Can the Micron Anthropic Partnership turn a memory maker into an AI infrastructure winner before earnings reset expectations again?

What Does the Micron Anthropic Partnership Mean for Wall Street?

The Micron Anthropic Partnership, announced Monday, June 22, spans three strategic pillars: co-design of memory and storage AI architecture, enterprise-wide deployment of Anthropic’s Claude across Micron’s operations, and a strategic investment in Anthropic’s Series H financing round. Unlike traditional supplier-customer relationships, this alliance embeds Micron directly into the AI model development lifecycle—shifting its valuation narrative from memory vendor to AI infrastructure architect. For U.S. investors, this reinforces a key theme across the NASDAQ: memory is no longer a cost center but a performance bottleneck—and Micron controls the bottleneck. The move also aligns with Bank of America’s recent designation of Micron, AMD, and Broadcom as core additions to its AI Big 10, underscoring its institutional repositioning beyond the Magnificent Seven.

How Do Analysts View Micron’s Valuation Ahead of Earnings?

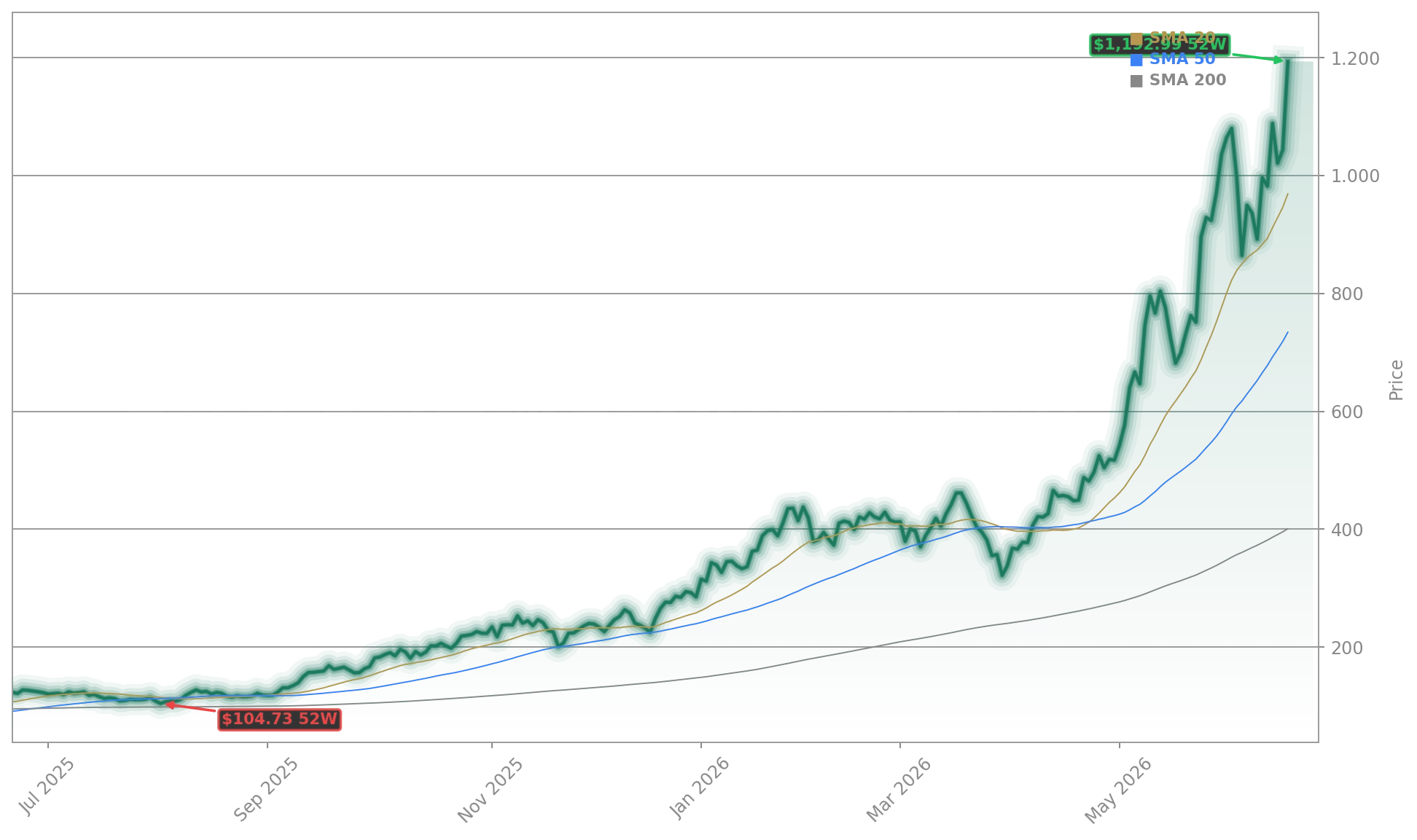

With 19 upward earnings revisions in the past month and three major price target hikes since June 18, Wall Street has moved decisively. Stifel raised its target to $1,500 from $550, citing DRAM average selling prices per GB more than doubling prior forecasts. Wedbush maintained its Outperform rating and lifted its target to $1,300, emphasizing AI-driven revenue and earnings acceleration in fiscal Q3. Needham followed suit, boosting its target to $1,550—up from $500—citing ‘stronger-for-longer’ memory fundamentals, robust pricing, and limited near-term capacity additions. Crucially, these upgrades are not speculative: they reflect confirmed HBM4 volume production for NVIDIA’s Vera-Rubin platform and sold-out 2026–2027 HBM capacity under long-term contracts. That structural visibility directly supports Micron’s forward P/E of just 9.5—far below peers like NVIDIA (22x) and Broadcom (28x) and validating its premium as a growth stock, not a cyclical play.

Why Is This Earnings Report a Make-or-Break Moment for the AI Trade?

