Can Micron’s AI memory advantage really turn a notoriously cyclical chipmaker into a premium growth story?

Why is the Micron Forecast changing?

Micron Technology, Inc. (MU) was up 13.18% intraday at $849.84, versus a previous close of $745.56, as analysts pushed their outlooks higher following fresh signs that AI memory demand remains tight. UBS lifted its target price to $1,625 from $535, one of the most dramatic target revisions on Wall Street this year. Mizuho kept its Outperform rating and an $800 target, while also maintaining Micron as a top pick tied to durable AI infrastructure demand.

The core of the new Micron Forecast is simple: memory pricing may be becoming less volatile because more supply is now being locked into multiyear agreements. UBS argued that long-term contracts, often spanning three to five years, can trade some near-term upside for better demand visibility, steadier utilization, and a smoother earnings profile. That matters because Micron has historically been valued as a boom-bust memory stock rather than a structurally advantaged AI supplier.

Can Micron hold AI memory leadership?

Micron’s bull case rests on its position in high-bandwidth memory, or HBM, a critical component for AI accelerators and servers. Alongside major Asian rivals, Micron is one of only a few global suppliers capable of producing advanced HBM at scale. Management has already indicated that 2026 HBM capacity is sold out under fixed-price contracts, and market commentary increasingly points to visibility stretching into 2027.

That puts Micron near the center of the same AI spending wave powering NVIDIA, Advanced Micro Devices, and hyperscale cloud platforms. UBS said 60% to 70% of industry server DDR5 supply may already be tied up through enhanced long-term contracts with large customers. If that trend continues, Micron’s revenue mix could become more resilient than in prior memory cycles. Mizuho has also pointed to sustained DRAM and NAND demand as AI servers expand and enterprises deploy more memory-intensive workloads.

What are analysts now modeling?

