Has Micron finally broken out of its old boom-bust pattern, or is this AI-fueled rally just another cycle in disguise?

Is Micron Technology, Inc. Still Cyclical?

Historically, memory chipmakers like Micron Technology, Inc. have been defined by violent boom-bust cycles — a reality underscored by Michael Burry’s recent short position, which he described as targeting a ‘defined cyclical like no other.’ Yet Q2 2026 data tells a different story: 85% gross margins, $35.58 billion in EBITDA, and a debt-to-equity ratio of just 0.06 signal unprecedented financial discipline and pricing power. Crucially, 20–30% of Micron’s shipment volume is now locked in under 3–5 year contracts — many with prepayment — directly mitigating traditional cyclicality. As Jim Cramer noted on Yahoo Finance Singapore, ‘Micron’s become a secular growth story, not a cyclical story.’ That reframing is now central to the Micron Forecast.

How Does Micron Compare to NVIDIA and Intel?

While NVIDIA dominates headlines as the AI infrastructure leader, Micron Technology, Inc. is emerging as its indispensable memory counterpart. Unlike Intel — trading at 90x forward P/E and lagging with just 278% YTD gains — Micron trades at 22.1x forward earnings, well below the S&P 500’s 21.5x average and far more reasonable than peers like Broadcom (59.98x) or AMD (172.61x). Its 32.62% ROE outpaces the industry average by 24.7%, and its revenue growth (345.72%) dwarfs NVIDIA’s 85.23%. Analysts at UBS and Cantor Fitzgerald aren’t just raising targets — they’re reclassifying the stock. UBS’s Nicolas Gaudois maintains a $1,625 price target, citing $1.2 trillion in projected industry free cash flow by 2027. Cantor Fitzgerald lifted its forecast to $2,000 on June 29, citing ‘structural DRAM tightness.’ This competitive edge positions Micron Technology, Inc. as a critical, undervalued lever for AI exposure — especially as Samsung moves to raise memory prices by 20%.

Micron Forecast: What Drives the 2027–2028 Outlook?

The Micron Forecast for 2027–2028 hinges on three pillars: supply constraints, AI memory architecture, and geographic expansion. UBS projects DDR memory prices will rise 32% in Q3 2026 and another 18% in Q4 — with the DRAM industry remaining undersupplied until at least Q2 2028. Micron’s $9.3 billion Hiroshima expansion — backed by $3 billion in Japanese government funding — will ramp HBM production later this decade, directly servicing the AI data center build-out expected to accelerate through 2030. Meanwhile, its $100 billion in strategic agreements insulates near-term earnings from volatility. As Melius Research’s Ben Reitzes emphasized in raising his target to $2,200, ‘Micron is the sole major U.S.-based manufacturer of HBM, NAND, and DRAM for AI-accelerated data centers.’ That U.S. anchor status adds strategic weight in an era of supply chain reshoring.

