If Micron HBM4 just won NVIDIA certification, why did investors still send the stock sharply lower?

Why did Micron HBM4 news fail to lift shares?

Despite NVIDIA’s public confirmation that Micron Technology, Inc. is fully certified to supply high-bandwidth memory for its next-gen Vera Rubin platform — alongside Samsung and SK Hynix — MU shares declined sharply. The disconnect underscores how sentiment has shifted: while Micron HBM4 qualification secures a critical, multi-year revenue stream, broader semiconductor valuations are now being stress-tested. Broadcom’s 12.5% single-day plunge after reiterating (not raising) its 2026 AI chip guidance triggered a cascade across the sector. Arm Holdings fell over 4%, Marvell Technology slid 3.2%, and Micron Technology, Inc. joined the slide — down nearly 8% on Thursday alone. The sell-off wasn’t about Micron’s fundamentals, but about recalibration: Wall Street is pricing in slower near-term DRAM price growth and questioning whether HBM4 ramp timing aligns with potential AI capital expenditure moderation.

How does Micron HBM4 compare to rivals?

Micron Technology, Inc. is now one of only three global suppliers — alongside Samsung and SK Hynix — qualified and in production for NVIDIA’s HBM4 stack. That’s a strategic win in a market where supply constraints have pushed HBM ASPs up over 60% year-over-year. Unlike Samsung and SK Hynix — both trading on Korean exchanges and down double-digits this week — Micron Technology, Inc. is the sole U.S.-listed pure-play memory leader, giving it unique portfolio weight for domestic investors. Zacks Equity Research maintains a Strong Buy rating on Micron Technology, Inc., citing its #1 ranking and A Growth Score, driven by AI inference infrastructure demand. Meanwhile, Morgan Stanley notes that Micron’s HBM4 yield ramp is ahead of internal forecasts, though it warns that DRAM pricing may peak by Q3 2026 as new capacity comes online.

What’s the impact on the S&P 500 and NASDAQ?

Micron Technology, Inc. is a top-20 NASDAQ component and a key weight in the semiconductor sub-index — which makes up over 12% of the NASDAQ Composite. Its 7.74% drop contributed significantly to Thursday’s 1.3% NASDAQ decline and weighed on the S&P 500’s tech sector, down 0.9%. The VanEck Semiconductor ETF (SOXX) lost 1.1%, its worst day since March. This volatility matters beyond chip stocks: AI infrastructure names like Tesla and Apple saw correlated pre-market softness, with both off over 1.5% amid broad tech risk-off flows. Morningstar’s May ETF data confirms the split — traders exited semiconductor positions while long-term investors added $19.6 billion to tech ETFs, signaling divergence between momentum and fundamentals.

Are insider moves a red flag?

