Can Marvell’s AI-fueled rally keep climbing as S&P 500 inclusion and hyperscaler demand collide?

Why Is Marvell Technology, Inc. Outpacing the NASDAQ?

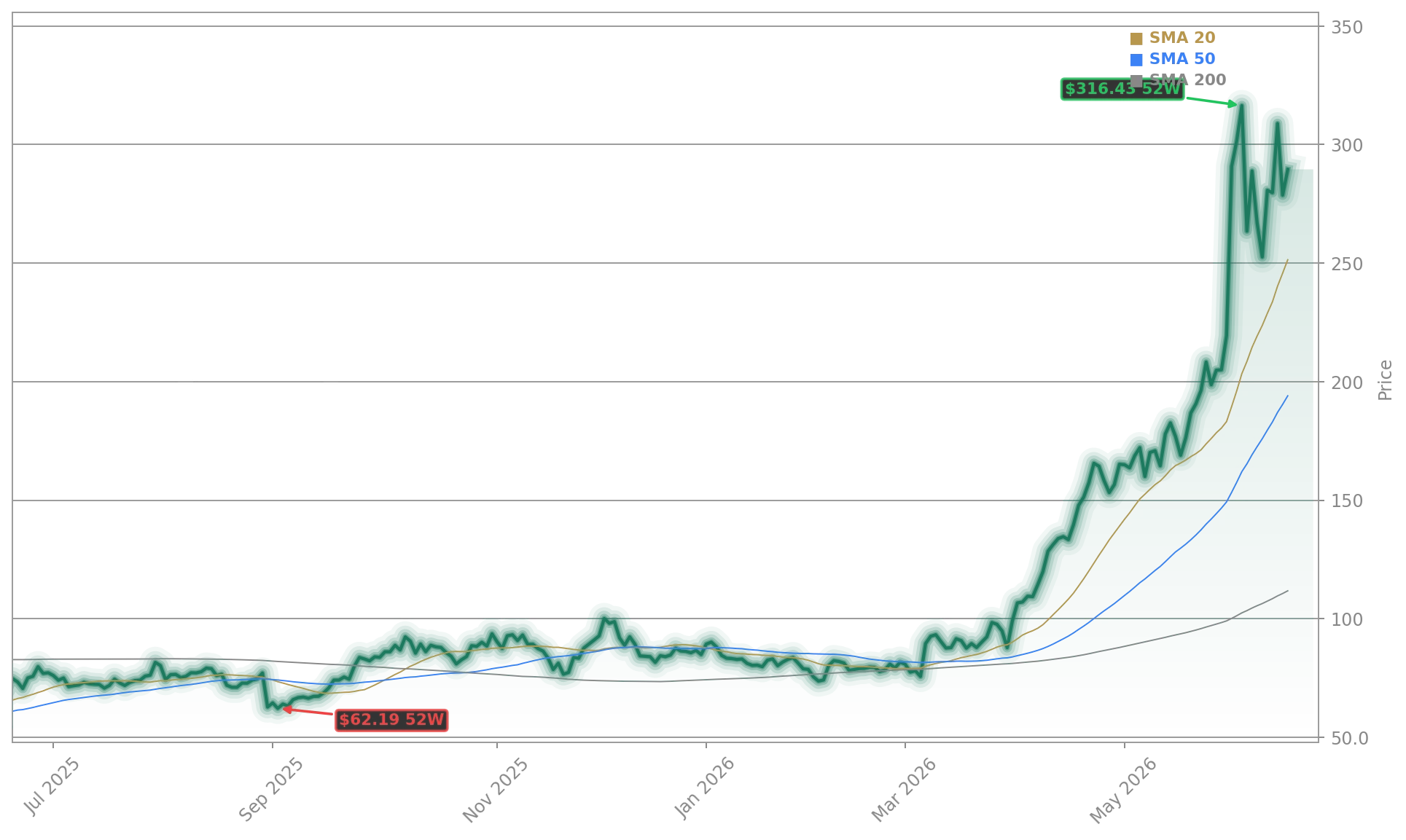

Marvell Technology, Inc. has delivered a jaw-dropping 57% rally over the past 30 days — far exceeding the NASDAQ’s 8.2% gain in the same period. Unlike broad-based tech indices, Marvell’s strength is hyper-focused: its custom AI accelerators, optical interconnects, and infrastructure ASICs are now embedded in the next-gen data centers of Meta, Microsoft, and Amazon. With revenue up 27.6% year-over-year to $2.42 billion in Q1 FY2027 and guidance for Q2 EPS of $0.88–$0.98, the company is executing against its AI roadmap with surgical precision. Analysts at Morgan Stanley recently raised their price target to $235, citing ‘unmatched design-win momentum in AI networking stacks.’

How Does the Marvell AI Boom Compare to NVIDIA and AMD?

The Marvell AI Boom isn’t occurring in isolation — it’s part of a broader semiconductor renaissance led by NVIDIA, Advanced Micro Devices, and Marvell Technology, Inc. While NVIDIA dominates AI training chips, Marvell owns critical infrastructure layers: high-speed SerDes, retimers, and co-packaged optics that enable AI clusters to scale without thermal or latency bottlenecks. In contrast, AMD’s AI growth remains tied to MI300 adoption, and Intel’s Gaudi roadmap faces delays. Marvell’s revenue from custom AI silicon alone is projected to exceed $10 billion by fiscal 2029 — a trajectory that has attracted attention from Citigroup, which upgraded MRVL to ‘Buy’ with a $240 price target last week.

What’s Driving the S&P 500 Inclusion Rally?

Marvell Technology, Inc. joins the S&P 500 on Sunday, June 22 — a milestone that triggers mandatory buying from over $14 trillion in index-linked assets. Historically, S&P 500 additions see +3.8% average gains in the 10 days before inclusion, per Barron’s analysis. Marvell’s inclusion validates its scale: $2.42 billion in Q1 revenue, $250 billion market