Did Tesla Deliveries really signal strength in Q2, or did the big beat simply hide a deeper US demand problem?

What Do Tesla Deliveries Reveal About US Demand?

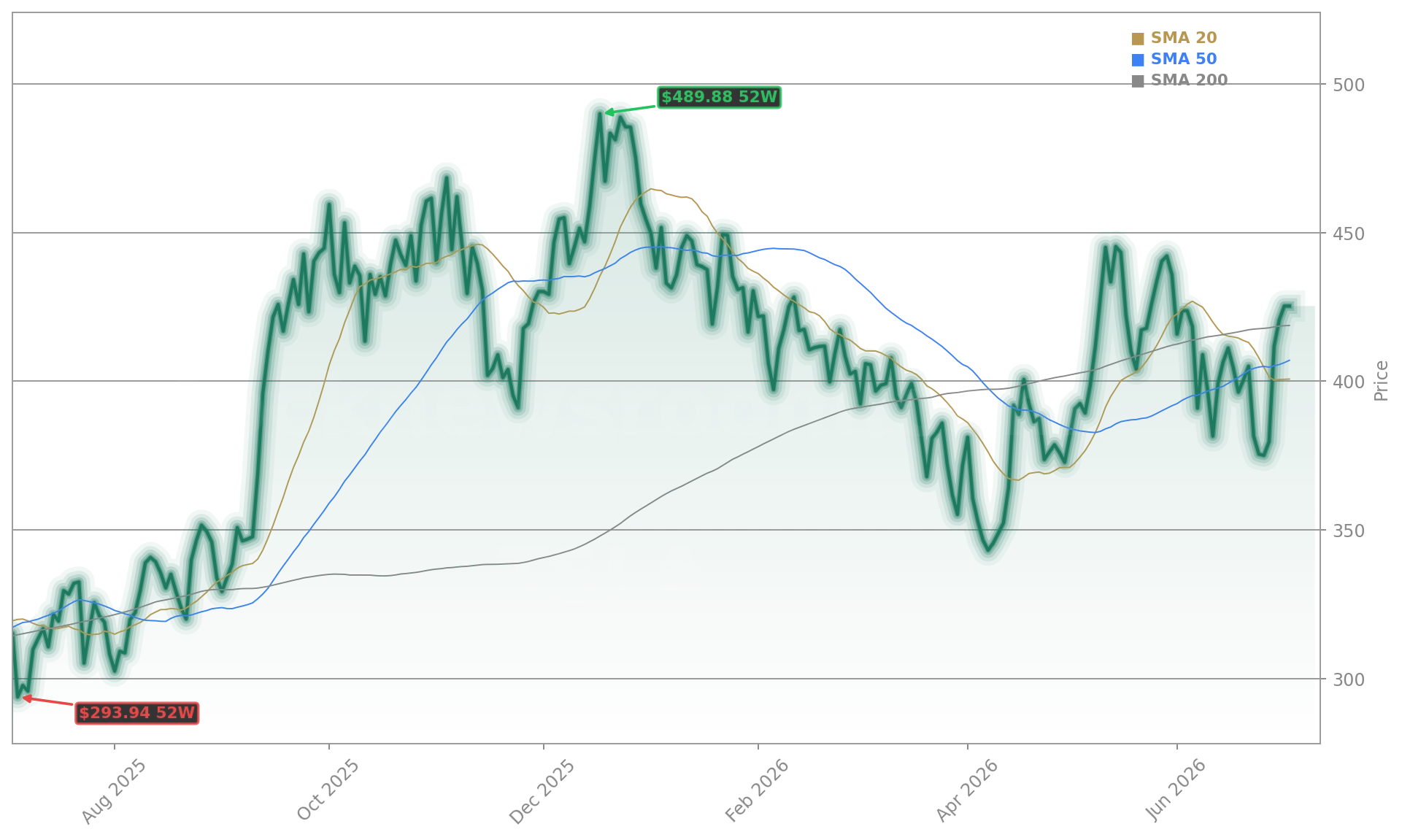

Tesla Deliveries for Q2 2026 smashed estimates — 480,126 units shipped, 25% higher than last year and well above the 406,024 consensus. Yet the headline number masks a stark regional divergence: while European registrations surged (Germany +318% in June), US sales fell an estimated 20% year over year, per Cox Automotive. That gap explains Thursday’s 7.5% intraday selloff — Tesla (TSLA) closed at $393.14, down 0.08% on the day but down sharply from its $420.60 Q2 close. The disconnect highlights a core tension: Tesla Deliveries are rising globally, but not where margins matter most — the US. With federal EV tax credits fully phased out, price sensitivity is intensifying. Tesla’s shift to lower-priced Model 3/Y trims helped lift volume, but analysts warn it’s compressing automotive gross margins — now under the microscope ahead of the July 22 earnings report.

How Does the Model Y L Fit Into Tesla’s US Strategy?

The Model Y L — a three-row, 325-mile-range SUV launching in US showrooms this October — isn’t just another variant. It’s Tesla’s direct answer to the US market’s clear preference for larger vehicles, filling the void left by the discontinued Model X and Model S. Priced from $61,990, the Y L targets affluent families and fleet buyers who’ve migrated to rivals like NVIDIA-powered Rivian R1S or the Ford Explorer EV. Unlike the China-only launch last August, the US rollout includes a ‘Launch Series’ with free Full-Self Driving (FSD) and 12 months of unlimited Supercharging — a potent incentive in an era of rising electricity costs. Crucially, the Y L arrives just as Tesla’s US inventory days dropped to 27 (from 22 in Q1), signaling tighter supply and pricing power. RBC Capital Markets reiterated its ‘Outperform’ rating with a $475 price target, citing the Y L’s potential to lift average selling prices and strengthen energy storage margins — a segment now contributing 40% gross margin versus 19% for vehicles.

Why Did Wall Street Sell Off Despite the Beat?