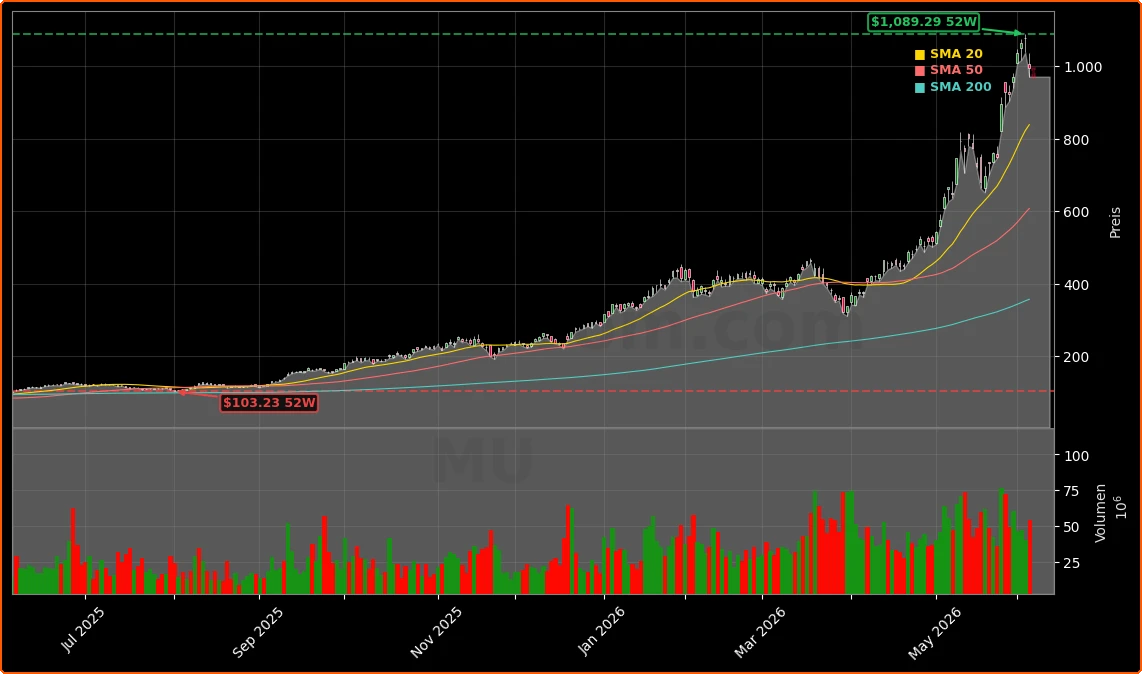

Micron Technology, Inc. CEO Sanjay Mehrotra sold $36 million in stock last week via a pre-arranged 10b5-1 plan — bringing his two-year total to over $100 million. While routine, the timing coincides with MU’s surge past $1,000 and near its 52-week high. Citigroup analysts acknowledge the selling but reaffirm their $1,125 price target, citing Micron HBM4’s role in enabling NVIDIA’s inference dominance. RBC Capital Markets maintains its ‘Outperform’ rating, emphasizing that long-term HBM4 contracts — now spanning three to five years — drastically reduce the cyclicality risk that once defined Micron Technology, Inc.’s business model. Still, the insider activity adds fuel to concerns about near-term valuation stretch, especially as forward P/E approaches 38x — above the semiconductor sector median.

What’s next for Micron HBM4 adoption?

Production for Micron HBM4 is now underway, with initial shipments to NVIDIA expected in late Q3 2026. Analysts at 24/7 Wall St. project Micron Technology, Inc. will capture 22% of total HBM4 supply in 2027 — up from 15% in HBM3 — driven by its 1.2 TB/s stack architecture and advanced packaging partnerships. Crucially, HBM4 adoption isn’t limited to NVIDIA: Apple’s next-gen AI silicon and Meta’s upcoming inference accelerators are also evaluating Micron HBM4. The company’s $9 billion capital expenditure plan for 2026 — up 24% year-over-year — signals full confidence in the HBM4 supercycle. With memory accounting for over 65% of AI accelerator BOM cost, Micron HBM4 isn’t just a product — it’s infrastructure.

Related Coverage: Analysts are questioning whether record memory revenue hides an inflection point — Micron Memory Prices: Is $33.5B Revenue Hiding a Peak?. Meanwhile, Zacks Equity Research highlights Micron Technology, Inc. as a top AI infrastructure play in its latest Strong Buy roundup, and Benzinga reports on CEO insider activity in this detailed analysis.

Micron is one of the three big DRAM makers, along with Korean companies SK Hynix and Samsung. GPUs and custom AI ASICs need to be packaged with large amounts of HBM for optimal performance, and the shift toward inference is only driving demand higher.— Zacks Equity Research

Micron HBM4 is a cornerstone of AI’s inference era — and a critical competitive advantage for Micron Technology, Inc. For U.S. investors, the recent pullback presents a tactical entry point amid structural demand tailwinds. The next catalyst will be Micron’s Q3 earnings report — expected in mid-July — where HBM4 revenue contribution and DRAM pricing guidance will define the next leg of the rally.