Can Micron Earnings and a blockbuster Anthropic deal still justify sky-high AI expectations after a brutal 10.3% sell-off?

What Does the Anthropic Deal Mean for Micron?

The June 22 announcement of a multi-layered agreement with Anthropic—a $1.550 billion strategic bet—transformed Micron Technology, Inc. from a supplier into a co-architect of next-generation AI infrastructure. The pact includes joint development of HBM, DRAM, and SSDs optimized for Claude’s training and inference workloads; a multiyear supply commitment; enterprise-wide deployment of Claude across Micron’s engineering and manufacturing; and a direct investment in Anthropic’s Series H funding round. Needham analyst N. Quinn Bolton cited the deal as evidence of ‘the strategic importance of memory in AI’ when raising his price target to $1,550 from $500—calling it ‘the most aggressive target on Wall Street.’ Bernstein’s Mark Li followed with a $1,300 target, citing ‘insatiable demand for DRAM-based HBM’ that will drive ‘almost vertical’ profit growth in 2026 and beyond.

Are Micron Earnings Still Enough to Move the Stock?

History says no—unless guidance shatters expectations. Micron Technology, Inc. has beaten earnings in seven of the last nine quarters, yet the stock rose after earnings only once in the past six. Analysts now expect $20.57 EPS on $35.01 billion in revenue—a 987% and 284% YoY surge, per FactSet. But Wall Street’s new standard is ‘beat-and-raise.’ Whisper numbers are even higher: Bank of America forecasts $22.17 EPS, Morgan Stanley $21.31, and Needham $20.97. Crucially, the market will scrutinize commentary on DRAM pricing sustainability, HBM4 ramp timing, and whether management confirms new multiyear supply agreements beyond the one with Anthropic. As Morgan Stanley’s Joseph Moore noted, ‘Micron may announce additional deals—but don’t expect clarity on terms, as they’re in active conversations with multiple customers.’

How Does Micron Compare to Its Memory Peers?

While Micron Technology, Inc. trades at a 53.5x trailing P/E, its forward P/E sits at just 11x—significantly below peers like Broadcom (28x) and NVIDIA (32x). That valuation cushion reflects both its U.S.-only manufacturing base and its leadership in high-margin HBM, where it holds ~21% market share behind SK Hynix’s 61%. Yet the sector’s concentration is stark: Micron, SK Hynix, and Samsung control 89% of the global DRAM market, per Counterpoint Research. This oligopoly, combined with AI-driven capacity constraints, has lifted DRAM and NAND pricing by triple digits. UBS and Susquehanna both project $1,600 price targets, citing ‘structural expansion’ in memory demand driven by agentic AI—not just training, but inferencing and real-time reasoning. Meanwhile, Western Digital and SanDisk have rallied alongside Micron, confirming the entire memory complex remains tightly correlated.

Is the AI Memory Supercycle Real—or Just Cyclical Hype?

The $1.3 trillion memory market is forecast to hit $1.28 trillion in 2027, per TrendForce—up 44% from 2026. DRAM revenue alone is projected to surge 46% to $903 billion. But skeptics warn of looming supply relief: Chinese producers ChangXin and Yangtze Memory are expanding capacity, with Yangtze’s new factories set to double output by end-2027. ING economist Min Joo Kang expects DRAM prices to soften around 2028. Yet Micron Technology, Inc.’s current HBM capacity is sold out through 2027, and CEO Sanjay Mehrotra has repeatedly called memory ‘a strategic asset’—a narrative shift from cyclical supplier to AI infrastructure partner. The question isn’t whether demand will soften, but whether the AI-driven structural shift in memory’s role will delay the next downturn far beyond historical precedent.

Micron Earnings: What’s the Real Risk for Investors?

