Are Micron Earnings proving the AI memory boom is real, or is Wall Street chasing the next semiconductor peak?

What Do Micron Earnings Mean for the S&P 500?

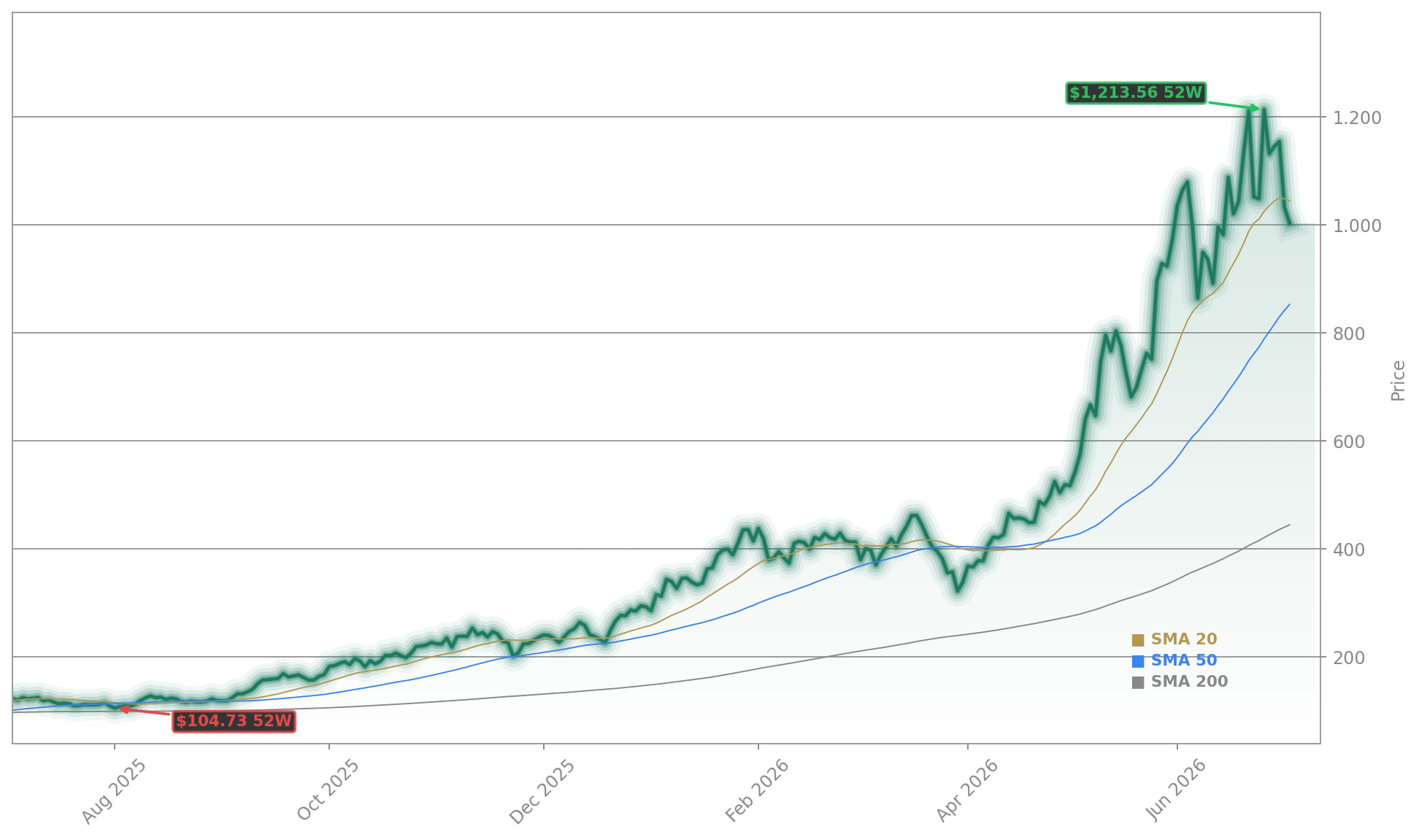

Micron Technology, Inc. isn’t just outperforming — it’s dragging the broader index upward. Year-to-date, Micron has surged 304%, making it the third-highest contributor to S&P 500 gains in H1 2026 — behind only Sandisk and Intel. Its 22.1x forward P/E sits below the S&P 500’s 21.5x average, while its 32.6% ROE and $35.58 billion in EBITDA dwarf industry peers. Unlike cyclical laggards, Micron’s $50.72 billion revenue forecast for FY2026 — up from $11.31 billion a year earlier — signals structural demand, not transitory hype. That’s why the Invesco PHLX Semiconductor ETF (SOXQ) and S&P 500 Momentum ETF (SPMO) have sharply increased MU weightings this quarter.

How Does Micron Compare to NVIDIA and Samsung?

While NVIDIA dominates AI compute, Micron Technology, Inc. owns the memory bottleneck — and that’s where margins are exploding. With gross margins hitting 85%, Micron outpaces NVIDIA’s 77% and Samsung’s estimated 62% in memory. UBS analyst Nicolas Gaudois projects DDR memory prices will rise 32% in Q3 and another 18% in Q4 — a catalyst NVIDIA can’t replicate. Meanwhile, Samsung’s 20% price hike announcement reinforces tightness across the ‘big three’ (Micron, SK Hynix, Samsung), but only Micron is U.S.-listed and deeply embedded in U.S. data center supply chains. That gives Micron Technology, Inc. a distinct edge in capital allocation, regulatory access, and shareholder returns — especially as it deploys $9.3 billion in Hiroshima to scale HBM production with $3 billion in Japanese government backing.

Why Are Analysts Raising Targets Despite Michael Burry’s Short?

Michael Burry’s recent short position — citing ‘defined cyclical like no other’ — has sparked volatility, but Wall Street is doubling down. Cantor Fitzgerald raised its price target to $2,000 on June 29, maintaining an Overweight rating. Barclays followed with its own $2,000 Overweight target. UBS’s Gaudois sees $1.2 trillion in industry free cash flow by 2027E and forecasts undersupply until at least Q2 2028. The disconnect? Burry focuses on long-term memory cycles; analysts see AI-driven demand compressing the bust phase. With 20–30% of Micron’s shipments now locked in 3–5 year contracts — many with prepayment — revenue visibility extends well beyond 2027. That’s why Jim Cramer now calls Micron Technology, Inc. ‘a secular growth story, not a cyclical story.’

What’s Next After Micron Earnings?

Fundamentals remain strong, with the memory industry set to generate close to $1.2 trillion of FCF in 2027E. We believe this will ultimately lead to a step-up in returns to shareholders.— Nicolas Gaudois, UBS analyst

Investors now pivot to September 22, when Micron Technology, Inc. reports Q3 results — but the real catalyst is already priced in. The $9 billion Hiroshima expansion is breaking ground, Teradyne (TER) order visibility is surging on test equipment demand, and U.S. auto OEMs like General Motors are signing new memory supply agreements. Meanwhile, SK Hynix’s U.S. listing could drain liquidity — or, as Benzinga notes, spur competitive investment that further tightens supply. For U.S. portfolios, Micron Earnings aren’t just a quarterly beat — they’re validation that AI infrastructure spending has legs. With 345.7% revenue growth and a debt-to-equity ratio of just 0.06, Micron Technology, Inc. is arguably the cleanest leveraged play on AI memory in the entire NASDAQ.