If Tesla Deliveries just hit a record, why did Wall Street punish the stock instead of rewarding it?

Why Did Tesla Deliveries Beat — But the Stock Fell?

Tesla Deliveries surged to 480,126 units in Q2 2026 — up 25% YoY and 34% sequentially — fueled by strong European demand and a final rush for discontinued Model S and X variants. Yet the stock plunged nearly 8% on Thursday, its largest single-day drop in nearly a year. The disconnect reflects a broader market shift: Tesla is no longer priced as an automaker. With margins under scrutiny and AI progress lagging behind Alphabet’s Waymo and NVIDIA’s DRIVE platform, investors are discounting delivery volume in favor of software monetization and autonomous scalability. Notably, Tesla produced only 451,758 vehicles — meaning it drew down inventory to meet demand, a tactic that won’t sustain long-term growth without margin expansion.

How Does Tesla Deliveries Compare to BYD and Legacy Automakers?

While Tesla Deliveries set a new quarterly record, BYD overtook Tesla in total battery-electric vehicle shipments globally in Q2 — delivering over 520,000 units. That shift highlights intensifying competition as Chinese EV makers gain scale, pricing power, and battery cost advantages. Meanwhile, traditional automakers like Ford and General Motors posted flat or declining EV deliveries amid supply chain constraints and slower-than-expected EV adoption in the U.S. Tesla’s 25% YoY growth stands out — but its U.S. sales reportedly fell 20% YoY, per Cox Automotive, underscoring reliance on international markets. In Germany alone, Tesla’s June registrations surged 318%, while the broader market rose just 15.7% — a stark divergence that may not persist without U.S. policy support.

What’s Next for Tesla’s Model Y L and Product Pipeline?

Tesla’s U.S. launch of the three-row Model Y L — priced from $61,990 and shipping in October — is a strategic pivot to fill the gap left by discontinued Model S and X. The vehicle, already a hit in China with over 120,000 units sold in its first month, adds premium pricing power and family-oriented appeal. Its inclusion of heated/ventilated front seats, power-reclining third row, and 325-mile range positions it against Apple-adjacent mobility ecosystems and NVIDIA-powered rivals. Crucially, the Model Y L Launch Series bundles 12 months of free Supercharging and Full Self-Driving — accelerating software adoption. With Tesla’s FSD subscriber base now at 1.28 million (+51% YoY), the Model Y L could become a key catalyst for recurring revenue — if regulatory tailwinds materialize.

Is Tesla’s AI Bet Still Credible to Wall Street?

Despite Tesla Deliveries strength, Wall Street remains skeptical about AI execution. Truest analyst William Stein raised his price target to $430 but maintained a ‘Hold’ rating, citing ‘no updates on AI projects or new vehicle timelines.’ RBC Capital Markets, meanwhile, reaffirmed its ‘Outperform’ rating with a $475 target, emphasizing Tesla’s energy storage growth — now at 13.5 GWh installed capacity — as a more tangible near-term driver. Meanwhile, Alphabet’s Waymo has launched fully driverless robotaxis in San Francisco and Austin, while Tesla’s Cybercab service remains limited to a few dozen Model Y-based vehicles in Texas. Lars Moravy, Tesla’s VP of Vehicle Engineering, teased ‘cool news’ from the Austin campus on July 7 — possibly signaling Cybercab production scale-up or regulatory approval. But until Tesla demonstrates autonomous economics at scale, investors will continue pricing the stock like a tech platform in waiting — not a delivery machine.