We believe the memory market has continued to strengthen over the past 90 days and see market fundamentals remaining stronger for longer as a result of continued strong demand, a robust pricing environment, and limited capacity additions.— N. Quinn Bolton, Needham analyst

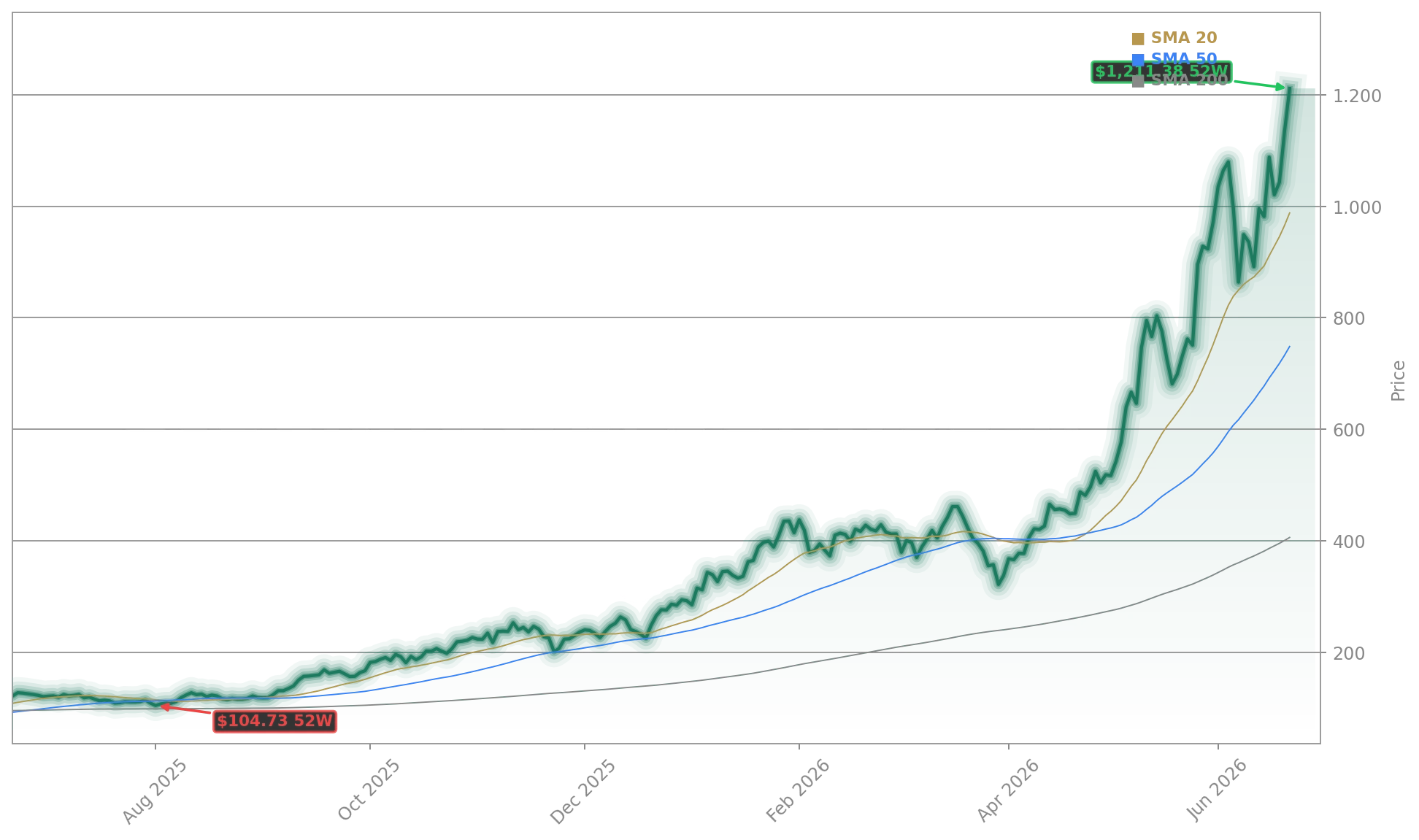

Valuation risk remains acute. At $1,211, Micron Technology, Inc. trades at 22x sales—well above the tech sector average of 8x—yet its forward P/E of 11x suggests markets price in massive earnings acceleration. The 24/7 Wall St. model forecasts $749.68 in 12 months, citing memory’s historical cyclicality as the primary downside catalyst. Insider activity shows net selling across 102 recent transactions. But bullish momentum is undeniable: Micron contributed 10 points to the S&P 500’s daily gain, its options IV sits at 116—the highest in the index—and its Benzinga Edge Momentum score ranks in the 99th percentile. With Polymarket pricing a 97% probability of an EPS beat, the real risk isn’t missing the number—it’s missing the narrative pivot.