Can Micron’s $250 billion U.S. buildout outweigh fresh competitive pressure from SK Hynix and keep the AI memory trade intact?

What Does $250 Billion Mean for Micron Investment Expansion?

Micron Technology, Inc. has escalated its U.S. manufacturing commitment to $250 billion — a $50 billion increase over its prior $200 billion pledge — to meet surging demand for AI memory chips. The expansion includes five active fabrication facilities across New York, Idaho, and Virginia, with the New York megafab now pouring its first concrete ahead of schedule. CEO Sanjay Mehrotra framed the initiative as ‘American investment. American technology. American workers,’ targeting 40% domestic DRAM production and over 90,000 U.S. jobs. This Micron Investment Expansion isn’t just about scale — it’s a strategic hedge against geopolitical risk, supply chain fragmentation, and long-term hyperscaler dependency. The company also announced a $3 billion U.S. supply chain initiative, including a $500 million investment in GlobalWafers’ Texas wafer facility, reinforcing vertical integration.

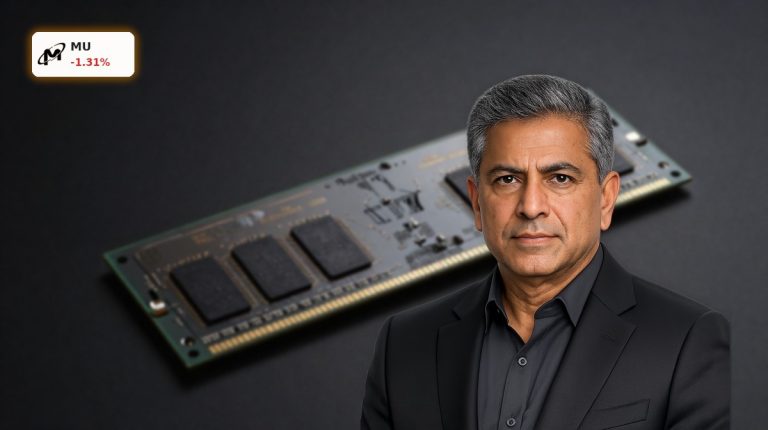

Why Is Micron Stock Pulling Back Amid Record Investment?