Micron reports Q3 2026 results after market close on Wednesday, June 24—a date now viewed as a de facto stress test for the entire AI infrastructure rally. Analysts expect $34.8 billion in revenue (up 268% YoY) and $19.72 EPS (up 930% YoY), per Zacks. But as seen with Apple and Tesla, Wall Street now demands a ‘beat-and-raise’—and Micron has delivered that in 8 of its last 9 quarters. The market’s high bar is clear: good is no longer good enough. With options positioning showing 65% puts versus 35% calls and implied volatility near the 93rd percentile, traders are bracing for ±14.3% moves. A strong outlook—especially around HBM4 ramp timelines, 2027 capacity visibility, or new multiyear agreements—could propel the stock toward $1,550. A conservative guide, however, risks triggering a rotation into less volatile AI enablers like Taiwan Semiconductor or Intel.

How Does Micron Compare to Memory Peers in the S&P 500?

Micron’s dominance is structural, not just cyclical. It holds 5.27% of the Invesco QQQ ETF—more than Apple’s 7.06% or NVIDIA’s 8.08%—and commands 26.96% of the memory ETF’s weight alongside SK Hynix and Samsung. Unlike peers, Micron is the only U.S.-based leader in high-bandwidth memory with full-stack control—from HBM4 design to Idaho and New York fab expansion. Its debt-to-equity ratio of 0.15 is stronger than industry peers, and its 21.0% ROE and $18.48 billion EBITDA dwarf the sector average. While SK Hynix recently eclipsed Samsung as South Korea’s most valuable company, Micron remains the only memory stock with direct U.S. policy tailwinds—including CHIPS Act funding and export controls that limit Chinese competition. That U.S. strategic advantage, combined with its Micron Anthropic Partnership, creates a moat no global peer replicates.

We continue to work with customers on strategic customer agreements, or SCAs, that are different from prior LTAs and have specific commitments over a multiyear time horizon for improved visibility and stability in our business model.— Sanjay Mehrotra, CEO of Micron Technology, Inc.

Micron Technology, Inc. has transformed from a memory cyclical into the central nervous system of AI infrastructure—and the Micron Anthropic Partnership is its most powerful validation yet. For U.S. portfolios, this isn’t just about earnings—it’s about confirming memory’s irreplaceable role in the AI stack. With analysts uniformly bullish and valuation metrics still compelling relative to growth, the next catalyst is clear: sustained execution. The next quarterly earnings will show whether the trend continues. For long-term investors, Micron remains the purest, most scalable bet on AI’s insatiable memory demand.