How did Micron Earnings smash expectations while the stock still suffered one of its ugliest weekly sell-offs in months?

What triggered Micron’s 14.4% weekly collapse?

This week, Micron Technology, Inc. posted a stunning fiscal third-quarter performance—yet its stock suffered its steepest weekly decline in over a year. From Monday’s open at $1,139.08 to Friday’s close at $975.56, the stock plunged -14.4%, hitting a weekly low of $950.28 and a high of $1,198.71. The move was driven not by weak results, but by three simultaneous shocks: a federal antitrust lawsuit filed Thursday accusing Micron, Samsung, and SK Hynix of DRAM price-fixing; a $518.58 billion joint Korean memory-chip investment announcement; and Michael Burry’s public short entry at $1,051.87. The most violent single-day moves—Wednesday’s -10.6% and Thursday’s -5.5%—came as investors digested legal exposure and recalibrated valuation amid peak technical extension.

Micron Earnings: Why did the market sell off after a record beat?

Micron Earnings were unequivocally exceptional: $41.46 billion in revenue (up 345.7% YoY), $25.11 in adjusted EPS, and Q4 guidance of $50 billion in revenue and $31 EPS—well above consensus. Yet the market reacted with skepticism, not celebration. Analysts at Cantor Fitzgerald raised their price target to $2,000, Barclays followed with a $2,000 target, and Wells Fargo’s Aaron Rakers lifted his to $1,525. Still, the narrative shifted: Jim Lebenthal (Cerity Partners) hailed the results as a “fundamental shift” in the AI trade, while Pierre Ferragu (New Street Research) warned that 85% gross margins risk demand destruction. The tension between structural pricing power and cyclical vulnerability defined the week—making Micron Earnings both the catalyst and the casualty.

Who’s bullish—and who’s betting against Micron?

