportunity if services revenue fails to inflect.

Related Coverage

For a deeper dive into how delays to Cupertino’s first foldable and a late AI pivot could affect valuation, see this analysis of Apple’s foldable warning, delay risks and AI pivot. It explores whether new form factors and AI‑enhanced services can truly fuel the next growth leg for the stock.

Investors following the AI hardware supply chain should also read our NVIDIA revenue surge and AI boom forecast, which examines whether Wall Street’s expectations for the GPU leader are still too conservative given current spending trends. Together, these pieces frame how device‑side AI at Apple intersects with data center AI demand at key suppliers.

In summary, the Apple AI Strategy is shifting the company from perceived AI laggard to a focused edge‑intelligence ecosystem player. For investors, the key will be whether M5‑class chips, MacBook Neo and a potential foldable iPhone translate AI capabilities into higher ASPs and Services growth. The next WWDC cycles and product launches will show whether this strategy can sustain Apple’s premium multiple on the NASDAQ and within the S&P 500.