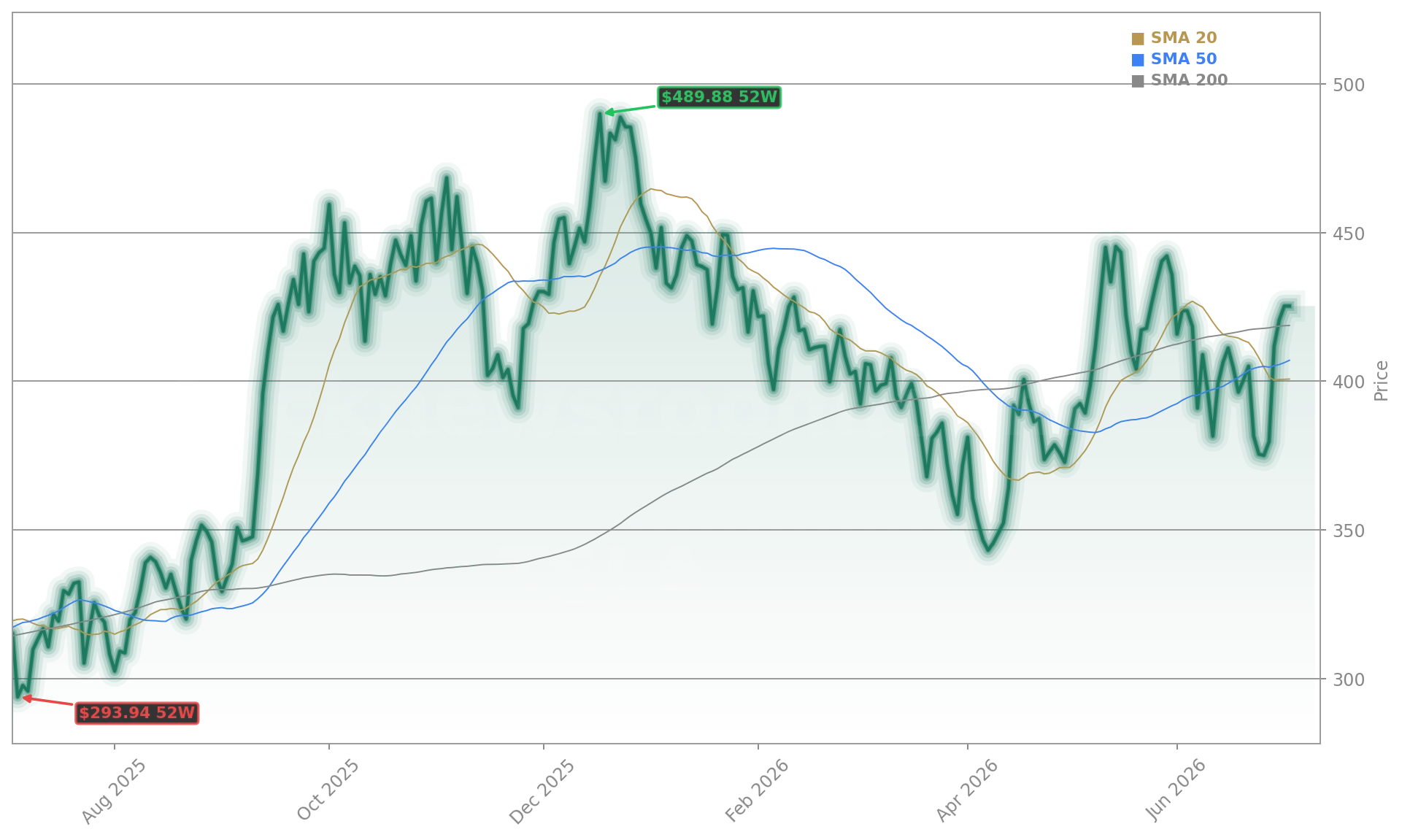

What Do Tesla Deliveries Mean for the S&P 500 and NASDAQ?

Tesla remains the fifth-largest component of the S&P 500 and a key driver of NASDAQ volatility — especially amid the ‘MAG-7’ rotation. Its 14% YTD underperformance (versus the S&P 500’s +12%) has weighed on tech-heavy indices, while its $1.9 trillion market cap gives it outsized influence on sector ETFs. With Q2 deliveries confirming demand resilience, the real test comes on July 22: automotive gross margin, FSD revenue contribution, and Cybercab progress will dictate whether Tesla can re-enter the ‘AI growth stock’ narrative — or remain a high-beta auto stock trading on delivery cadence alone. For U.S. portfolios, Tesla Deliveries are no longer the headline — they’re the baseline. The future hinges on what Tesla builds *beyond* the car.

Related Coverage: Tesla’s Q2 delivery beat triggered a wave of reassessment — Tesla Deliveries Hit 480K as Record Beat Meets Stock Warning dives into why Wall Street is treating strong deliveries as a ‘sell-the-news’ event amid mounting margin and AI execution risks.

Tesla’s competitive advantage is manufacturing.— Lars Moravy, Tesla VP of Vehicle Engineering

Tesla Deliveries confirm demand remains intact, but the company’s valuation hinges on autonomous scale, not unit volume. For long-term investors, the July 22 earnings report will reveal whether Tesla’s delivery strength translates into sustainable margin expansion and AI monetization. Until then, the stock remains a barometer for investor patience with the AI transition — and a critical test for the S&P 500’s tech leadership. Tesla Deliveries are the foundation — now the platform must deliver.