Is Micron’s AI-fueled memory boom still intact, or did the sharp after-hours drop just expose a valuation problem?

What’s Driving the Micron Forecast Surge?

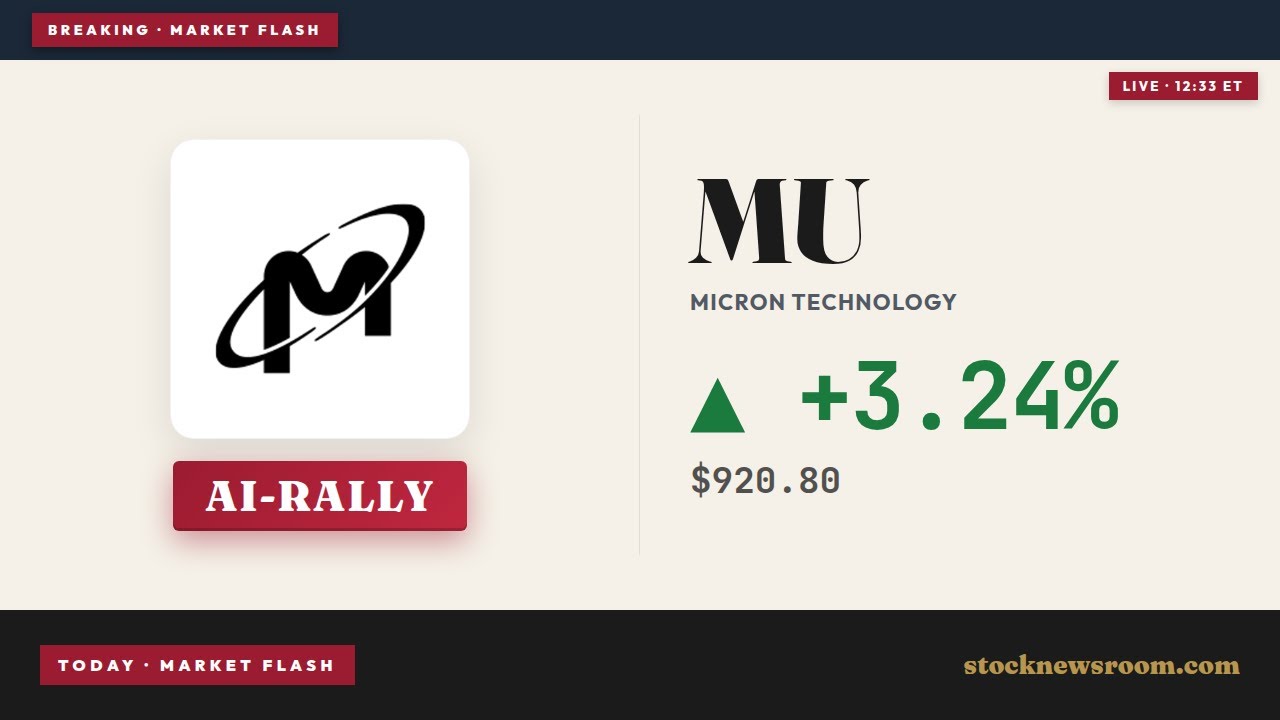

Micron Technology, Inc. surged 3.56% to $923.61 in after-hours trading on Thursday, June 11, 2026 — rebounding from a 11.5% June pullback but still sitting 14.7% below its $1,089.29 52-week high. The rally comes as analysts sharpen their Micron Forecast amid tightening supply visibility: Susquehanna analyst Mehdi Hosseini raised his target to $1,750, Cantor Fitzgerald lifted its call to $1,500, and Daiwa Securities boosted its target to $1,600 — all citing sold-out HBM4 capacity and NVIDIA’s Vera Rubin platform certification. Crucially, Micron’s fiscal Q3 guidance — $33.5 billion in revenue and $19.15 EPS — implies 60% year-over-year growth and gross margins near 81%, levels previously reserved for software firms. That structural shift is reshaping how Wall Street values the stock: at just 9x forward fiscal 2027 earnings, it trades at a steep discount to peers like NVIDIA (28x) and Apple (30x), despite delivering record free cash flow of $6.9 billion in fiscal Q2 — up 837% year over year.