cap, and profitability across multiple product lines. Yet unlike past index additions, MRVL is already trading above the consensus analyst price target of $224.68 — a signal that market expectations have surged ahead of fundamentals. RBC Capital Markets notes the move reflects ‘a structural re-rating, not just a technical event.’

Are Valuation and Insider Activity Red Flags?

Yes — but not dealbreakers. Marvell Technology, Inc. trades at 71x forward earnings, well above the S&P 500’s 21x average. And in the past 90 days, insiders have sold $31.96 million worth of shares — including outgoing CFO Willem Meintjes’ planned $65.3 million sale. Still, the new CFO, Dan Durn (ex-Adobe), has reaffirmed full-year guidance and emphasized ‘record AI design-win velocity.’ The disconnect between valuation and execution underscores a key Wall Street theme: investors are paying a premium not for current earnings, but for Marvell’s irreplaceable role in AI’s physical layer — a role that neither Tesla nor Apple can replicate. As Goldman Sachs puts it: ‘This is infrastructure, not cyclical semiconductor exposure.’

Related Coverage: Marvell’s AI infrastructure surge was spotlighted just yesterday in Marvell AI Infrastructure Jumps 9.7% as AI Bets Build, where analysts highlighted record bookings in optical interconnects. Meanwhile, the broader AI infrastructure challenge is explored in Microsoft AI Strategy: $37B Boom Faces Capex Warning, underscoring why companies like Marvell Technology, Inc. are becoming indispensable to hyperscaler capex plans.

This is infrastructure, not cyclical semiconductor exposure.— Goldman Sachs

Marvell Technology, Inc. remains the definitive infrastructure play in the Marvell AI Boom. For investors seeking AI exposure beyond chip design, MRVL offers unique leverage to the data center buildout — not just the chips inside them. The June 22 S&P 500 inclusion is a catalyst, not an endpoint. The next quarterly earnings report will test whether the Marvell AI Boom can sustain its velocity into Q2 FY2027.