Can Meta’s massive AI infrastructure gamble turn today’s cash cow into tomorrow’s dominant platform, or is it overbuilding into an AI bubble?

Is Meta spending too much on AI build‑out?

Meta Platforms, Inc. is deep into an aggressive AI investment cycle, with combined hyperscaler capital expenditure from Meta, Alphabet, Amazon and Microsoft expected to approach roughly $725 billion in 2026. Management has explicitly framed the Meta AI Infrastructure program as a “spend now or fall behind” decision, arguing that underinvestment is riskier than overshooting on capacity. In its latest quarter, Meta delivered about 24% year‑on‑year revenue growth and roughly 41% operating margins, but guided 2026 operating expenses about 40% higher, largely tied to AI and infrastructure. That guidance helped trigger a 13% share pullback in Q1 as portfolio managers questioned whether the return profile is as attractive as at rivals like NVIDIA or Alphabet.

Despite the higher cost base, Meta continues to generate strong cash flow from its core advertising franchises in Facebook, Instagram and WhatsApp. Investors focused on the long term point to growing AI‑driven engagement — more relevant content recommendations and better ad conversion — as early evidence that the Meta AI Infrastructure outlay is already supporting the core business. Baron Capital’s Durable Advantage Fund, for example, highlighted rising time spent and improved ad ranking as tangible benefits from Meta’s AI models, even as macro uncertainty and geopolitical tensions weighed on digital ad budgets.

How is Meta securing chips, cloud and power?

A key pillar of Meta AI Infrastructure is access to compute. Meta is both buying advanced servers based on NVIDIA GPUs and ARM‑based chips, and signing large third‑party cloud and colocation deals. One standout agreement is a long‑term contract with Nebius, under which Nebius will provide up to $27 billion worth of AI computing capacity over five years. Nebius has reported that major orders from Meta and Microsoft left its data‑center capacity fully booked through at least the first quarter, underlining the intensity of hyperscaler demand.

The infrastructure build‑out doesn’t stop at servers. AI data centers are enormous power consumers, and Meta has joined other hyperscalers in locking in long‑term electricity supply, including nuclear power agreements. Utilities such as Vistra have cited Meta power purchase deals as part of their growth strategy, while Constellation Energy and others are restarting or expanding nuclear assets to meet AI‑driven load. At the political level, this surge in electricity demand has drawn scrutiny: Senator Elizabeth Warren has criticized Meta, Amazon, Google and Microsoft for driving grid upgrades that could raise residential bills, and has opened an investigation into how utilities allocate these costs.

Where does Meta AI Infrastructure show up in products?

Beyond back‑end capex, Meta AI Infrastructure underpins a growing portfolio of models and services. The company has released the open‑source Llama 2 large language model family and continues to develop internal systems like the Spark platform for generative and recommendation AI. These models power content moderation, personalized feeds and ad targeting across Facebook and Instagram, and are increasingly central to Meta’s Metaverse ambitions, including smart glasses and virtual assistants.

New monetization layers are also emerging on top of this stack. Meta is rolling out WhatsApp Plus, a €2.49 per month paid add‑on with extra features, as it tests subscription revenue alongside advertising. AI‑driven business messaging, commerce and creator tools could all benefit from the same Meta AI Infrastructure, potentially expanding margins over time if unit economics scale. Competitively, Meta is racing against Apple and Google, which are embedding generative AI more deeply into mobile operating systems, while Tesla and others push AI into physical products like autonomous driving and robotics.

What are the regulatory and geopolitical risks for Meta?

The build‑out of Meta AI Infrastructure is unfolding amid intensifying regulatory and geopolitical scrutiny. Meta recently lost a jury verdict related to user harm tied to product design, adding to a complex global legal backdrop that already includes privacy, antitrust and content moderation challenges. Higher AI usage could invite additional questions from regulators about algorithmic transparency and mental‑health impacts, especially as recommendation engines become more powerful.

On the geopolitical front, Meta’s leadership is set to join executives from Apple and Tesla on President Trump’s upcoming trip to China, underscoring how critical the Chinese market and supply chain remain for U.S. tech giants. One focal point is Beijing’s stance on cross‑border AI deals, with Meta reportedly interested in pushing back against moves to block certain transactions. Any easing of AI export or cooperation restrictions could alter the demand outlook for chips and data centers, including those supplied by NVIDIA, while a hardening stance would reinforce the need for domestic and allied‑nation capacity — making Meta AI Infrastructure even more strategically important.