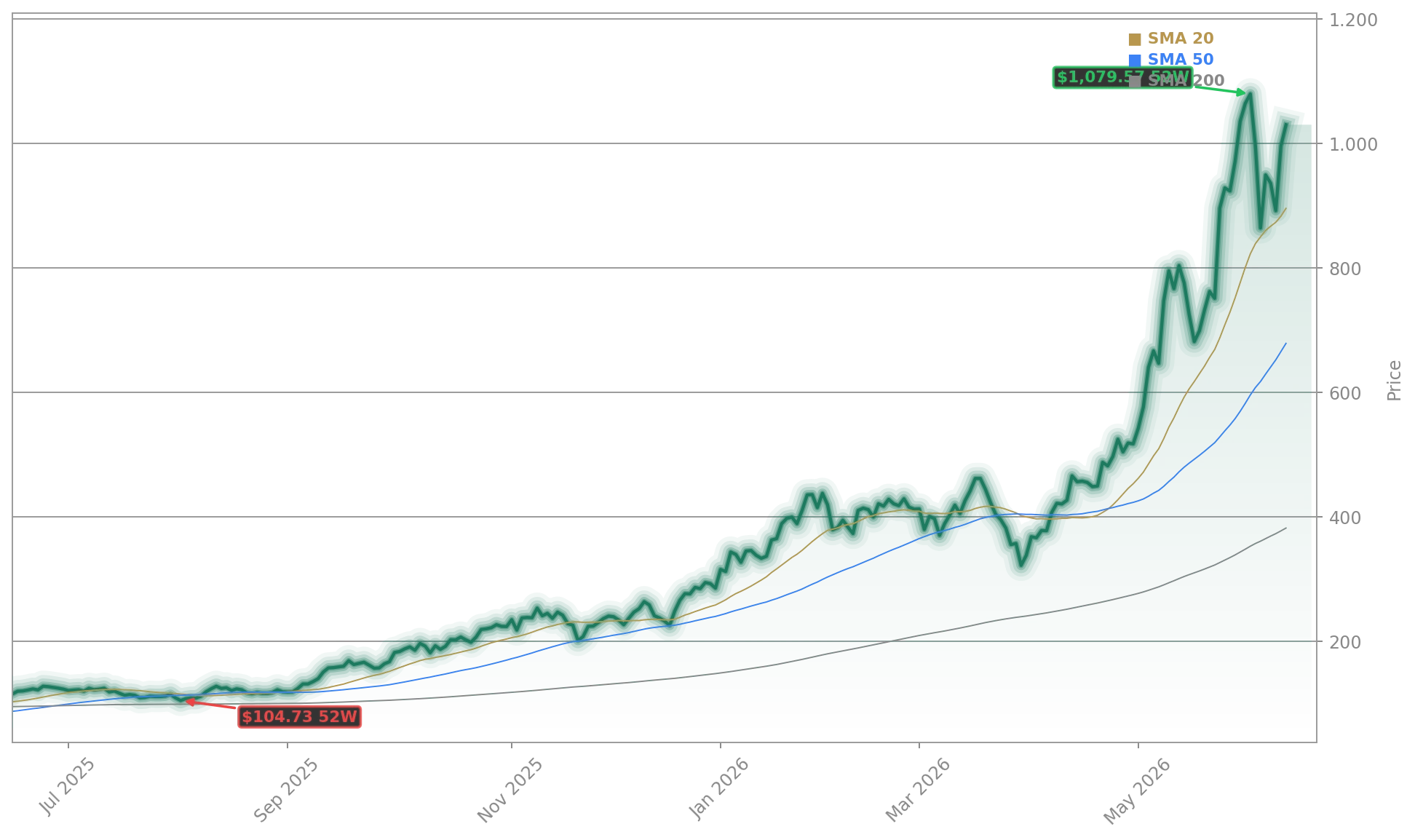

UBS materially raised its earnings estimates through 2029 and argued Micron could support earnings above $100 per share even if the market softens moderately later in the cycle. The bank’s valuation framework applies roughly 15 times next-12-month earnings, a multiple it believes is more comparable to premium AI hardware leaders than old-line commodity memory names. That is an aggressive stance, but it shows how fast the Micron Forecast is being rewritten.

Recent operating performance helps explain the enthusiasm. Micron reported quarterly revenue of about $13.64 billion, up 56.6% year over year, with non-GAAP EPS of $4.78 above expectations. Gross margin also expanded sharply, while cloud memory posted standout profitability. Guidance for the current quarter called for revenue near $18.7 billion and non-GAAP EPS of $8.42, reinforcing the idea that the company remains one of the clearest publicly traded ways to play AI memory.

How much risk still remains for Micron?

Despite the rally, investors should not ignore the cyclical risks. Memory has a long history of oversupply, abrupt price reversals, and sharp valuation resets when capacity catches up. That is why some market observers remain constructive but cautious, arguing Micron’s near-term fundamentals are exceptional even if the longer-term cycle will eventually reassert itself.

There is also a valuation question. At an $849.84 stock price, Micron is already trading above Mizuho’s $800 target, even after Tuesday’s surge. Bulls argue the stock still has room if AI demand stays undersupplied and contract pricing remains firm. Skeptics counter that the shares now require continued execution, sustained tightness, and no major pause in data-center spending from customers such as Apple suppliers, cloud players, and AI system builders linked to NVIDIA.

Related Coverage: StockNewsRoom recently examined the company’s earlier setup in Micron Forecast +4.1% as AI Memory Boom Lifts MU Outlook. That piece focused on strengthening DRAM and NAND pricing and asked whether the AI memory cycle still had room to run. Tuesday’s analyst moves add fresh support to that thesis, while also raising the stakes for Micron’s next earnings report.

We believe there’s no clear line of sight on when the supply-demand imbalance could end as demand durability sees secular long-term tailwinds with DRAM/NAND as key AI enablers.— Vijay Rakesh, Mizuho

The latest Micron Forecast reflects a market that is no longer treating memory as just another commodity segment. If long-term contracts, HBM scarcity, and AI server demand continue to tighten supply, Micron could keep earning a premium multiple. For investors, the next key test is whether upcoming results confirm that this AI-driven reset in memory economics is durable.