Is this Micron Record just another chip rally spike, or the start of a structural AI-driven memory revaluation?

What Just Drove the Micron Record?

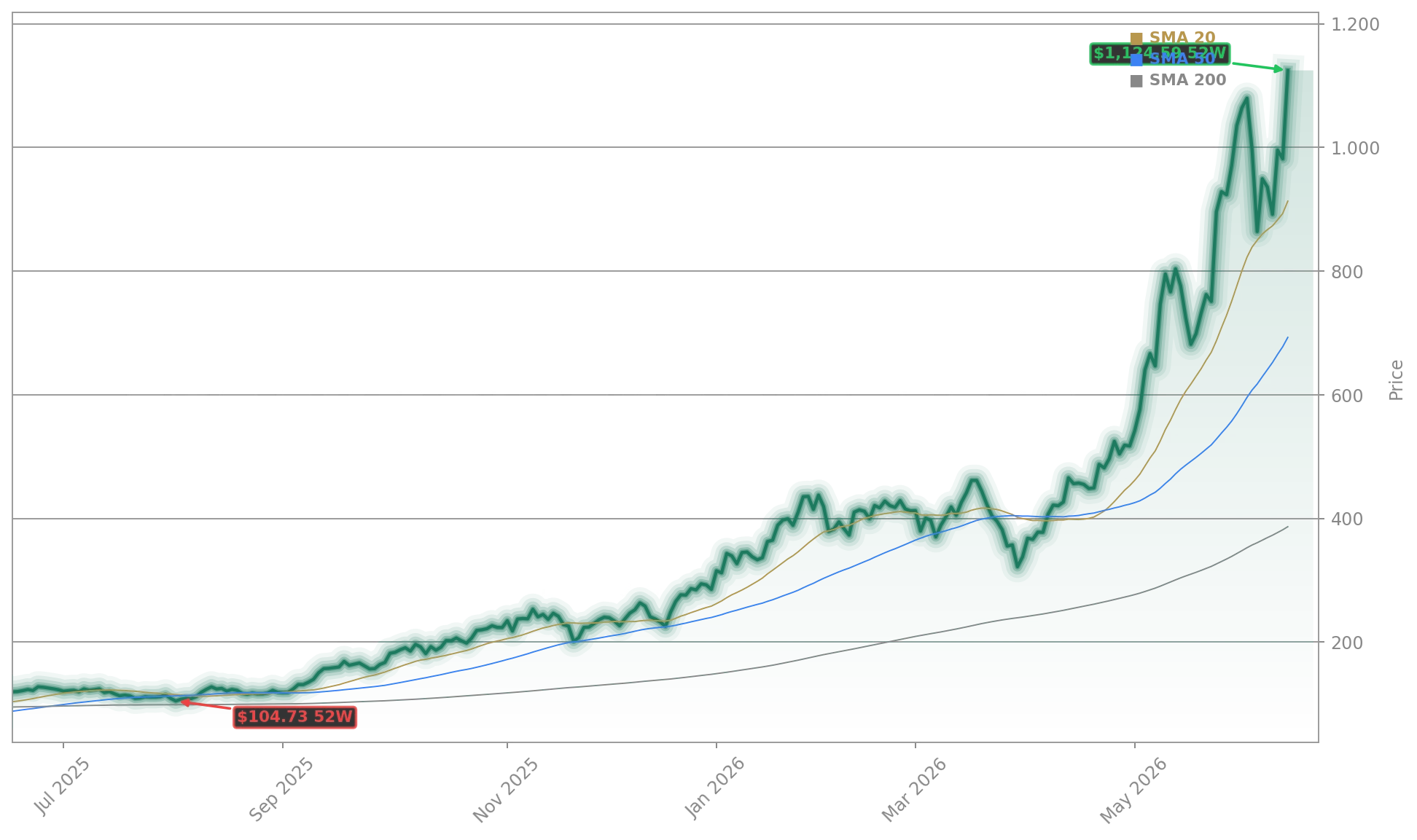

Micron Technology, Inc. surged 10.84% to $1,087.99 on Monday — its highest close ever — fueled by two major analyst upgrades and accelerating confidence in AI’s structural impact on memory economics. The memory subsector of semiconductors rose nearly 9.5%, outperforming the broader NASDAQ and S&P 500. TD Cowen lifted its price target from $660 to $1,500 — nearly tripling it — while affirming its ‘Buy’ rating. RBC Capital Markets followed with an ‘Outperform’ rating and raised its target from $525 to $1,200. Both firms cited not just short-term pricing strength, but five to six additional quarters of DRAM expansion — a radical shift in cycle visibility for a company long defined by volatility.

Why Is This Micron Record Different?

Historically, memory stocks peaked months before server pricing cycles — a telltale sign of cyclical exhaustion. This time, TD Cowen analyst Krish Sankar explicitly rejected that pattern, stating, ‘The role of the memory in AI is structural, not cyclical.’ That distinction underpins the Micron Record. High Bandwidth Memory (HBM) — the ultra-fast, capital-intensive chips essential for AI training — now accounts for over 35% of Micron’s DRAM revenue. With production requiring three times the capex of standard DRAM, HBM acts as a natural supply choke point. Meanwhile, hyperscalers like Meta and Apple have signed multiyear, volume-guaranteed contracts — including Micron’s first-ever five-year agreement — locking in pricing power well into 2027.

How Does Micron Compare to Rivals?

While NVIDIA remains the AI rally’s poster child, Micron Technology, Inc. has outperformed the chipmaker YTD — up 240% versus NVIDIA’s 182%. That outperformance reflects a narrowing valuation gap: Micron now trades at 21x forward sales, more than double its Dotcom-era peak, yet still below NVIDIA’s 28x. Competitors Samsung and