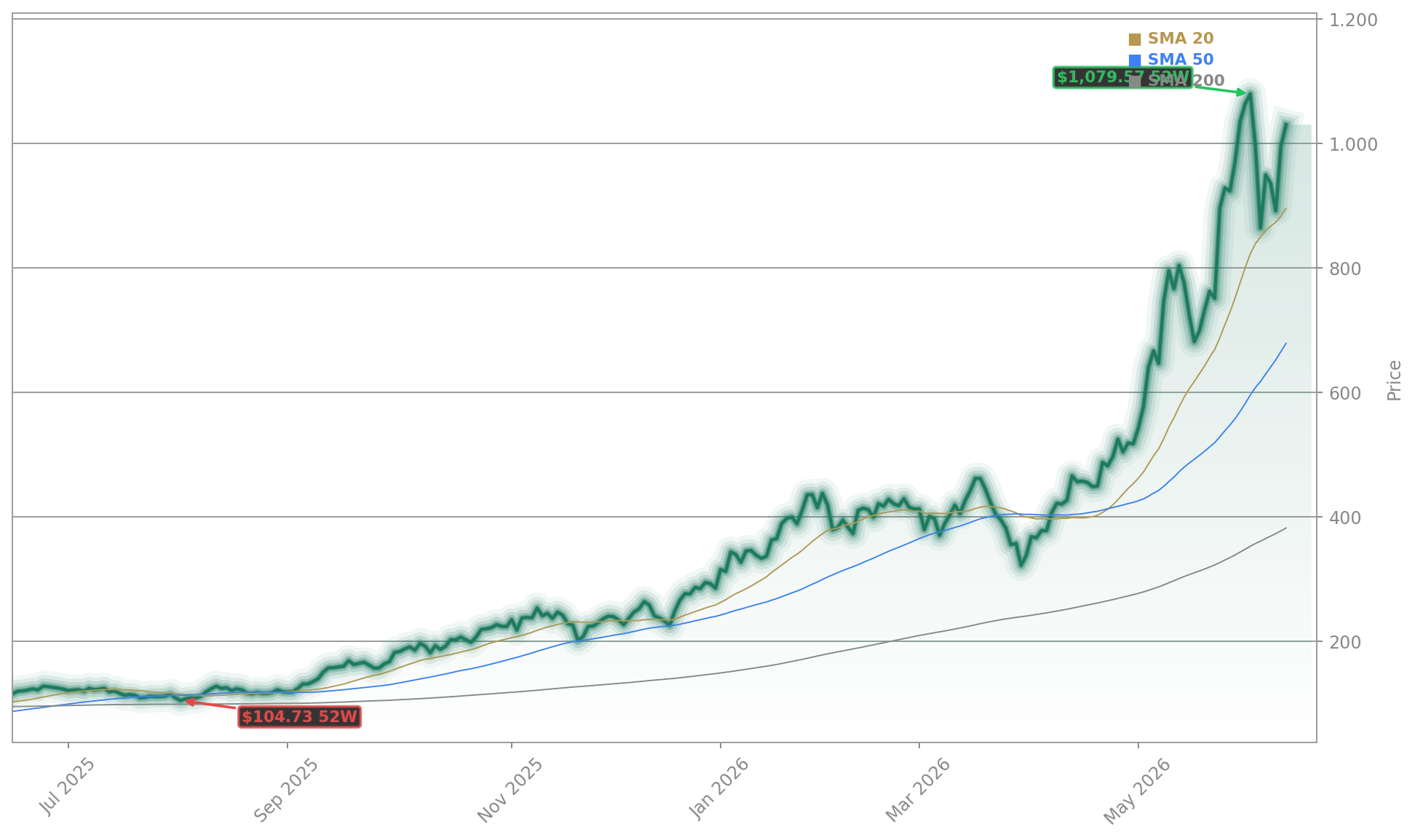

Can Micron’s AI memory surge keep pushing the stock toward $1,000, or is Wall Street already pricing in perfection?

Why is Micron Record momentum building?

Micron Technology, Inc. has become one of the market’s most aggressive AI winners, with investors treating memory as a direct beneficiary of the next data-center buildout. The latest advance pushed MU closer to the $1,000 level intraday, extending a sharp run that recently carried the company above a $1 trillion market capitalization. That milestone places Micron in rare semiconductor territory alongside NVIDIA and Broadcom, and it underscores how quickly investor attention has shifted from pure GPU exposure to the memory layer that supports AI training and inference.

The bull case is centered on high-bandwidth memory, where Micron has been gaining strategic relevance. Its HBM3E products already ship with strong performance and energy-efficiency claims, and its HBM4 roadmap is now tied to next-generation AI systems. Demand has been strong enough that Micron’s 2026 HBM supply is effectively sold out, reinforcing a market narrative built on scarcity, pricing power, and unusually strong earnings leverage.

What are analysts saying about Micron?

Fresh Wall Street target hikes added fuel to the rally. Mizuho reiterated an Outperform rating and raised its price target on Micron to $1,150 from $800, arguing that agentic AI should drive a meaningful increase in memory intensity across servers and enterprise systems. Mizuho also turned more constructive on related names including SanDisk, Dell Technologies, Arm Holdings, and On Semiconductor, signaling that the firm sees the next AI leg broadening beyond accelerators into infrastructure and storage.

Susquehanna analyst Mehdi Hosseini also became more bullish, raising his target as he projected memory pricing would stay stronger for longer than many investors expected. That matters because Micron’s earnings power is highly sensitive to pricing in DRAM, NAND, and premium AI memory products. The current Micron Record setup is therefore not just about volume growth; it is also about mix, supply tightness, and the possibility that margins remain elevated deeper into 2026 and 2027.

Can Micron sustain a trillion-dollar value?

The core debate on Wall Street is whether Micron can hold this valuation once the memory cycle eventually normalizes. Bulls point to explosive growth: fiscal second-quarter revenue rose to $23.8 billion, while management has guided for a record $33.5 billion in fiscal third-quarter revenue. Cloud memory and mobile-client demand have both surged, helped by AI servers, AI PCs, and increasingly memory-hungry smartphones. The company’s strategic ties to NVIDIA, Samsung, and SK Hynix also keep Micron close to the center of the AI hardware stack.

Still, memory remains cyclical. As more capacity comes online, today’s shortage could ease, weakening the pricing power that currently supports extraordinary profit expansion. Yahoo Finance highlighted that tension by noting the market’s enthusiasm has pushed Micron far above some fair-value estimates. TipRanks, meanwhile, flagged both the strong earnings backdrop and the risk that technical conditions are becoming overbought after a massive year-to-date run. For US investors, that makes MU one of the most compelling but also one of the most hotly debated names in the semiconductor complex, alongside Apple supply-chain beneficiaries and broader AI infrastructure plays.

Related Coverage: Investors looking for a deeper dive into the memory thesis can also read Micron AI Memory in Record HBM Boom as Targets Climb. That piece examines whether soaring HBM demand and rising analyst targets still leave room for upside, while also addressing the risk that expectations may already be racing ahead of fundamentals.

Micron Record trading now hinges on whether AI memory demand can keep outrunning concerns about peak-cycle valuation. If HBM tightness, DRAM pricing, and enterprise AI deployments stay firm, MU could keep pressing toward $1,000, making the next earnings update and additional analyst revisions the key catalysts investors will watch.