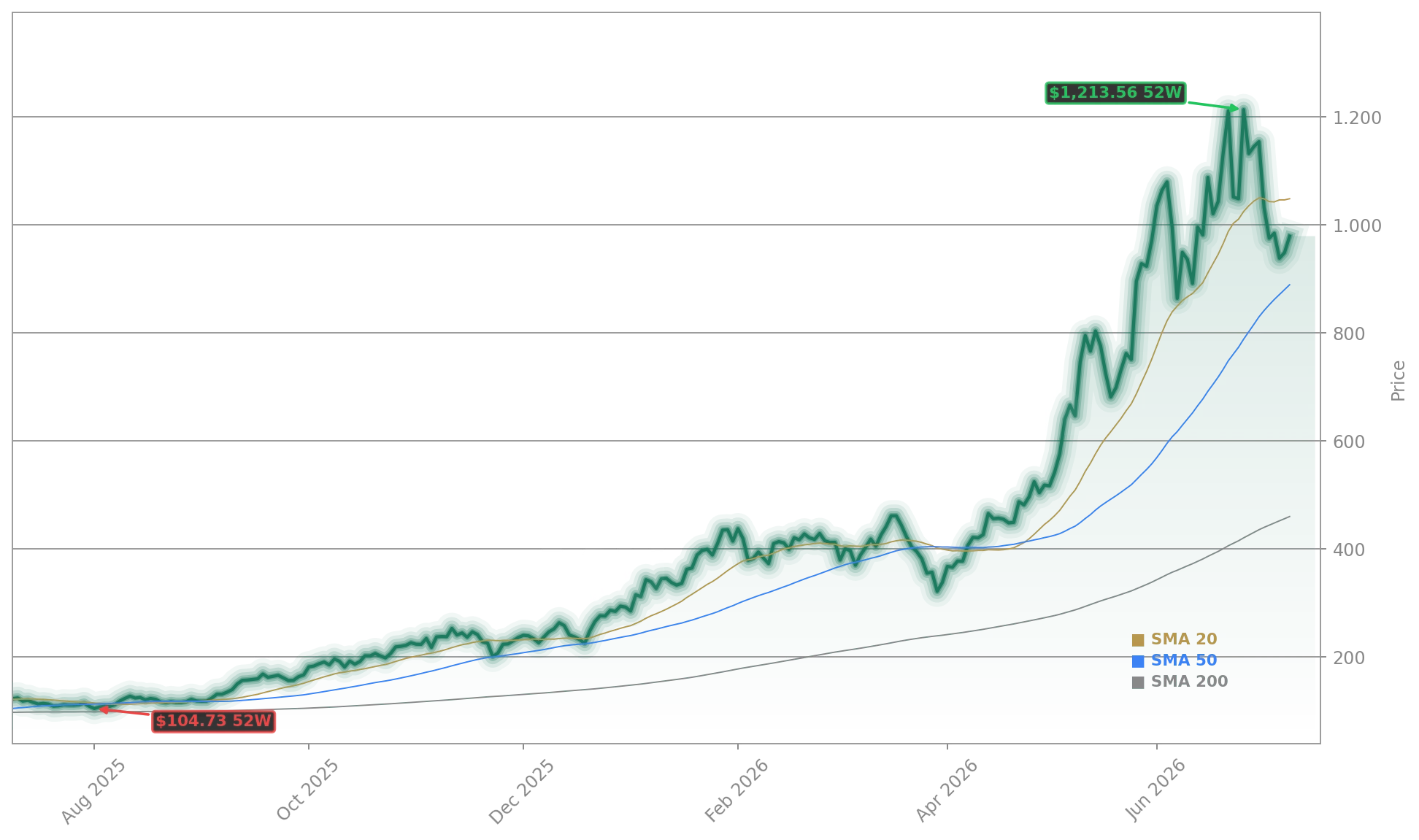

Despite robust fundamentals — fiscal Q3 2026 revenue of $41.46 billion (up 345.7% year over year), GAAP gross margin of 84.6%, and seven consecutive EPS beats — Micron Technology, Inc. shares declined 1.31% to $977.77 on Friday, July 10. The pullback reflects capital rotation, not deterioration: SK Hynix’s $26.5 billion Nasdaq debut created immediate liquidity pressure, with institutions reallocating positions to gain direct exposure to the HBM leader. Micron’s forward P/E remains at just 6.4 — dramatically below the Nasdaq-100 average of 25 — yet its valuation premium over SK Hynix (trading at ~6x forward earnings) is narrowing. As Barron’s analyst Adam Clark noted, SK Hynix offers ‘a cheaper way to play the memory-chip boom,’ triggering tactical profit-taking in MU after its 247.66% YTD surge.

How Does SK Hynix’s U.S. Listing Reshape the Memory Landscape?

SK Hynix now holds a commanding 56.4% share of the global HBM market — nearly triple Micron’s 21% — and supplies NVIDIA Corp. (NVDA) as its primary memory partner. Its Nasdaq listing under ticker SKHYV gives U.S. investors their first pure-play access to the dominant HBM supplier, ending Micron’s monopoly as the sole U.S.-listed memory manufacturer. This shift has already catalyzed ETF innovation: Direxion and Leverage Shares launched leveraged SKHYV ETFs within 24 hours of its debut. For Wall Street, the implication is clear — memory is no longer a single-stock trade. As portfolio manager Hendi Susanto of the Gabelli Global Technology Leaders ETF emphasized, ‘The main players have demonstrated discipline on capacity expansion… demand is still expected to outpace supply in 2027.’ Still, SK Hynix’s $26.5 billion capital raise could fund accelerated capacity, testing that discipline.

Where Do Competitors Like Samsung and Intel Fit In?

While SK Hynix and Micron dominate HBM, Samsung retains strong DRAM and NAND positioning — and surged in Seoul following Micron’s $250 billion announcement. Intel, meanwhile, faces stark contrast: its Q2 2026 forecast shows a projected 4% revenue decline, highlighting divergent trajectories across the semiconductor sector. Unlike Micron’s AI memory tailwinds, Intel’s foundry and client CPU businesses remain under pressure. RBC Capital Markets recently downgraded Intel to ‘Underperform,’ citing ‘persistent execution risk and margin compression.’ Meanwhile, Citigroup raised its price target on Micron Technology, Inc. to $1,486, citing ‘unmatched strategic customer agreements with AI hyperscalers and pricing discipline locked in through 2028.’ That target implies 52% upside from current levels — a stark signal to investors weighing AI infrastructure exposure against broader tech volatility.

Is Micron Investment Expansion a Hedge Against the Memory Cycle?

This is American investment. American technology. American workers.— Sanjay Mehrotra, CEO of Micron Technology, Inc.

Historically cyclical, the memory industry is undergoing structural change: multi-year Strategic Customer Agreements now lock in pricing bands and volume commitments — a direct result of AI’s insatiable bandwidth demands. Micron’s contracts with Microsoft, Meta, and Ford ensure revenue visibility through 2028, insulating it from traditional supply-demand swings. Analysts at Morgan Stanley note that ‘Micron’s U.S. fab buildout isn’t just capacity — it’s geopolitical optionality.’ With U.S. AI infrastructure spending projected to exceed $1.5 trillion in 2027, and memory expected to capture 35–40% of that spend (per Bank of America), this Micron Investment Expansion positions the company not just as a supplier — but as critical national infrastructure. That’s why the stock remains a core holding in AI-focused ETFs like the VanEck Semiconductor ETF (SMH), where Micron accounts for 9.39% of assets.