How Does Micron Compare to Samsung and SK Hynix?

As one of the world’s big three DRAM makers — alongside Samsung Electronics and SK Hynix — Micron Technology, Inc. holds unique strategic weight for U.S. investors. It’s the only American-based memory champion in a sector increasingly defined by geopolitical supply-chain resilience. While Samsung and SK Hynix dominate global market share, Micron’s U.S. manufacturing footprint — now anchored by its $100 billion New York fab — gives it privileged access to CHIPS Act incentives and hyperscaler partnerships. Bechtel’s recent selection as EPC partner for the Clay, New York project underscores execution credibility. Meanwhile, Samsung and SK Hynix face export restrictions and longer lead times on U.S.-bound HBM shipments — giving Micron Technology, Inc. pricing power and near-term margin insulation. That advantage is reflected in its 74.4% GAAP gross margin — up from 36.8% a year ago — versus industry averages hovering near 62%.

Micron Forecast: Is the Cycle Really Over?

The Micron Forecast debate centers on whether AI has permanently de-commoditized memory. Morgan Stanley recently acknowledged the correction was “necessary after a massive run” but stressed “the memory cycle is not over for now.” RBC Capital Markets and Wells Fargo both reaffirmed Overweight ratings — Wells Fargo lifting its target to $1,220 — citing long-term multiyear contracts and HBM4e ramp timelines extending into 2027. Still, caution persists: Goldman Sachs maintains a Hold rating, and Morningstar warns of potential 50% revenue contraction by 2029 if new fab capacity hits supply too quickly. Yet with Micron’s HBM4 allocation fully sold out through 2026 and customers already negotiating 2027–2028 terms, the near-term Micron Forecast remains anchored in visibility, not speculation. That’s why the stock trades at a 9x forward P/E — cheap for a company growing EPS at triple-digit rates.

What Do ETFs and Technicals Say About Micron?

Micron Technology, Inc. remains the largest single weighting in the NYSE Semiconductor Index and holds 7.63% in the iShares Semiconductor ETF (SOXX). Its moves directly impact $120 billion in fund assets. Technically, shares remain in a powerful uptrend — trading 146.4% above the 200-day moving average — though MACD momentum is cooling. Resistance looms at $1,089.50, near the 52-week high. Meanwhile, the GraniteShares 2x Long MU Daily ETF (MUL) is executing a 25-for-1 stock split on June 25 — a sign of sustained retail and leveraged demand. With premarket gains of 2.98% on Thursday and Nasdaq futures up 1.27%, the broader market tailwind supports continued strength ahead of the June 24 print. That event remains the definitive catalyst — not just for Micron, but for the entire AI hardware cohort including Tesla and AMD.

What’s Next for Micron Technology, Inc.?

Micron Technology, Inc. is no longer just a memory supplier — it’s a strategic AI infrastructure partner. Its appointment of Dr. Alexis Black Björlin, former executive at NVIDIA, Meta, and Broadcom, signals deepening integration into the AI stack. With HBM demand projected to grow from $35 billion in 2025 to $100 billion by 2028, the Micron Forecast isn’t just about one quarter — it’s about capturing structural share in a $300 billion AI hardware opportunity. Investors should watch fiscal Q3 not for growth, but for margin sustainability and 2027 guidance clarity. A clean beat and strong forward outlook could trigger a wave of index rebalancing and ETF inflows — pushing the Micron Forecast toward its $1,500–$1,750 range.

In the AI era, memory has become a strategic asset for our customers, and we are investing in our global manufacturing footprint to support their growing demand.— Sanjay Mehrotra, CEO of Micron Technology, Inc.

Related Coverage: Micron’s massive New York fab breakthrough is detailed in Micron New York Fab: $16.7B Boom Ahead of Q3 Earnings, while the broader competitive dynamics in AI hardware are explored in AMD AI Strategy +3.3% as CPU Surge Lifts Wall Street View.