How should investors view Meta’s valuation now?

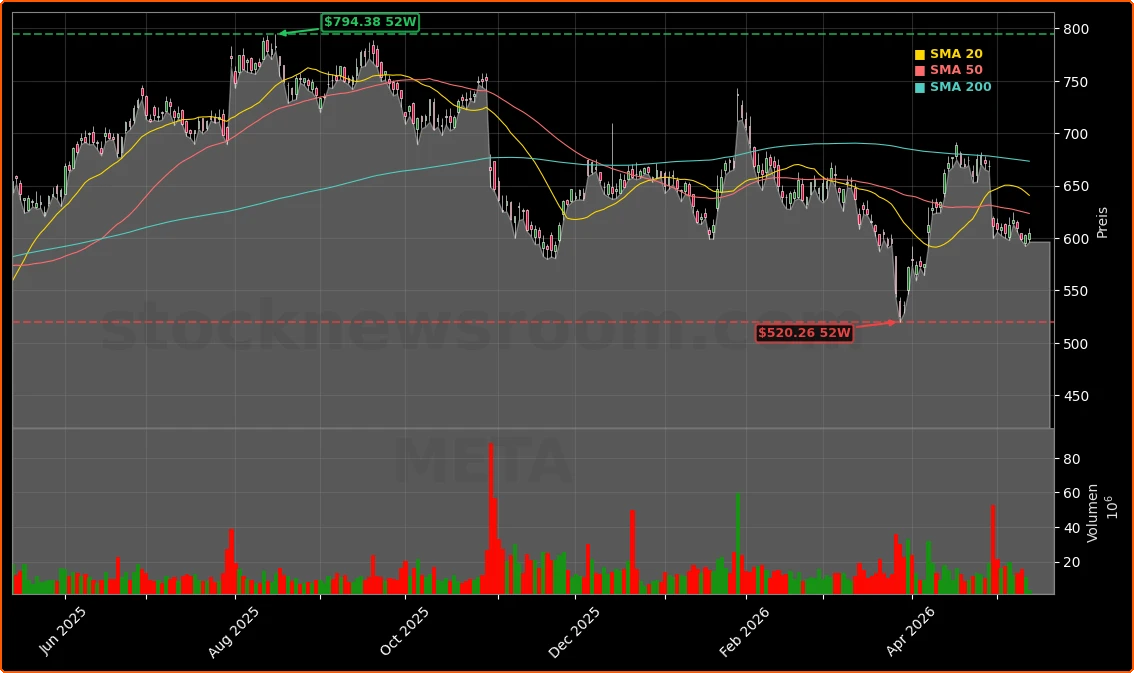

At about $605 per share and a market cap near $1.5 trillion, Meta remains one of the largest names in the S&P 500 and NASDAQ. The stock is off roughly high‑single‑digits over the last 12 months, reflecting a reset after a powerful multi‑year rally. Some institutional holders, including Danske Bank, have modestly trimmed positions, while CEO Mark Zuckerberg recently reported an internal transfer of Class B shares, keeping voting control unchanged. Options markets are pricing for a potential move toward the $640 area in the coming months, in line with structured products that cap upside but benefit from moderate gains.

Sell‑side opinion is mixed but generally positive: large banks such as Goldman Sachs and Morgan Stanley have emphasized Meta’s durable ad moat and AI upside, while also flagging that any further step‑up in capex or operating expenses could pressure near‑term multiples. For U.S. investors, the central question is whether Meta AI Infrastructure will translate into sustained, above‑market earnings growth or whether the company is at risk of overspending relative to peers.

Related Coverage

For a deeper dive into how this investment wave fits into Meta’s broader strategy, readers can review our recent analysis in “Meta AI Strategy Record Spend vs. Profit Boom Warning”, which examines whether record AI spending and job cuts can deliver durable profit growth or if Wall Street’s caution is justified.

Meta AI Infrastructure is rapidly becoming the backbone of Meta’s growth story, linking its ad engine, Metaverse ambitions and new subscription products into a single, capital‑intensive platform. For long‑term investors, the stock now represents a high‑conviction bet that these AI and data‑center investments will outpace rising energy, regulatory and capex headwinds. The next few quarters of execution and guidance will be crucial in proving that Meta AI Infrastructure can convert today’s massive spending into tomorrow’s sustainable earnings power.