Is Micron’s explosive pricing power finally turning the Micron Forecast into Wall Street’s next major semiconductor breakout story?

Why Is Micron Forecast So Aggressively Upgraded?

Wall Street’s latest wave of price target hikes isn’t speculative — it’s data-driven. Wedbush analysts reported that DRAM and NAND average selling prices rose by “high double to even triple digits” in Q2 2026, far exceeding Micron’s prior guidance assumptions. Their updated Micron Forecast now models a 65% quarter-over-quarter pricing increase for both memory types in fiscal Q3 — up from 40% — citing early contract pricing advantages and stronger-than-expected demand from hyperscalers. Stiefel Securities followed with a $1,500 target, while Citigroup raised its target to $1,200. These aren’t isolated calls: 19 upward revisions have hit Micron in recent weeks, per Zacks Investment Research.

How Does Micron Compare to NVIDIA and Apple?

While NVIDIA remains the AI infrastructure bellwether, Micron Technology, Inc. is now the critical enabler — and its growth is accelerating faster. Fiscal Q2 2026 revenue hit $23.86 billion, up 270% year over year; DRAM revenue alone jumped 207%. That dwarfs Apple’s memory-related pricing pressure — which Apple recently cited to justify iPhone and Mac price hikes — and positions Micron as the direct beneficiary. Unlike cyclical peers, Micron’s exposure to high-bandwidth memory (HBM4) shipments and AI server modules means it’s no longer competing on cost, but on bandwidth, latency, and integration — a dynamic that mirrors NVIDIA’s own defensibility. Even Apple’s U.S. chip manufacturing pact with Intel indirectly validates Micron’s domestic capacity push.

What’s Driving the Micron Forecast Beyond AI?

The Micron Forecast isn’t just about AI data centers. Pent-up demand from smartphones and PCs — suppressed by memory shortages — is set to rebound, per IDC forecasts showing 14% smartphone sales decline in 2026 followed by recovery. Meanwhile, Micron’s $25 billion fiscal 2026 capital expenditure plan — up from $13.8 billion — is accelerating U.S. production: its Manassas, Virginia fab now manufactures 1-alpha DRAM, and its $200 billion U.S. investment across New York, Idaho, and Virginia is the largest private semiconductor buildout in American history. Yahoo Finance reports Micron has selected Bechtel to lead Phase One of its Clay, New York complex — a move directly tied to national supply chain resilience and Trump-era onshoring incentives.

Can Micron Forecast Sustain This Momentum?

Pricing for both NAND and DRAM in the second calendar quarter increased by ‘high double to even triple digits,’ exceeding the assumptions Micron used in its prior guidance.— Wedbush analysts

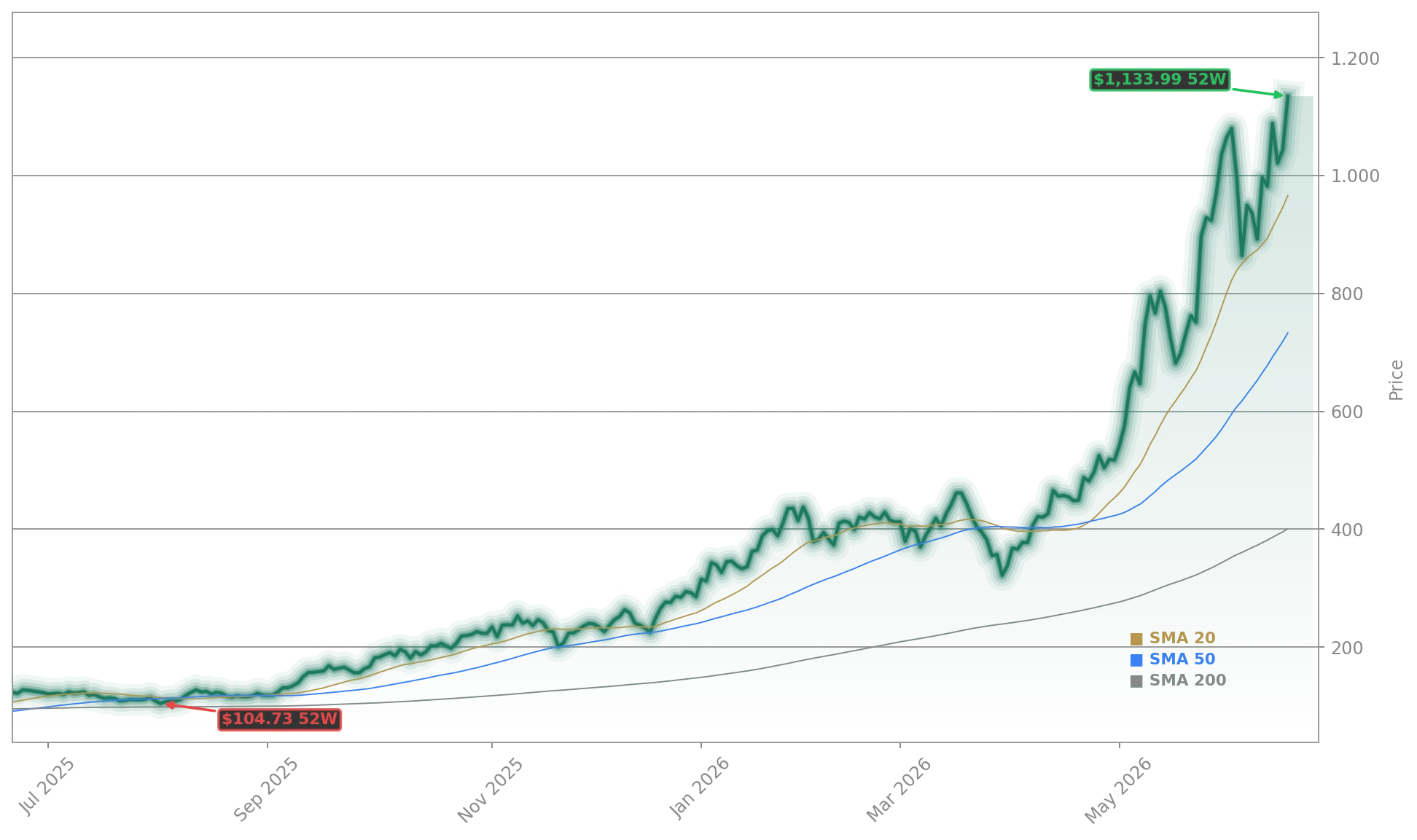

Yes — but volatility remains baked in. Micron has beaten earnings every quarter for the past two years yet rose post-earnings only once in the last six quarters, per TradingView. That suggests expectations are now stratospheric: a $1,500 target implies a $1.6 trillion market cap, pushing Micron past $1 trillion in valuation — a milestone that raises questions about sustainability. Yet SK Hynix itself forecasts memory bottlenecks lasting until 2030, with HBM demand growing 30% annually through the decade. Wedbush notes new supply will be rapidly absorbed — especially given HBM’s 4x wafer intensity versus conventional DRAM. With the Federal Reserve signaling potential 2026 rate hikes, Micron’s PEG ratio of just 0.33 (per Yahoo! Finance) may be its strongest buffer against macro headwinds.