Can Micron AI Memory keep dominating the AI buildout even as the stock slips on a sharp intraday pullback?

How Is Micron AI Memory Reshaping the AI Hardware Stack?

Micron Technology, Inc. is no longer just a memory supplier — it’s an AI infrastructure gatekeeper. While NVIDIA dominates GPU compute, Micron AI Memory solves the critical bottleneck: data delivery speed and capacity. HBM4 chips, now in volume shipment, deliver 60% more capacity and 20% better energy efficiency than HBM3E — a decisive edge for AI training clusters and inference servers. With NVIDIA integrating HBM4 into its Vera Rubin platform launching in H2 2026, Micron’s memory becomes inseparable from the industry’s most powerful AI systems. That tight coupling explains why Micron’s cloud memory segment surged 307% YoY to $13.7 billion — and why Wall Street now views memory as a leading indicator of AI capex momentum.

What’s Driving Micron’s Explosive Revenue Across All Segments?

AI demand is no longer confined to data centers. Micron Technology, Inc. reported record growth across all four business units: core data center (+653% to $11.5B), mobile and client (+254% to $11.5B), automotive and embedded (+311% to $4.6B), and cloud memory (+307%). The mobile surge reflects on-device AI acceleration — models like Apple’s on-device Llama variants now require higher-density DRAM, while automotive growth signals AI’s physical expansion: vehicles with basic autonomy need 5x more memory than legacy models, and humanoid robots require 10x more. This diversification insulates Micron from data center cyclicality — a key reason JPMorgan raised its price target to $1,540, citing 16 strategic customer agreements totaling $100 billion in floor-priced revenue.

