Is the Micron Forecast still too conservative if AI memory demand stays tight all the way into 2028?

Is Micron Forecast Too Optimistic?

Not according to UBS analyst Nicolas Gaudois, who maintains a $1,625 price target and calls the recent selloff ‘likely temporary.’ His forecast rests on structural supply constraints: UBS estimates bit demand growth for DRAM will hit +36.2% year-over-year in 2027, while supply expands only +19.3%. That gap ensures tightness through mid-2028. Cantor Fitzgerald has gone further—raising its price target to $2,000 on June 29 and reiterating an Overweight rating. Barclays echoed that move, also lifting its target to $2,000. Even Melius Research’s Ben Reitzes, who initiated coverage at $700 in April, now sees $2,200—implying a $2.5 trillion valuation, larger than NVIDIA, Tesla, and Broadcom combined.

How Does Micron Compare to Peers?

Micron Technology, Inc. trades at a P/E of 22.05—well below the semiconductor industry average of 147.9 and even the S&P 500’s 21.5x forward multiple. Its ROE of 32.62% dwarfs the sector average of 7.92%, and its $35.58 billion in EBITDA is nearly six times the industry norm. Unlike Apple or Broadcom, Micron’s revenue growth of 345.72% isn’t just cyclical—it’s AI-infrastructure driven. While NVIDIA (NVDA) powers AI computation, Micron powers AI memory access. That symbiosis matters: data centers can’t scale without both. And with Samsung signaling a 20% memory price hike and SK Hynix preparing its U.S. listing, pricing power remains concentrated—and U.S.-anchored in Micron’s case.

What’s Driving the Micron Forecast?

The Micron Forecast hinges on three pillars: long-term agreements, HBM capacity expansion, and AI infrastructure build-out timelines. Micron has locked in 20–30% of its shipment volume under 3–5 year contracts—with prepayment—reducing cyclicality. Its $9.3 billion Hiroshima HBM fab, backed by $3 billion in Japanese government support, begins production later this decade. Meanwhile, PwC estimates the AI-enabling infrastructure opportunity at $15.7 trillion globally. That’s not a 2026 story—it’s a 2026–2030 runway. Jim Cramer recently declared Micron ‘a secular growth story, not a cyclical story,’ a reversal from his past skepticism about memory makers’ boom-bust patterns.

Are Legal and Short-Seller Risks Overblown?

