Can Micron keep turning the memory squeeze into outsized profits as AI demand outruns global supply?

Why is Micron Memory Shortage mattering now?

Micron Technology, Inc. has become one of Wall Street’s clearest AI infrastructure beneficiaries because memory is now a bottleneck, not a commodity afterthought. The current Micron Memory Shortage narrative centers on HBM, the advanced memory used alongside AI accelerators from NVIDIA and other chip designers. Newer HBM generations require more wafer capacity per usable bit, which is intensifying supply pressure even as manufacturers expand output. That helps explain why investors continue to pay up for MU despite a sharp run and periodic pullbacks tied to rising bond yields and profit-taking across momentum names.

The broader memory market also remains constrained. Samsung, SK hynix, SanDisk, and Kioxia have all moved to raise pricing in recent quarters, reinforcing the view that contract pricing has not yet rolled over. Yahoo Finance reported Wednesday that Micron and SanDisk shares were also helped by the threat of an 18-day Samsung worker strike in South Korea, a development that could further tighten already stretched memory supply through 2026 and into 2027.

How strong is Micron’s operating momentum?

Micron’s latest reported numbers underscore why bulls remain constructive. In fiscal Q2 2026, the company posted record revenue of $23.9 billion, up 196% year over year, with diluted earnings per share of $12.07 and gross margin of 74.4%. Management also guided for another step higher in fiscal Q3, including projected revenue of about $33.5 billion at the midpoint and gross margin around 81%.

Those figures matter because they show the Micron Memory Shortage is translating into real financial leverage, not just thematic enthusiasm. When supply is sold out and customers still need more HBM and DRAM for AI servers, pricing and margins can expand quickly. Micron has said medium-term production capacity only covers roughly half to two-thirds of expected demand, highlighting how tight the market remains.

The company is trying to relieve that pressure through new capacity in Singapore, Idaho, New York, and Japan, but these projects take years to reach meaningful scale. For investors, that delay is crucial: it suggests favorable supply-demand conditions may persist longer than in a normal semiconductor upswing.

What are analysts and rivals signaling?

Analyst sentiment remains broadly upbeat even after MU’s extraordinary advance over the past year. Benzinga highlighted that Melius Research lifted its Micron price target to $1,100 on Tuesday, implying substantial upside from recent levels. TradingView also pointed to Micron and NVIDIA as standout profitability plays within the semiconductor group.

Competition is tight, but the market structure still favors the leaders. Samsung, SK hynix, and Micron dominate DRAM, while demand from hyperscalers and AI system builders such as Microsoft, Amazon, and Apple keeps advanced memory in high demand. Unlike hard-disk suppliers such as Seagate, Micron is directly exposed to the DRAM and HBM segments where shortages are most acute and margin expansion is strongest.

There are risks. Benzinga noted that higher long-term Treasury yields are pressuring richly valued chip stocks, including memory names. And memory has always been cyclical, so investors will need to watch for any future sign that DDR5 or HBM pricing starts flattening materially.

Can Micron keep outperforming?