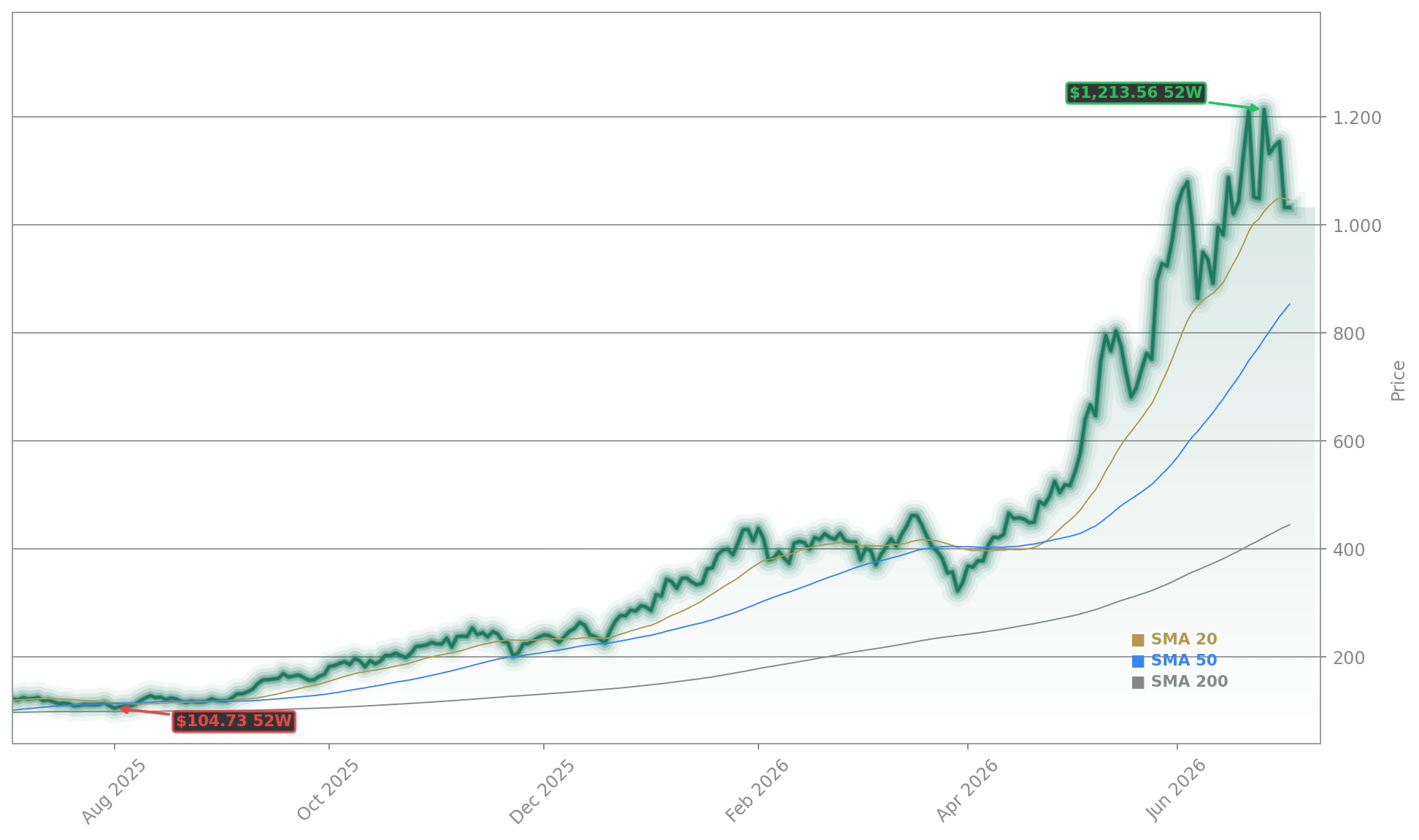

Wall Street’s bullish consensus remains intact: the average analyst price target stands at $1,542.05, with Citigroup at $1,400, Cantor Fitzgerald at $2,000, and Barclays also at $2,000. Yet dissent is now institutionalized. Michael Burry launched a direct short at $1,051.87, citing Micron’s 4% median ROIC and “destroyer of capital” history. His thesis—echoed by Stifel and Deutsche Bank in broader semiconductor caution—clashed with bulls like Bryn Talkington (Requisite Capital), who emphasized 818.73% 12-month gains and “higher highs, higher lows.” The divergence is stark: while NVIDIA and Tesla face similar AI hype, Micron’s pure-play memory exposure makes it uniquely sensitive to both supply shocks and legal risk.

What matters next week for Micron Technology, Inc.?

Next week, U.S. markets are closed Friday for the Fourth of July—so Monday’s open will be the first true test of sentiment. Key catalysts include South Korea’s KOSPI performance (where SK Hynix and Samsung rebounded 11% and 8.2% on Friday), the first trading day after the antitrust filing, and options expiration. The $991 support level—identified by technical analysts—is critical; a break below could trigger deeper selling. Also looming: the September 22, 2026 Micron Earnings report, where analysts expect $31.24 EPS and $50.72 billion revenue. Meanwhile, the company’s $100 billion U.S. manufacturing investment and $250 million Trump Accounts commitment remain politically resonant but financially immaterial in the near term.

Related Coverage: For deeper analysis on how Micron’s $100 billion customer agreements intersect with its legal and supply-chain risks, see Micron Weekly Recap: $100B Deals Face Post-Earnings Warning, where Editor-in-Chief Maik Kemper examines whether long-term contracts can insulate the company from cyclical and regulatory headwinds.

Micron defines cyclical like no other, citing 34 drawdowns of more than 30% over 42 years, a median return on invested capital (ROIC) of 4%, and return on equity (ROE) of 7%, which he called ‘frankly terrible.’— Michael Burry

Despite the sharp selloff, Micron’s fundamentals remain unchallenged: 345.72% revenue growth, $35.58 billion EBITDA, and a debt-to-equity ratio of just 0.06—stronger than NVIDIA, Apple, and all major semiconductor peers. The week’s volatility wasn’t a rejection of Micron Earnings, but a recalibration of risk. For investors, the key takeaway is that Micron has successfully de-risked its business model with 16 Strategic Customer Agreements—locking in $100 billion in minimum revenue through 2030. That durability, not just the quarterly beat, makes Micron Earnings a structural inflection point—not a cyclical peak.