Can Micron Earnings justify an AI supercycle narrative even as the stock drops 4.5% in regular trading?

What Do Micron Earnings Mean for the S&P 500?

The Nasdaq Composite fell 0.46% on Thursday despite Micron Technology, Inc. surging 15% — a stark reminder that the index’s leadership is fracturing. While Micron Earnings lifted semiconductor ETFs and memory peers like Western Digital (+13%) and SanDisk (+15%), broader tech sentiment cooled amid Apple’s (AAPL) 6% drop following hardware price hikes and rising inflation concerns. Crucially, Micron’s blowout quarter reinforced AI’s capital intensity: hyperscalers’ $700+ billion 2026 data center CapEx — driven by Meta, Google, Microsoft, and Amazon — is now visibly flowing into memory procurement. For the S&P 500, where tech accounts for nearly 30% of index weight, Micron Earnings underscore a growing divergence: AI infrastructure beneficiaries are accelerating, while consumer-facing tech faces margin pressure.

How Is Micron Earnings Changing the Memory Business Model?

Gone is the boom-bust playbook. Micron Technology, Inc. now operates under 16 strategic customer agreements (SCAs) — multi-year, take-or-pay contracts with floor pricing — covering 40% of revenue and expected to rise. These aren’t volume guarantees; they’re margin anchors. CEO Sanjay Mehrotra confirmed the floor price is “well above our peak quarterly margins in any past cycle” — referencing the 61% high set in 2018. With gross margins at 85% and data center margins approaching 90%, Micron is achieving pricing power once reserved for NVIDIA. The shift is structural: memory is no longer sold on spot markets but as a committed AI infrastructure component. As BNP Paribas analyst Karl Ackerman noted, this “supports demand assurance, through-cycle profitability, and mitigated cyclicality.”

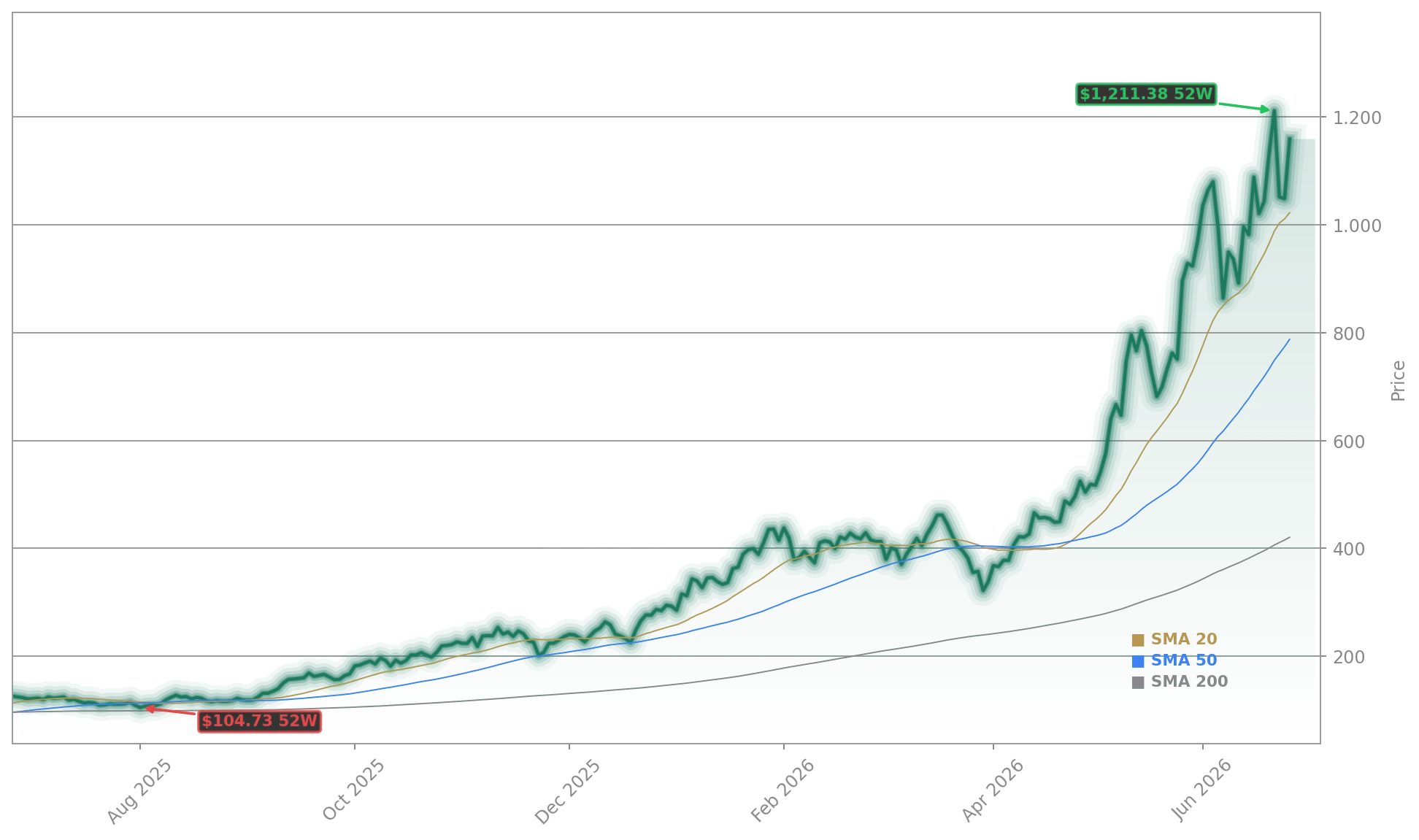

Are Analysts Rerating Micron Earnings — or Just Raising Targets?

Yes — and aggressively. Citigroup lifted its price target to $1,400. KeyBank to $1,600. Wells Fargo to $1,525. Baird to $1,280. Morgan Stanley to $1,200. Cantor Fitzgerald to $1,500. Barclays to $2,000. And Milius Capital set the most bullish mark: $2,200. Earth State Group upgraded to Buy. Collectively, 35 of 42 analysts tracked by FactSet raised fiscal 2027 EPS forecasts — the consensus now stands at $144.27, up from $101.74 just one month ago. What’s notable isn’t just the magnitude, but the rationale: analysts are pricing in sustained margin expansion, not temporary AI euphoria. With a forward P/E of just 7.5, Micron Technology, Inc. trades at half the S&P 500’s multiple — a valuation gap analysts now say is unjustified given its contracted revenue visibility and AI moat.

What’s Next for Micron Earnings and the AI Supply Chain?

Our customers are recognizing that supply shortages in memory and storage will take considerable time to improve. Even as we expect industry supply to improve gradually in 2028, we currently do not have line of sight as to when memory supply will be able to catch up with increasing demand.— Sanjay Mehrotra, CEO of Micron Technology, Inc.

Micron Earnings confirm what investors feared — and hoped — for: no meaningful supply relief before 2028. New clean-room capacity requires five years to build; existing fabs are at 100% utilization. The company can meet only 15–66% of current demand. That bottleneck is lifting the entire semiconductor ecosystem: Lam Research (LRCX) jumped 7.2% on Thursday after Wells Fargo raised its target to $450, citing Micron’s CapEx surge. Teradyne (TER) hit an all-time high. Even Qualcomm, positioning itself as a data center AI competitor, cited Micron’s memory constraints as a catalyst for its own infrastructure push. For Wall Street, the message is clear: Micron Earnings aren’t an outlier — they’re the leading indicator of AI’s hardware bottleneck, and the rally is broadening beyond chips into equipment, power, and cooling infrastructure.