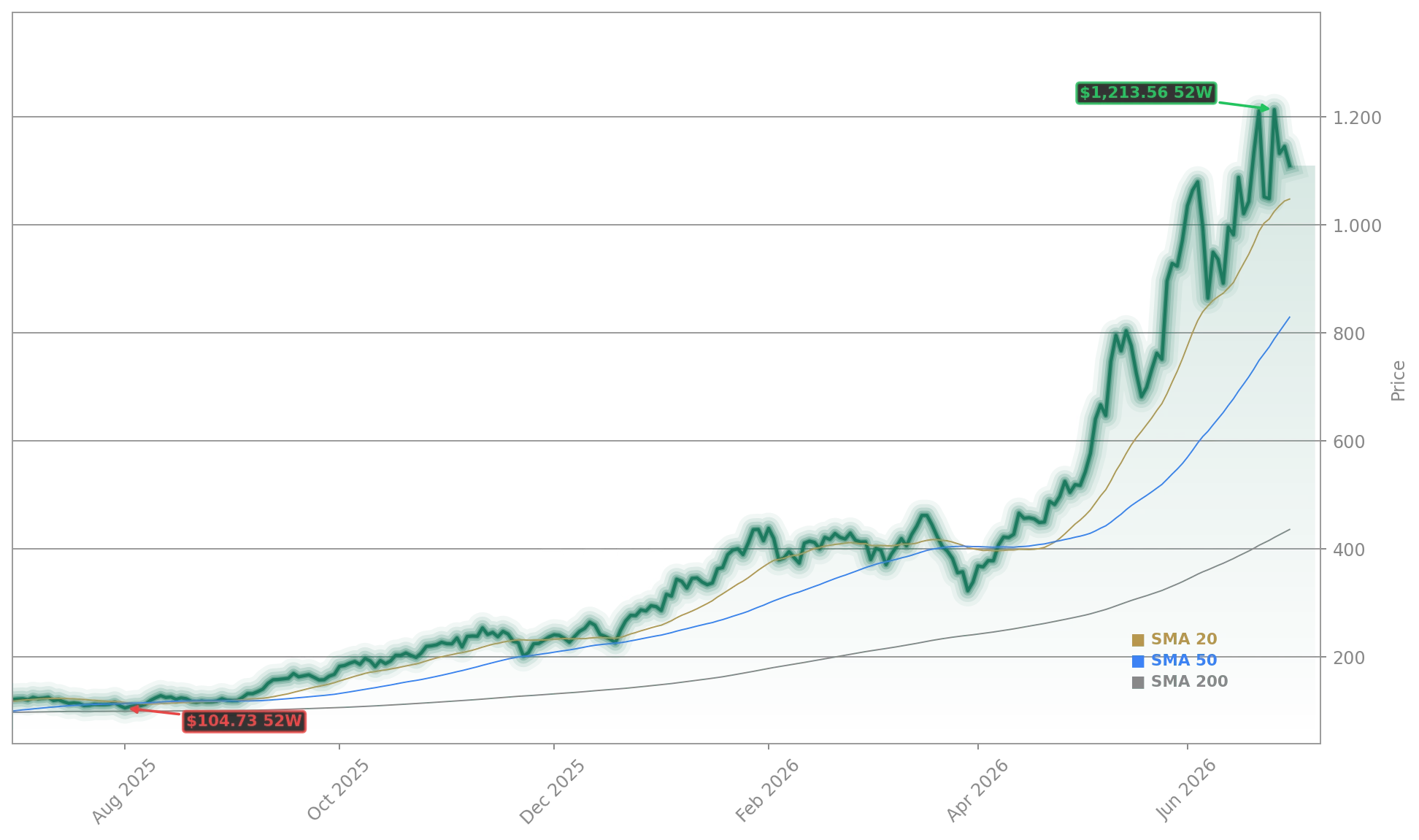

Why Is Micron Stock Rising Despite a -3.12% Intraday Dip?

Though Micron Technology, Inc. shares dipped -3.12% in early trading on July 1, the broader trend remains unbroken: +304% YTD and +800% over 12 months. That strength reflects structural pricing power — global memory shortages have pushed DRAM and NAND ASPs to all-time highs, lifting gross margins to record levels. Zacks Investment Research recently upgraded Micron to a Rank #1 (Strong Buy), citing its unmatched HBM4 execution and leadership in AI-optimized memory. Crucially, Micron’s forward P/E of just 7.6 — based on Wall Street’s $148.03 FY2027 EPS consensus — looks deeply undervalued next to the Nasdaq-100’s 34.1 multiple. As Apple CEO Tim Cook recently flagged an ‘extreme shortage’ in AI hardware, memory makers like Micron are reaping outsized rewards — even as tech end-users absorb higher input costs.

How Do Competitors Compare in the AI Memory Race?

While Seagate (STX) leverages HDDs for AI storage scale, Micron AI Memory owns the high-performance, low-latency memory layer essential for AI acceleration — a distinction Yahoo Finance Australia highlights as the core driver of Micron’s superior upside potential. AMD and Intel are gaining in AI accelerators, but neither controls memory IP or fabrication at scale. Micron’s vertical integration — from design to advanced packaging — gives it a structural advantage over fabless peers. Meanwhile, BlackRock’s recent note urges investors to look beyond chipmakers like Micron toward power infrastructure — a tacit acknowledgment that Micron’s growth is now so embedded in AI’s physical layer that it’s shifting capital allocation upstream. For U.S. portfolios, Micron remains the purest, most direct play on AI memory — and its inclusion as the fourth-largest component of the Philly Semis index underscores its systemic importance to the S&P 500’s tech leadership.

Micron Technology, Inc. remains the cornerstone of the AI memory revolution. Its record Q3 results and aggressive HBM4 rollout confirm that Micron AI Memory is not just keeping pace with AI demand — it’s defining its architecture. For investors, the opportunity lies not just in current margins, but in Micron’s expanding role across devices, vehicles, and robots — all requiring exponentially more memory. The next catalyst? Full-scale Vera Rubin deployments in Q4, which could trigger another wave of HBM4 order revisions. For growth-focused portfolios, Micron AI Memory is indispensable.

Micron’s strategic customer agreements now total 16 and represent approximately $100 billion in cumulative revenue at floor pricing — providing meaningful protection against revenue cyclicality and ensuring gross margins well above past peaks.— Harlan Sur, JPMorgan Analyst

Related Coverage: Micron’s recent earnings report — though accompanied by a -6.3% stock reaction — revealed $100 billion in strategic customer agreements that could lock in margins well into 2028, as detailed in Micron Earnings -6.3%: Shock Despite $100B AI Deals. Meanwhile, the broader AI chip race is intensifying, with Broadcom’s $22 billion inference push challenging NVIDIA’s dominance — a dynamic explored in Broadcom AI Chip: $22B Revenue Boom Fuels Inference Push.