Can Micron Investment turn today’s AI memory surge into a lasting valuation reset for one of America’s most strategic chipmakers?

What Does $250 Billion in Micron Investment Mean for Wall Street?

Thursday’s announcement — confirmed by Reuters and Yahoo Finance — marks the largest single corporate commitment to U.S. semiconductor manufacturing in history. The $250 billion figure dwarfs Intel’s and TSMC’s combined U.S. plans and signals a structural shift: Micron Technology, Inc. is no longer reacting to AI demand — it’s engineering the supply chain to sustain it. The investment includes $3 billion specifically earmarked to fortify the domestic semiconductor ecosystem, including a $500 million strategic financing package for GlobalWafers’ 300mm silicon wafer facility in Sherman, Texas. A 10-year supply agreement locks in long-term raw material access — a critical hedge against geopolitical risk and a key differentiator versus Korean peers. For investors, this isn’t just capex — it’s a de-risking of margin sustainability and a vote of confidence in U.S.-based tech leadership.

How Does Micron Investment Compare to SK Hynix and Samsung?

While SK Hynix prepares for its Nasdaq debut — offering U.S. investors direct exposure to Nvidia’s top memory supplier — Futurum Equities’ Shay Boloor and CEO Daniel Newman both favor Micron Technology, Inc. for distinct reasons: domestic supply chain security and lower tariff risk. Newman explicitly cited Micron’s ‘shock risk’ as the lowest among memory leaders. That advantage is now quantified: Micron’s $250 billion Micron Investment dwarfs SK Hynix’s U.S. listing proceeds and reinforces its ability to meet U.S. data center and defense requirements without cross-border friction. Samsung, meanwhile, faces scrutiny after its mixed earnings — a contrast that helped trigger a broader memory selloff last week, detailed in Micron Samsung Selloff -8.3% After Samsung Earnings Shock.

Is Micron Investment Driving Record Margins and Valuation Shifts?

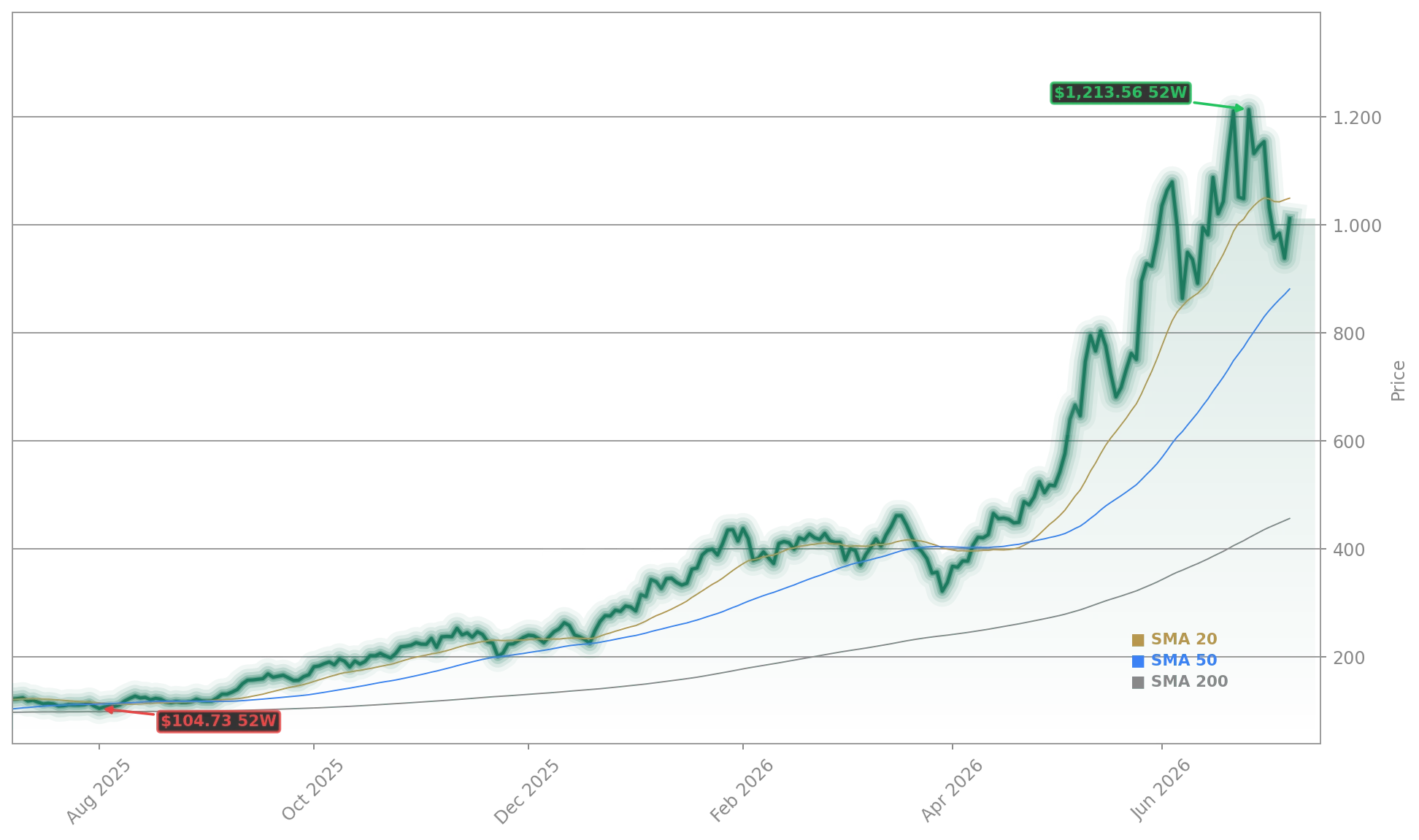

Absolutely. Gross margins hit 85% in fiscal Q3 — unprecedented for a memory company — driven by pricing power across cloud, data center, and mobile segments. Revenue surged 346% year-over-year to $41.5 billion, while net income jumped 205% to $28.2 billion. Bank of America Global Research reaffirmed its Buy rating and raised its price target to $1,550, citing a sum-of-the-parts valuation that assigns Micron’s high-bandwidth memory (HBM) business a 31x P/E multiple — reflecting its strategic, non-cyclical role in AI infrastructure. Cantor Fitzgerald lifted its target to $2,000, while Bernstein set $1,300. With forward P/E at just 6.5x and a PEG ratio of 0.14, Micron Investment isn’t a cost center — it’s the engine behind a valuation re-rating.

What’s Next for Micron Investment and the AI Memory Supercycle?

We believe the market is underestimating the transition toward longer-duration agreements and more predictable pricing. As memory evolves from a cyclical commodity to a strategic AI enabler, multiples should expand.— Vivek Arya, BofA Global Research

Management expects tight HBM supply conditions to persist ‘beyond calendar 2027’ — a timeline reinforced by analyst consensus projecting 81% revenue growth in fiscal 2027. The company has presold its full HBM production capacity through 2027 and is locking in 50% of total revenue via three- to five-year strategic customer agreements. This transforms Micron from a commodity play into a contracted AI enabler — a shift Wall Street is pricing in. The Russell 1000 Growth Index recently added Micron at a near-400-basis-point weighting, reflecting its new status as a core AI infrastructure holding. With $250 billion in Micron Investment now committed, the question isn’t whether the supercycle ends — it’s how long the U.S. manufacturing ramp can sustain it.