Are Micron Memory Prices nearing a peak just as AI demand makes Micron look stronger than ever?

Are Micron Memory Prices Already Peaking?

Raymond James analyst Karl Ackerman has issued a stark forecast: DRAM and NAND average selling prices will peak in mid-calendar year 2026 — significantly earlier than the mid-2027 timeline previously assumed by most Wall Street firms. Ackerman’s call, supported by accelerating fab expansions at SK Hynix and Samsung Electronics, has triggered renewed scrutiny of Micron Technology, Inc.’s pricing power. While Micron’s operating margin soared to 68% last quarter on $24 billion in revenue, that margin assumes continued price discipline and supply constraints. If Micron Memory Prices soften even modestly, earnings could decelerate faster than forward guidance implies — especially as the company prepares for $33.5 billion in next-quarter revenue, a figure that exceeds its entire 2024 annual total.

How Does Micron Compare to Marvell and NVIDIA?

While NVIDIA dominates AI chip headlines and Marvell Technology (MRVL) garners bullish attention for its AI networking chips, Micron Technology, Inc. occupies a uniquely critical — and less substitutable — position in the AI stack: high-bandwidth memory (HBM). Unlike logic chips, memory cannot be easily virtualized or optimized away. That structural advantage has allowed Micron to command long-term contracts with Meta, Microsoft, and cloud hyperscalers — a moat Marvell lacks. Yet Marvell trades at a higher valuation premium despite lower GAAP profitability and a higher debt-to-equity ratio, according to Yahoo Finance Singapore. Meanwhile, NVIDIA’s ecosystem expansion continues to lift demand for Micron’s HBM3 and HBM4, reinforcing pricing leverage — but also increasing dependency on a single catalyst.

What Do Analysts Say About MU’s Valuation?

Morgan Stanley recently lifted Micron’s price target and reaffirmed its Outperform rating, citing 2–3 years of tight memory supply and strong HBM contract renegotiation tailwinds. The firm expects Micron to benefit from continued AI infrastructure build-out, even amid rising supply. In contrast, Raymond James maintains its Outperform rating but explicitly warns that Micron’s forward P/E — now at 11.7x, up from 4.4x in April — reflects growing market awareness of near-term margin pressure. Citigroup has not adjusted its rating but notes that Micron’s current multiple assumes ‘moderating contract ASP growth’ and ‘oversupply conditions looming in the next 1–2 years.’ These divergent views underscore a broader Wall Street tension: is Micron a structural beneficiary of AI, or merely the latest cyclical winner in a historically volatile sector?

Could SpaceX IPO Drain Liquidity From MU?

With SpaceX’s highly anticipated IPO expected later this year — and its acquisition of xAI adding AI credibility — some investors worry about a liquidity drain from semiconductor stocks like Micron Technology, Inc. While SpaceX is not a memory competitor, its projected $100+ billion valuation could absorb capital from high-flying tech names. Barron’s reports that pre-market selloffs in MU, Marvell, and Arm on June 4 reflect this rotation risk. Yet analysts stress a key distinction: SpaceX delivers AI services; Micron delivers AI hardware. That hardware dependency remains non-negotiable — and increasingly expensive. As Morgan Stanley notes in its ‘chipflation’ report, memory chip prices have spiked six-fold, forcing Sony and Lenovo to raise consumer device prices — evidence that Micron Memory Prices are not just a Wall Street story, but a macroeconomic input.

What’s Next for Micron’s Earnings Trajectory?

We expect DRAM and NAND average selling prices will peak in mid-CY26.— Karl Ackerman, Raymond James

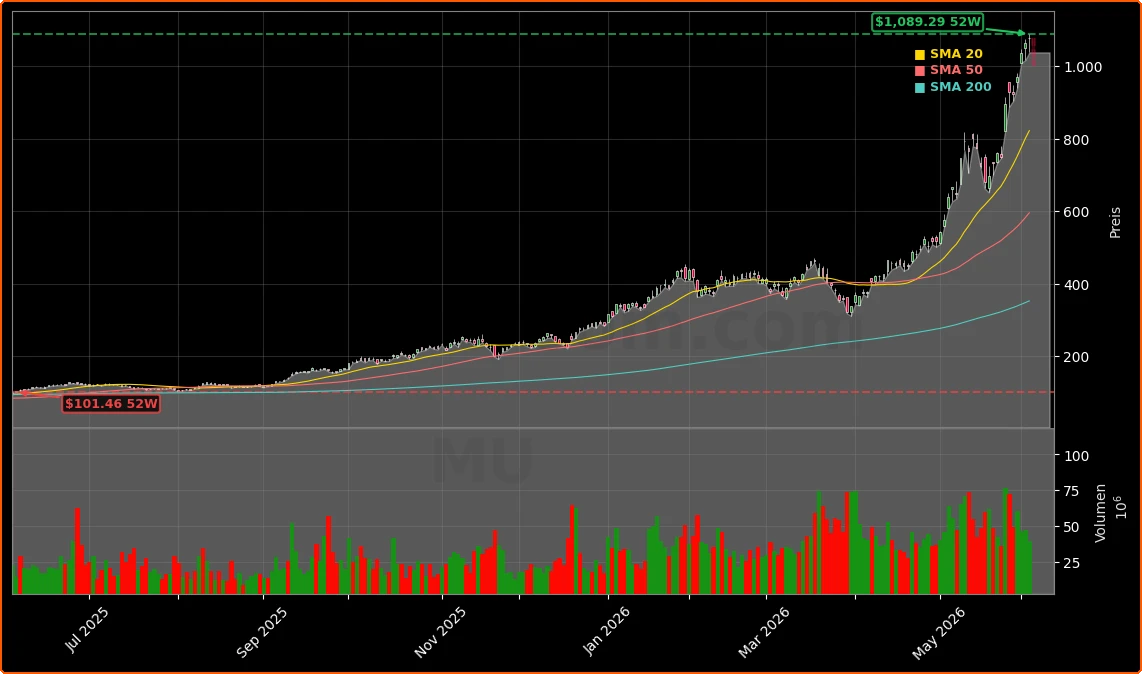

Micron Technology, Inc. is projected to generate over $100 billion in net income in both 2027 and 2028 — a figure that would imply a forward P/E of just 12 on its $1.2 trillion market cap. But that forecast assumes AI infrastructure spending remains unbroken. Any slowdown in cloud capex, geopolitical supply chain disruption (e.g., US-Iran tensions), or unexpected yield improvements at Korean rivals could compress Micron Memory Prices faster than anticipated. With options activity showing bearish positioning and the stock trading well above its 52-week moving average, volatility is likely to rise ahead of Q2 2026 earnings — due in early August. For now, Micron’s dominance in HBM remains unchallenged — but pricing power is not infinite.