Can Micron’s blockbuster earnings and $100 billion customer deals outweigh lawsuits, new supply fears, and a high-profile short call?

What triggered Micron’s sharp reversal after earnings?

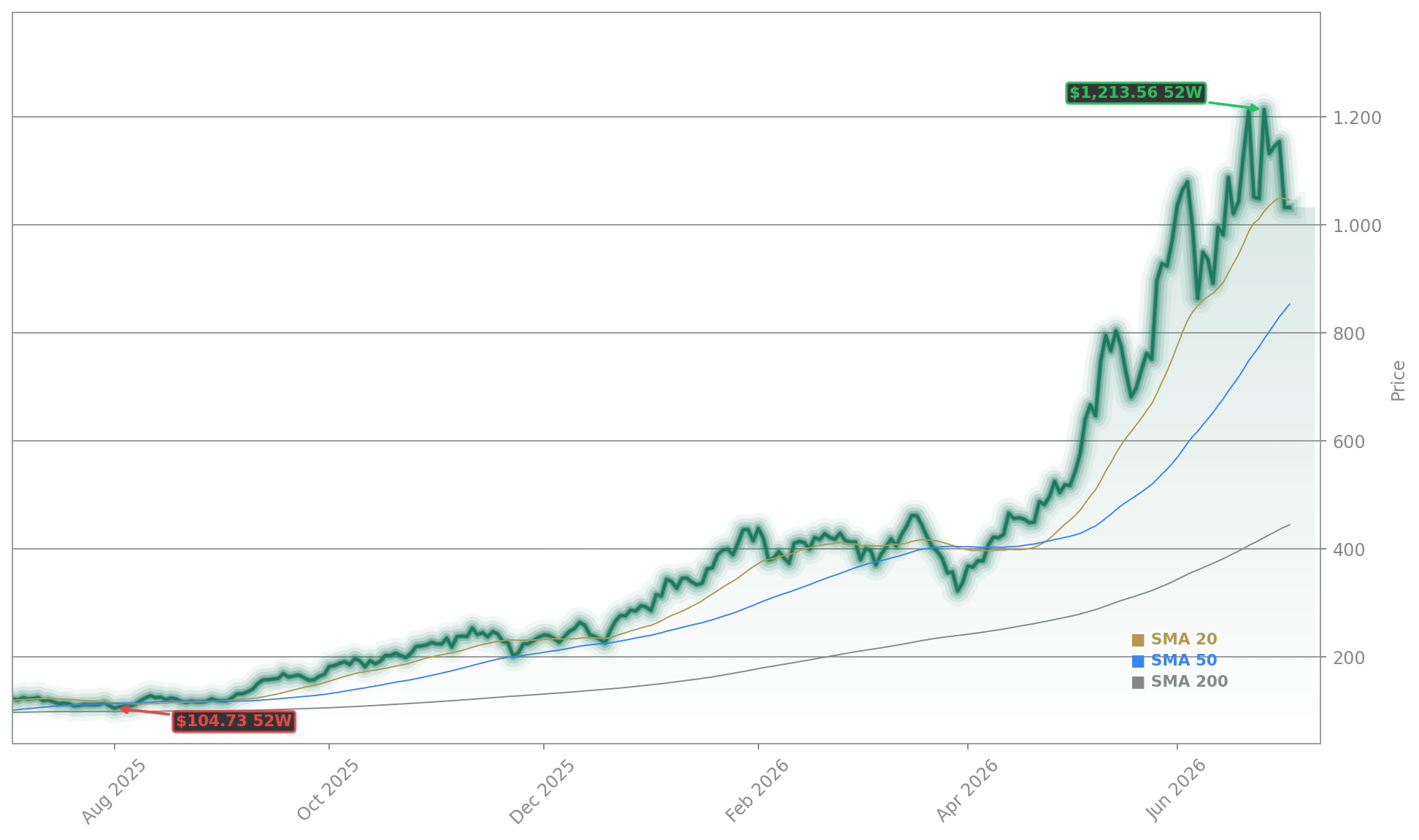

This week’s Micron Weekly Recap centers on a powerful divergence: stellar fundamentals versus escalating sentiment risks. Micron Technology, Inc. had soared to a record $1,255 on Thursday, June 26 — the day after its blowout fiscal Q3 report — only to lose over 20% in the following three trading sessions. The catalyst was threefold: a federal antitrust class-action lawsuit filed in California accusing Micron, Samsung, and SK Hynix of DRAM price-fixing; South Korea’s announcement of a $518.58 billion memory-chip investment by its two rivals; and Michael Burry’s public disclosure on July 2 that he had shorted Micron at $1,051.87 — calling it a structural ‘destroyer of capital’ with ‘frankly terrible’ 4% median ROIC. These developments triggered a broad-based tech selloff, with the KOSPI plunging 7.9% on Thursday as SK Hynix and Samsung fell 14.6% and 9.1%, dragging down Micron’s U.S. peers.

