Can AMD’s AI growth story still justify its premium valuation after a sharp sell-off rattled semiconductor investors?

Is AMD’s AI Growth Outpacing Its Valuation Risk?

Advanced Micro Devices, Inc. trades at a staggering 179.8x trailing P/E — nearly 7x the S&P 500 median — and a 24.0x price-to-sales ratio versus the index’s 3.4x. That premium reflects Wall Street’s conviction in its AI narrative: Data Center revenue hit $5.78 billion in Q1 2026, up 57% YoY and now the company’s primary earnings driver. Yet with forward EPS at just $6.87, reaching $1,000 per share by 2031 would require either aggressive multiple expansion or sustained, above-consensus earnings acceleration. Goldman Sachs’ $650 target implies 26% upside from current levels — but the firm holds 12 million AMD shares, raising questions about alignment. Meanwhile, the consensus analyst target remains at $508.31, below today’s price — and zero sell ratings exist among 51 total ratings (5 Strong Buys, 37 Buys, 9 Holds).

How Is AMD AI Forecast Shaping Hyperscaler Commitments?

CEO Lisa Su highlighted concrete wins driving the AMD AI Forecast: a 6GW OpenAI GPU deployment, a major Meta MI450 commitment, and an Oracle supercluster rollout. These are not theoretical — they’re revenue-generating contracts accelerating AMD’s transition from CPU challenger to AI infrastructure partner. Still, AMD remains behind NVIDIA in AI chip share, with analysts noting its MI308 export restrictions to China ($440 million in FY2025 charges) limiting near-term upside. While Meta and Oracle deepen ties, Microsoft and Google continue prioritizing NVIDIA’s Blackwell architecture — a competitive reality that tempers bullishness. The AMD AI Forecast assumes hyperscaler wins convert into recurring, high-margin revenue — but gross margins on new AI GPUs are currently below corporate average, pressuring near-term profitability.

Why Is the Semiconductor Sector Dragging AMD Down?

Advanced Micro Devices, Inc. fell alongside Micron, Intel, and Broadcom as global chipmakers sold off following Samsung Electronics’ 8% post-earnings drop — despite a 19-fold profit surge. That disconnect underscores investor fatigue: even stellar results can’t offset concerns about AI capex sustainability. The SMH Semiconductor ETF broke its uptrend, and sector rotation into defensives has accelerated. With a beta of 2.469, AMD is especially vulnerable to sentiment shifts. U.S. equity futures slid as chip stocks led losses, and AMD’s volume has softened slightly above $500 — a technical warning sign for momentum traders. This isn’t isolated weakness: Intel plunged 10.2%, and Broadcom slid 1.4%, confirming broad-based pressure. The AMD AI Forecast assumes continued AI infrastructure spend — but if hyperscalers pause deployments, AMD feels it first.

What Do Insider Trades and Margin Pressures Signal?

Ninety-two recent insider transactions — net selling — raise eyebrows amid the rally. While CEO Lisa Su and other executives continue to buy selectively, the overwhelming net outflow suggests internal caution. Management also confirmed it expects second-half gaming revenue to decline more than 20% versus H1 and plans for lower PC shipments — segments that still contribute meaningfully to cash flow. Worse, new AI GPU sales carry lower gross margins, threatening to dilute overall profitability even as top-line growth accelerates. This tension — between explosive Data Center growth and eroding legacy margins — makes the AMD AI Forecast a high-wire act. For U.S. portfolios, AMD offers concentrated AI exposure — but at the cost of elevated volatility and single-stock risk versus diversified semiconductor ETFs.

Is This a Buying Opportunity or a Valuation Trap?

Data Center now the primary driver of our revenue and earnings growth.— Lisa Su, CEO of Advanced Micro Devices, Inc.