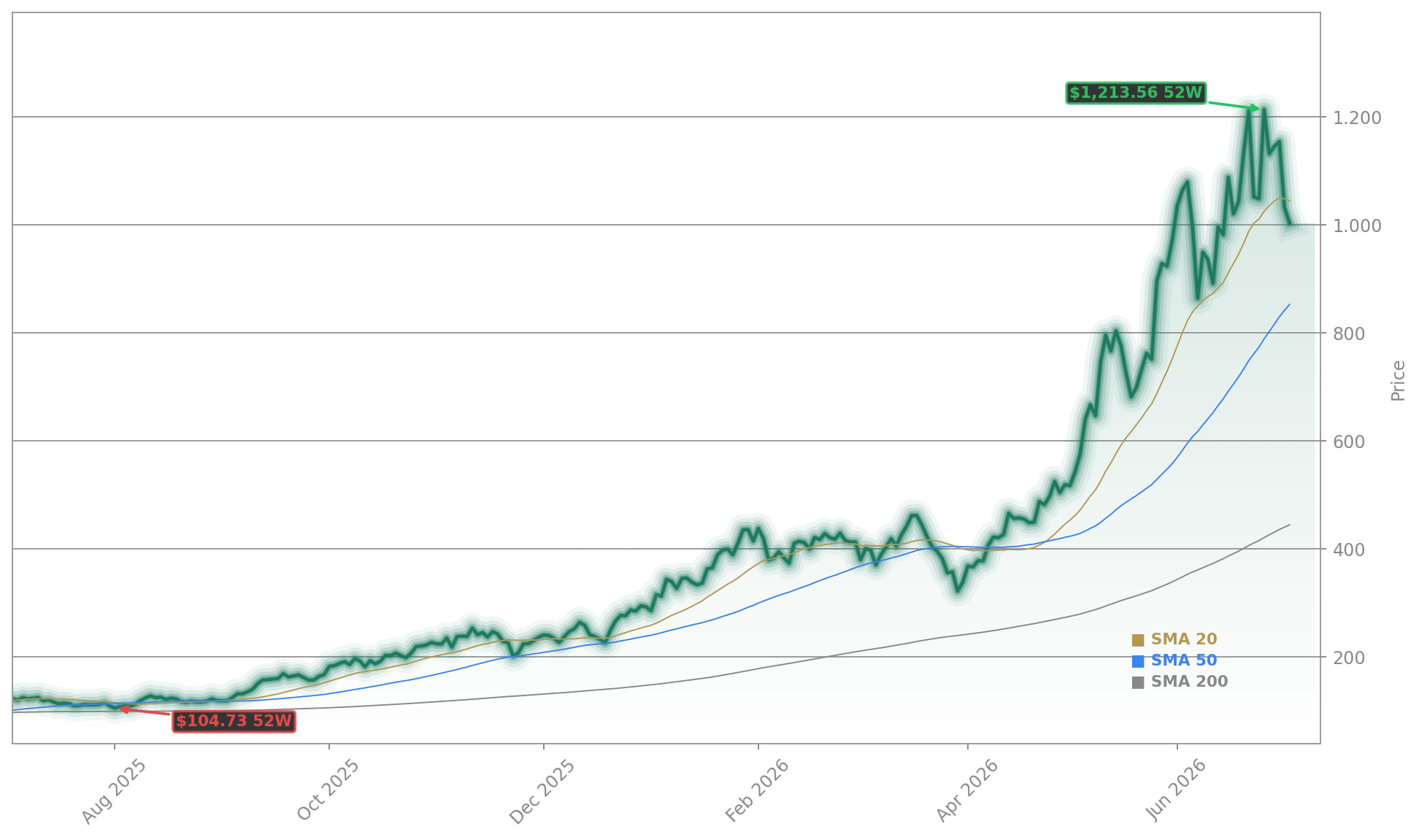

Why Did the Stock Dip — and Is It a Buy?

Despite its strength, Micron Technology, Inc. shares fell 14% over five sessions in early July — a correction that Barron’s called a ‘chance to get in on the memory surge.’ The selloff had no fundamental catalyst, occurring amid broader tech volatility and concerns over AI trade visibility. Yet premarket trading on Monday, July 6, saw the stock rise nearly 3% to $1,007.54 — now 127.1% above its 200-day moving average. Technical indicators remain bullish: the RSI is neutral at 48.67, and key support holds near $991.00. With a consensus Buy rating and average price target of $1,542.05 — implying 53% upside — the dip reflects sentiment, not fundamentals. Citigroup has even opened a ’90-day upside catalyst watch’ with a $1,400 target, citing stronger AI CPU demand driving DRAM pricing.

What’s Next for Micron Technology, Inc.?

With earnings due September 22, 2026, the next catalyst is clarity on HBM3 ramp timing and long-term contract execution. Regulatory scrutiny remains a risk — a class-action lawsuit alleging price-fixing with SK Hynix and Samsung is ongoing — but Micron’s U.S. domicile and strong balance sheet provide resilience. The Higashihiroshima expansion, covered by Seeking Alpha, and growing automotive memory partnerships — highlighted in AUTO Connected Car News — signal diversification beyond data centers. As Wall Street redefines the memory cycle, the Micron Forecast is no longer about cyclical timing — it’s about AI’s decade-long infrastructure build-out. Investors are pricing in 200%+ earnings growth for fiscal 2026, and the runway extends well beyond.

Related coverage: Micron Earnings +3.3%: Record AI Memory Boom Lifts Targets details how Q2 results validated the structural shift in memory demand. For deeper technical context on the HBM supply chain, see Micron launches $9B plant expansion in Japan. Investors also monitor how Micron’s results lift Teradyne orders and Susquehanna’s rating, highlighting the broader semiconductor equipment ecosystem.

Micron Technology, Inc. has permanently upgraded its earnings profile through AI-driven demand, strategic contracts, and capital discipline. For U.S. portfolios, it represents a rare blend of growth, profitability, and geopolitical advantage. The next quarterly earnings will confirm whether the Micron Forecast holds — and whether the stock can sustain its leadership in the AI memory race.

Micron’s become a secular growth story, not a cyclical story.— Jim Cramer

Fazit folgt.