Can Micron’s AI-driven memory rally keep climbing, or has Wall Street already priced in near-perfect earnings?

What’s Driving the Micron Forecast?

Wall Street’s bullish pivot stems from hard data: Micron Technology, Inc. has fully sold out its 2026 high-bandwidth memory (HBM) production under contract, with demand from hyperscalers like Meta and cloud infrastructure firms far exceeding supply. Deutsche Bank’s Melissa Weathers raised the target from $1,000 to $1,500 on June 17 — a 50% increase — citing ‘DRAM bit demand vastly outpacing supply’ driven by AI training workloads. TD Cowen’s Krish Sankar echoed the move, calling HBM adoption a ‘permanent shift,’ not a cyclical blip. This Micron Forecast surge aligns with broader semiconductor momentum: Intel jumped 6.4% on Tradegate, SK Hynix rose 7% in Seoul, and the Philadelphia Semiconductor Index (SOX) outperformed the NASDAQ despite Federal Reserve Chair Kevin Warsh’s hawkish stance on inflation.

How Does Micron Compare to Rivals?

While Micron Technology, Inc. leads in HBM3 adoption speed, its competitive position remains tense. Samsung and SK Hynix gained market share in Q2 2026 — not due to superior technology, but greater production scale and lower cost-per-bit. That dynamic pressures Micron’s margins long term, even as near-term pricing power soars. Compared to NVIDIA, which commands 80x forward P/E, Micron trades at 48x — still rich, but cheaper than a year ago on a forward EPS basis. Analysts note that while NVIDIA designs AI accelerators, Micron enables them: every A100, H100, and Blackwell GPU requires 12–24 HBM stacks. That symbiotic relationship underpins the Micron Forecast resilience — even as valuation debates intensify.

Is the AI Memory Boom Sustainable?

Yes — but with caveats. Plurimi Wealth CIO Patrick Armstrong told Bloomberg Television that his firm is ‘underweight the Magnificent Seven’ and instead owns ‘the companies they’re giving the money to’ — naming Micron Technology, Inc., Samsung, and NVIDIA. Yet the memory industry’s boom-bust history remains a structural risk. Wall Street expects peak DRAM pricing in 2028, with 2029 revenue forecasts dropping sharply. Meanwhile, SpaceX’s newly announced $8 billion semiconductor investment — and Meta’s $50 billion AI capex plan — extend near-term visibility. TradingView notes Micron’s Zacks Rank #1 (Strong Buy) reflects ‘exceptional returns’ and ‘robust gross margin growth’ — validating the current Micron Forecast optimism, even amid bubble warnings.

What’s at Stake in the June 24 Earnings Report?