Price action over the week

Micron Technology, Inc. posted a weekly performance of -14.4%, falling from Monday’s open of $1,139.08 to Friday’s close of $975.56. The weekly high stood at $1,198.71, while the weekly low plunged to $950.28. Three outlier days drove the decline: Wednesday’s -10.6% drop — the steepest single-day loss since March — followed by Thursday’s -5.5% and Friday’s -6.7% slide. The Wednesday plunge coincided with the lawsuit’s public emergence and Burry’s Substack post; Thursday’s fall reflected global contagion as Korean memory stocks collapsed; and Friday’s close confirmed the depth of the sentiment shift, though the stock rebounded 0.31% in after-hours trading — hinting at early stabilization.

What did analysts say about Micron’s valuation and strategy?

Despite the selloff, analyst confidence remained robust — and in some cases, intensified. Wells Fargo maintained its Overweight rating and raised its price target from $1,220 to $1,525 — implying ~35% upside. Cantor Fitzgerald lifted its Overweight target from $1,500 to $2,000, while Barclays and Citigroup also raised their targets to $2,000 and $1,400, respectively. The consensus price target now stands at $1,542.05. Analysts highlighted Micron’s 16 Strategic Customer Agreements — covering $100 billion in minimum revenue commitments through 2030 — as a structural de-risking of its historically cyclical model. As Wells Fargo’s Aaron Rakers noted, these take-or-pay contracts deliver pricing floors, margin stability, and visibility that justify a premium valuation — even as short-term sentiment wobbles.

How do Micron’s peers and macro trends shape its outlook?

Micron Technology, Inc. remains tightly linked to NVIDIA, Apple, and Tesla — not as direct competitors, but as critical customers and ecosystem anchors. Apple raised Mac and iPad prices citing memory costs; NVIDIA’s AI chips depend on Micron’s HBM; and Tesla’s AI-driven vehicle computing requires memory bandwidth. Simultaneously, macro pressures mounted: the $518.58 billion Korean investment signaled long-term supply expansion, though analysts at Barron’s stressed it won’t impact pricing until late 2027 or 2028. Meanwhile, New Street Research’s Pierre Ferragu warned that current DRAM gross margins near 90% — implying fivefold price increases — risk demand destruction. Yet BofA’s Wamsi Mohan expects NAND supply/demand imbalance to persist through 2027, reinforcing the scarcity thesis.

Micron Weekly Recap: What matters next week?

With U.S. markets closed Monday for the Fourth of July, the focus shifts to overseas signals: South Korea’s KOSPI rebounded 5.8% on Friday — SK Hynix rose 11%, Samsung 8.2% — suggesting potential stabilization. Next week’s key catalysts include the release of the U.S. June jobs report (Friday, July 10), potential early legal responses to the antitrust suit, and continued monitoring of insider activity — including VP Arnzen’s Form 144 filing to sell 40,000 shares. Investors will also watch for pre-earnings positioning ahead of Micron’s next report on September 22, 2026, where consensus forecasts $50.72 billion in revenue and $31.24 EPS. The central question remains: is this a technical correction — or the first crack in the AI memory narrative?

Micron Earnings: $100B AI Boom Meets Antitrust Warning dissects how the company’s record $41.46 billion fiscal Q3 revenue and $25.11 EPS coexist with mounting legal and competitive risks — asking whether the antitrust suit could delay or dilute future Strategic Customer Agreements. The article also explores how Burry’s short bet intersects with institutional positioning, and whether the $100 billion in committed SCA revenue provides sufficient insulation against near-term volatility.

Micron defines cyclical like no other, with 34 drawdowns of more than 30% over 42 years, a median return on invested capital (ROIC) of 4%, and return on equity (ROE) of 7%, which he called ‘frankly terrible.’— Michael Burry

Key takeaway: This week’s Micron Weekly Recap underscores that Micron Technology, Inc. is no longer just a memory play — it’s a barometer for AI infrastructure confidence. The -14.4% move was not a fundamental reversal, but a sentiment reset. With $100 billion in locked-in revenue, industry-leading gross margins, and analyst targets averaging $1,542, the long-term thesis remains intact. For investors, the dip presents not panic, but precision — a chance to align with a company transforming from cyclical commodity supplier into the AI economy’s most dependable memory partner. This Micron Weekly Recap confirms that volatility is the price of leadership — and leadership is precisely what Micron has seized.