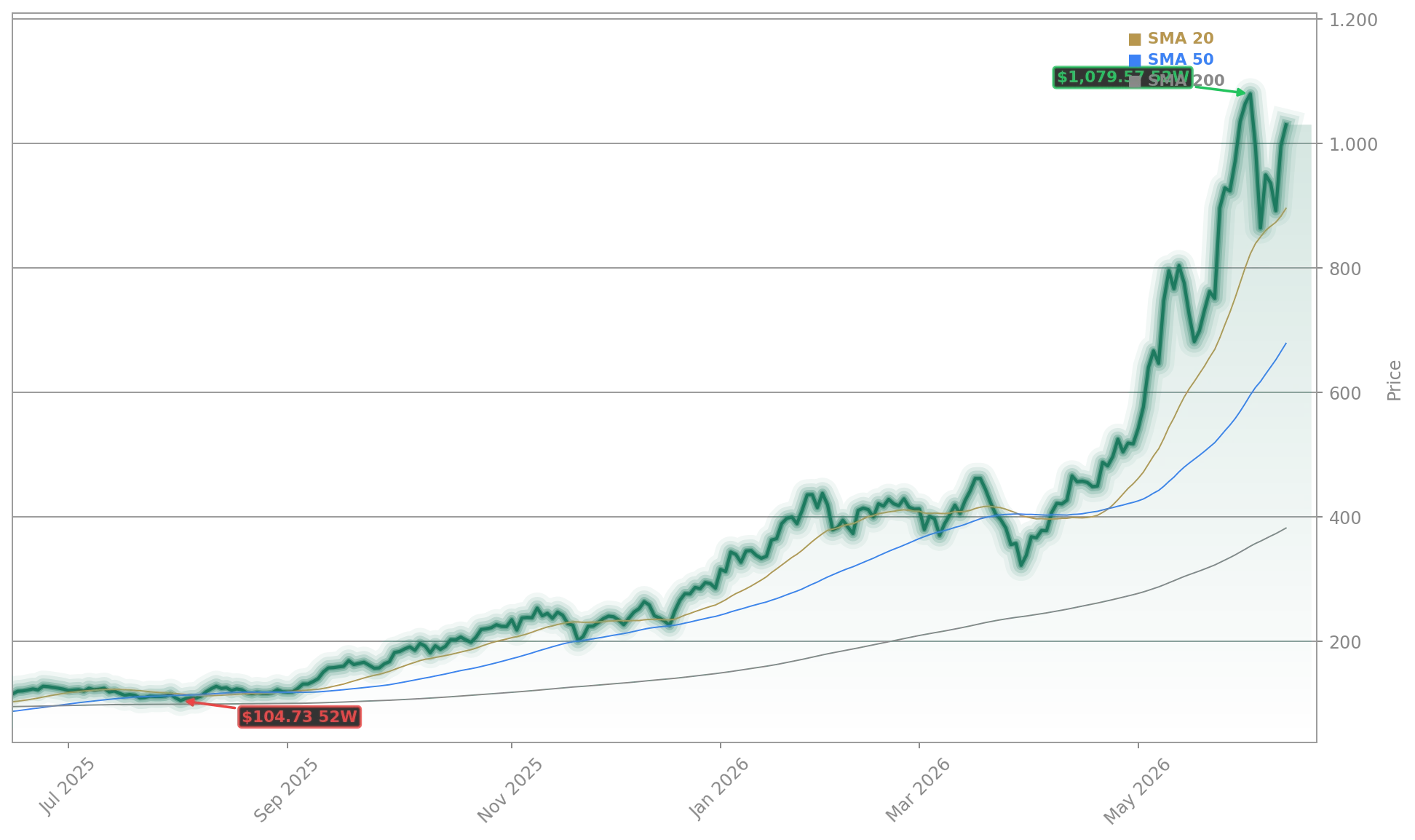

For now, the bull case still rests on execution and scarcity. MU’s intraday gain to $707.24 shows investors are willing to buy the stock again as AI demand stays intense and memory pricing remains firm. The company is not making a fresh high based on the current market data provided, but it is still trading near levels that reflect unusually strong confidence in the cycle.

Related Coverage: Investors tracking recent volatility may also want to read Micron AI Memory -3.6% Plunge: Is the AI Boom Overheating?, which looks at whether the stock’s rapid climb left it vulnerable to a sharper reset. That piece complements today’s setup by showing how quickly sentiment can swing in a momentum-driven AI trade, even when the fundamental memory backdrop remains supportive.

The bottom line is that the Micron Memory Shortage remains one of the most important themes in semiconductors. As long as AI server demand keeps outrunning new capacity, Micron looks positioned to sustain strong pricing, rising earnings, and continued investor attention. The next earnings report and any update on HBM supply will be key catalysts, but for now the Micron Memory Shortage still favors the bulls.