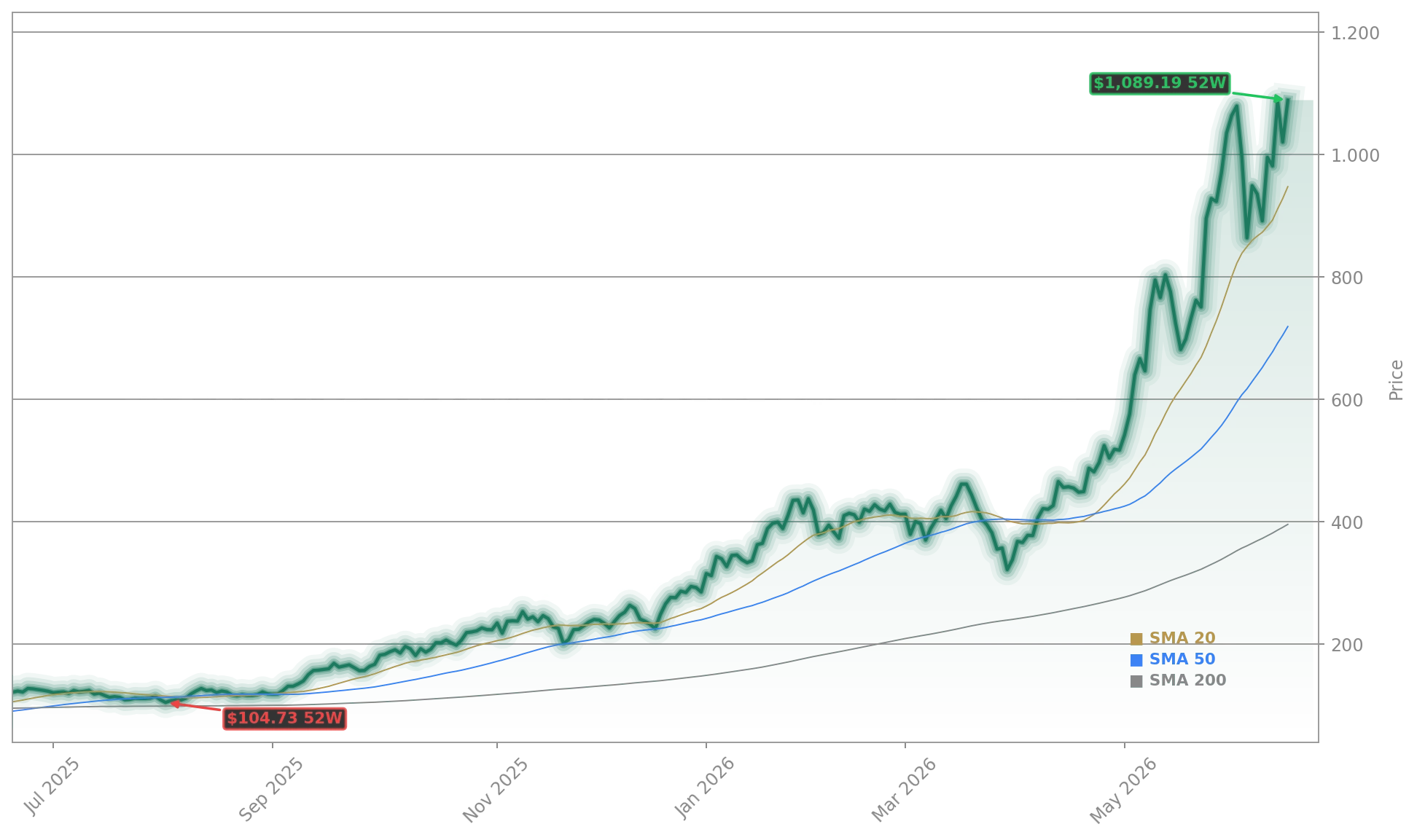

Micron’s Q3 2026 report — due Tuesday, June 24 — is expected to deliver $35.06 billion in revenue and $20.25 in EPS, per TradingView consensus. That’s a 196% jump from last year’s $23.8 billion and a 682% surge in non-GAAP net income — numbers that would dwarf even Marvell’s AI-fueled +5.5% rally. But investors will scrutinize gross margin guidance, HBM4 ramp timing, and capital expenditure plans. A miss on long-term supply commitments could trigger volatility — especially given the stock’s 1,940% gain since January 2023, far outpacing Apple and Tesla. With shares up 3.45% today and trading above $1,090, the market has priced in perfection. Yet Deutsche Bank, Citi, and RBC Capital Markets all maintain Buy ratings — signaling confidence in the Micron Forecast durability.

Related Coverage

We’re underweight the Magnificent Seven — the hyperscalers — those are the companies that are spending a trillion dollars over the next 12 months on AI datacenters. And we own the companies they’re giving the money to.— Patrick Armstrong, Plurimi Wealth CIO

For deeper context on Micron’s earnings dynamics, readers should review “Micron Earnings -2.9%: Warning Signs Despite Record Revenue”, which explores supply bottlenecks amid AI-driven top-line growth. Also critical is “Marvell AI Boom +5.5% as S&P 500 Entry Fuels Surge”, highlighting how infrastructure enablers — not just chip designers — are capturing outsized value in the AI build-out. Both pieces underscore that Micron’s strength lies not in hype, but in irreplaceable hardware leverage.