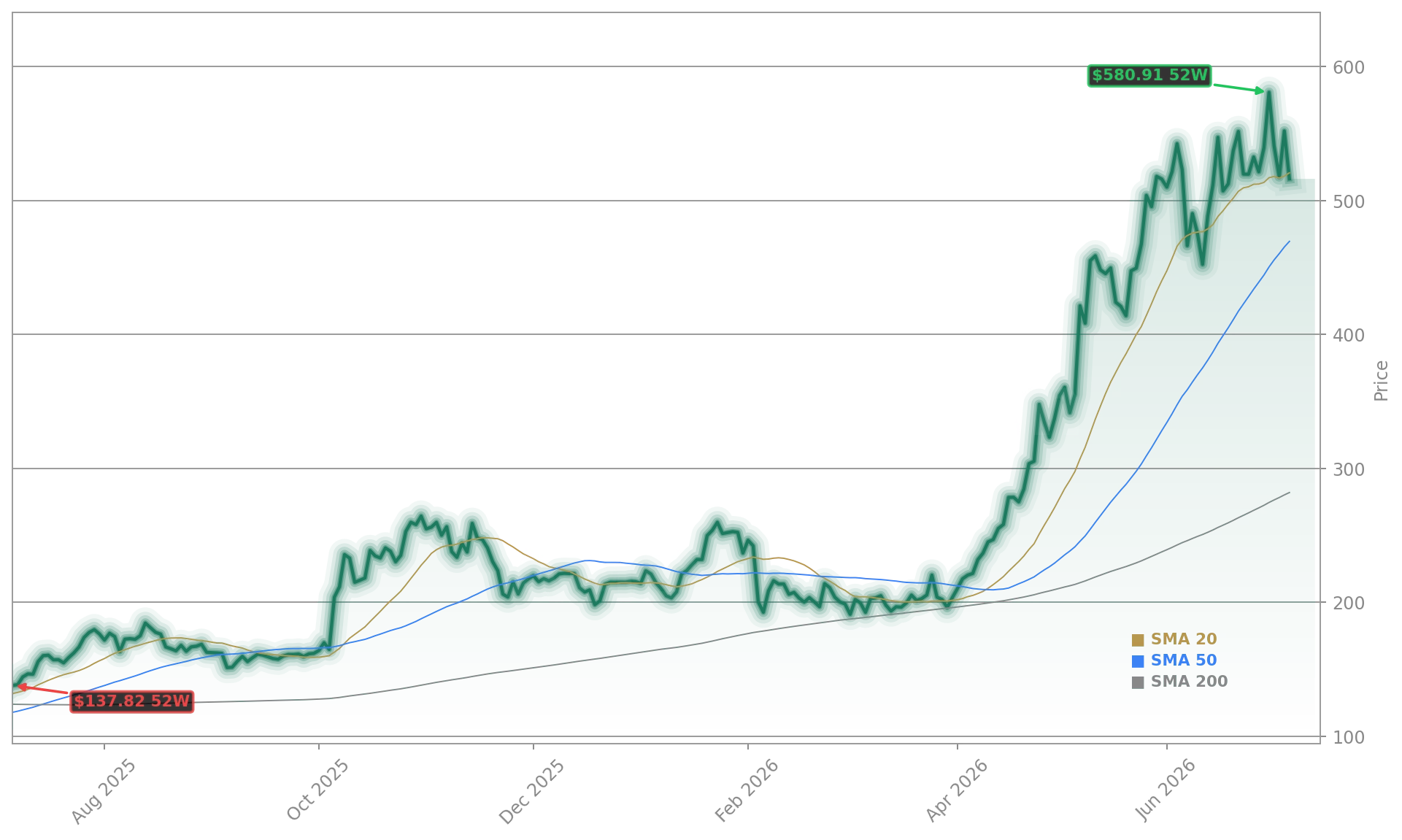

At $515.48, AMD sits just above the psychologically critical $500 level — a zone analysts cite as a potential demand zone for directional calls. But technicals alone won’t override fundamentals. RBC Capital Markets recently reiterated its ‘Outperform’ rating, citing AI pipeline visibility, while Morgan Stanley notes the stock’s “narrow valuation window.” The bear case — $431.73 — assumes AI capex slows and margin pressure deepens. The base case — $708.19 — assumes steady execution. The bull case — $812.33 — depends on sustained 56% gross margins and hyperscaler monetization. With Q2 2026 earnings due in August, the next catalyst is clear: can AMD reaffirm its AI leadership — or will valuation concerns dominate?