If Tesla Deliveries hit a record, why is Wall Street suddenly more worried about margins than momentum?

Why Did Tesla Deliveries Beat Spark a Sell-Off?

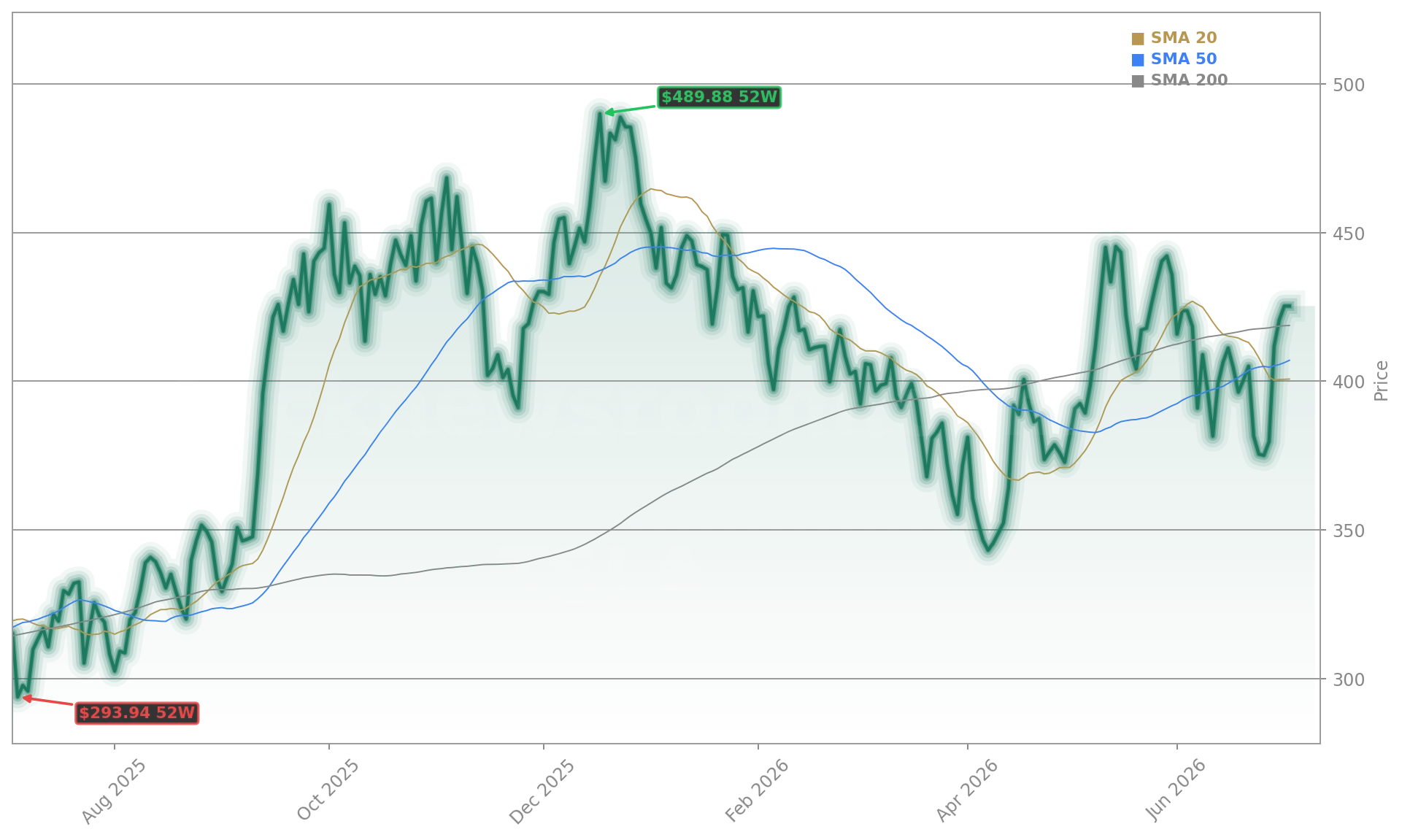

Despite shipping more vehicles than ever — 480,126 units, including 451,758 produced and 28,368 drawn from inventory — Tesla (TSLA) fell sharply in after-hours trading. The reaction reflects structural fatigue: investors have grown wary of delivery-driven rallies absent corresponding margin expansion. RBC Capital Markets maintained its ‘Outperform’ rating but emphasized that ‘vehicle gross margin sustainability — not volume — will dictate near-term price action.’ Tesla’s Q2 automotive gross margin is expected to dip to 19.8% (from 21.1% in Q1), pressured by aggressive Model Y L pricing, rising warranty accruals, and lower ASPs in Europe. That’s a stark contrast to NVIDIA, where Q2 earnings delivered both revenue growth and expanding AI chip gross margins — reinforcing Wall Street’s preference for tech with clear, scalable unit economics.

Is the US Market Really Crumbling?

Cox Automotive estimates Tesla’s US sales fell 20% year-over-year in Q2 — a direct consequence of expired federal EV tax credits and tightening consumer budgets amid elevated interest rates. While Tesla Deliveries surged globally, the US accounted for just 29% of total volume, down from 37% a year ago. That geographic shift is alarming for a company whose valuation assumes domestic pricing power. Meanwhile, BYD overtook Tesla in global BEV deliveries for the first time in Q2 — a symbolic blow that’s resonating across the S&P 500’s auto and tech sectors. Analysts at Citigroup warn that ‘without a US rebound by Q4, Tesla risks being reclassified from growth to value — with implications for its NASDAQ weight and index inclusion.’

What’s the Model Y L Really Supposed to Fix?

Tesla’s U.S. launch of the Model Y L — priced from $61,990 and shipping this October — is both a tactical response and a strategic pivot. With the Model S and X discontinued to free capacity for Optimus and Cybercab, the Y L fills a critical gap in Tesla’s premium SUV lineup. Its 325-mile range, three-row seating, and FSD-included Launch Series aim squarely at affluent suburban families — a demographic increasingly underserved by Tesla’s current portfolio. But early data is mixed: while European registrations spiked (Germany +318% in June), Norway’s EV market collapsed 43% after subsidy cuts — a cautionary tale for U.S. rollout timing. Morgan Stanley notes that ‘the Y L’s success hinges less on specs and more on whether it can command a $10,000+ premium over the standard Y — without cannibalizing existing demand.’

What’s Happening at Gigafactory Texas on July 7?

Tesla’s competitive advantage is manufacturing.— Lars Moravy, Tesla Vice President of Vehicle Engineering

Tesla Vice President of Vehicle Engineering Lars Moravy teased ‘cool news’ from the Austin campus on July 7 — widely interpreted as a Cybercab production ramp, regulatory approval for pedal-free operation in Texas, or even a humanoid robot manufacturing milestone. Unlike Apple’s predictable product cycles, Tesla’s AI roadmap remains opaque — fueling skepticism. Michael Burry’s recent short position on Tesla, disclosed via Substack, targets what he calls ‘the AI super bubble’ — specifically citing overvaluation relative to near-term cash flow. That bet gained traction as Tesla’s forward P/E remains at 226x, dwarfing the S&P 500’s 21x and even Tesla’s own historical median of 120x. The market isn’t rejecting Tesla Deliveries — it’s demanding evidence that autonomy and robotics can generate margins, not just headlines.