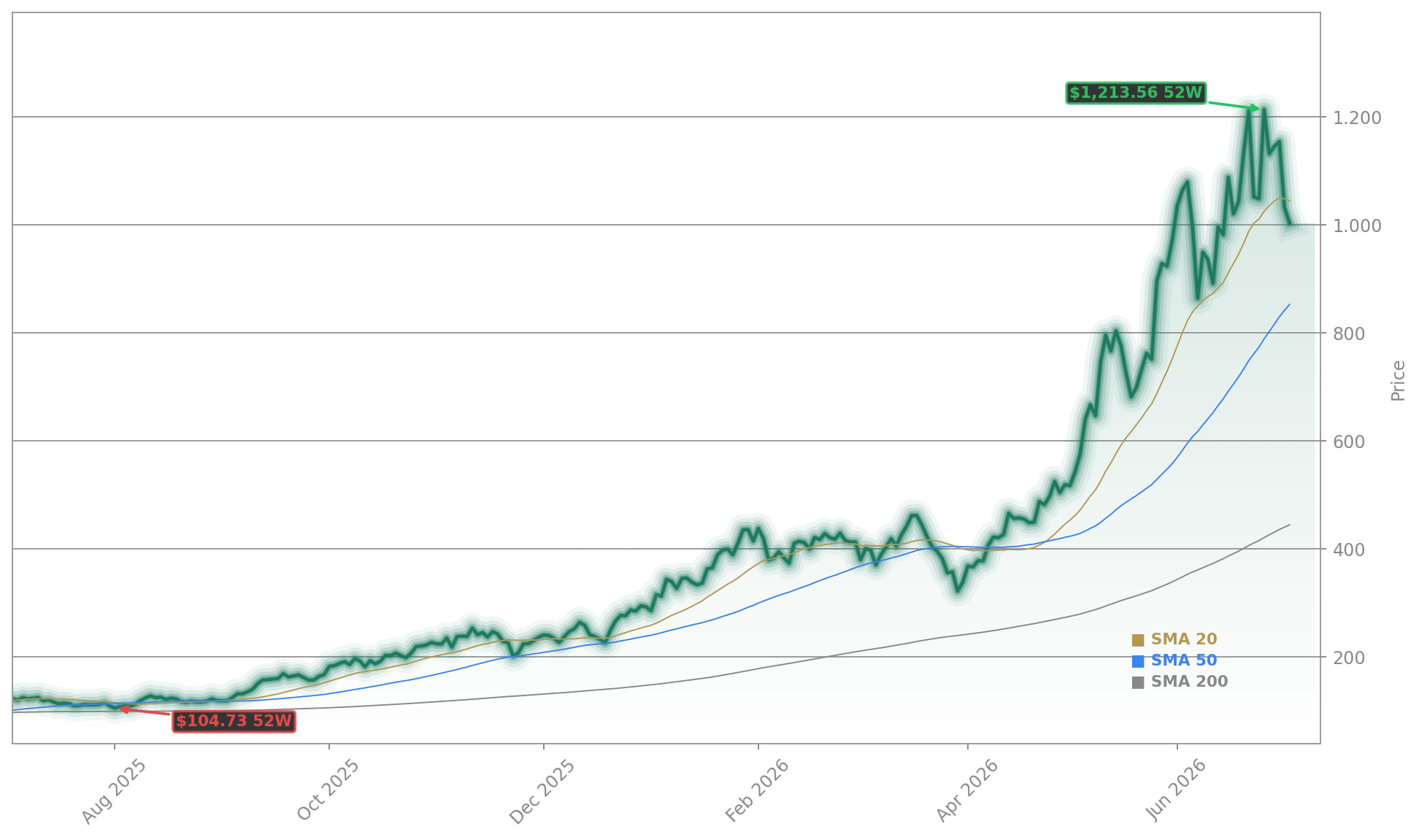

Michael Burry’s short position—and a class-action lawsuit alleging price coordination among Micron, SK Hynix, and Samsung—have added volatility. But the market is pricing in resilience: MU’s stock rose 3.17% on Monday, July 6, to $1,009.54, despite those headwinds. Analysts note that Burry’s thesis assumes a return to 2025-style oversupply—a scenario UBS explicitly rules out before 2028. Technical indicators support the bullish case: MU trades 127.1% above its 200-day moving average and remains in a long-term uptrend. Its Benzinga Edge Growth score of 84.78 and Momentum score of 99.62 reflect institutional conviction, not speculation.

What’s Next for Micron Forecast and Wall Street?

The next catalyst arrives September 22, 2026, when Micron reports Q3 earnings—its ninth consecutive beat. Wall Street expects EPS of $31.24 on $50.72 billion in revenue, up from $3.03 and $11.31 billion a year earlier. Citigroup has opened a 90-day upside catalyst watch with a $1,400 price target, citing strengthening AI CPU demand. With memory supply unlikely to catch demand before 2028—and with Micron’s gross margins hitting 85%—the Micron Forecast is no longer about timing the cycle. It’s about owning infrastructure for the AI era. As one analyst put it: ‘This isn’t a rally. It’s a re-rating.’

Fundamentals remain strong, with the memory industry set to generate close to $1.2 trillion of FCF in 2027E. We believe this will ultimately lead to a step-up in returns to shareholders.— Nicolas Gaudois, UBS analyst

Related coverage: Micron Forecast +3%: AI Memory Boom Extends Through 2028 analyzes how long-term contracts and HBM capacity expansion lock in pricing power beyond 2027. For deeper technical context on how Micron’s momentum compares to broader semiconductor ETFs, see Micron Forecast +3%: AI Memory Boom Extends Through 2028.