SK Hynix are racing to scale HBM capacity, but Micron’s aggressive 2026 capex — up 62% YoY — and leadership in 2.5D/3D packaging give it an edge in near-term yield. Notably, Micron sold its entire 2026 HBM supply months in advance — a stark contrast to Western Digital’s softer NAND demand. Even as memory stocks rise, Micron’s margin expansion stands apart: gross margins hit 80% in Q2 — a level analysts expect to persist through FY2027.

What’s Next for the Micron Record?

With Q3 earnings due June 24, all eyes are on whether Micron Technology, Inc. delivers on CEO Sanjay Mehrotra’s promise of ‘exceptional records across revenue, gross margin, EPS, and free cash flow.’ Wall Street consensus forecasts $98.52 in non-GAAP EPS for fiscal 2027 — a 172% annual growth rate — supporting the $1,500 price target at a 15x earnings multiple, consistent with prior cycle peaks. However, Melius Research’s Ben Reitzes warns that valuation compression is inevitable as the cycle matures — though he expects $150 EPS and massive buybacks in 2027 to offset it. The RSI has cooled from 90 to 69, suggesting momentum remains intact but not yet extreme. As Barron’s notes, Micron’s rally reflects a fundamental re-rating — not just a trade.

Is the Micron Record Sustainable?

The role of the memory in AI is structural, not cyclical.— Krish Sankar, TD Cowen

Sustainability hinges on two factors: AI’s memory intensity and manufacturing discipline. While Morningstar’s William Kerwin cautions that Micron lacks a durable moat and ceded NAND/DRAM share recently, the company’s HBM leadership and contract structure provide real insulation. New fabs from Samsung and SK Hynix won’t ramp meaningfully until 2028 — giving Micron Technology, Inc. at least 18 months of pricing power. Analysts now see the memory cycle peaking in 2028, not 2026 — reinforcing the Micron Record as the start of a multi-year earnings arc, not a blow-off top. For U.S. investors, that means Micron is no longer a speculative semiconductor bet — it’s a core AI infrastructure holding.