Tesla Deliveries beat expectations — but investors sold the news. The reason? Sustainability. Nearly 30,000 units came from inventory drawdown (production was just 451,758), including a ‘pull-forward’ of final Model S/X orders before April’s discontinuation. That one-time boost won’t repeat in Q3. More critically, the global EV market is intensifying: BYD overtook Tesla in Q2 BEV deliveries, and Apple’s rumored autonomous vehicle project continues to weigh on long-term auto-sector valuations. Truist analyst William Stein raised Tesla’s price target to $430 but held a ‘Hold’ rating, noting ‘no material updates on AI timelines or Cybercab regulatory progress.’ Meanwhile, Morgan Stanley cut its 2026 vehicle margin forecast to 18.2% from 20.5%, citing tariff headwinds and higher warranty costs. The stock’s 1.7 beta — nearly double the S&P 500’s — amplifies sensitivity to such margin whispers.

What’s Next for Tesla After the July 22 Earnings?

July 7 looms large: Tesla’s VP of Vehicle Engineering Lars Moravy teased ‘cool news’ from Gigafactory Texas — likely Cybercab production scale-up or regulatory clearance for driverless operation in Austin. That news could precede the July 22 earnings report, where vehicle margins, FSD subscription growth (now at 1.28 million users), and Megapack 3 deployment will dominate. With Tesla Deliveries now at record levels but US demand soft, the path forward hinges on execution: Can the Model Y L capture 15% of US three-row SUV sales by year-end? Can Cybercab’s $30,000 target price unlock mass robotaxi adoption? And can Tesla’s AI stack — trained on 6.2 billion real-world miles — finally monetize autonomy at scale? For now, the company’s $1.9 trillion valuation reflects not just car sales, but a bet on physical AI — one that investors will test rigorously in the weeks ahead.

Tesla’s competitive advantage is manufacturing.— Lars Moravy

Related Coverage: Tesla’s record Q2 delivery numbers are undeniable — but the real story lies in what’s missing from the report. Tesla Deliveries Hit 480,126 as Margin Warning Grows dives deep into the growing gap between volume momentum and profitability, quoting Tesla VP Lars Moravy’s blunt assessment: ‘Tesla’s competitive advantage is manufacturing.’ With vehicle margins under unprecedented scrutiny ahead of the July 22 earnings, this analysis separates the signal from the noise — and explains why Wall Street’s focus has shifted from units to unit economics.