Can Micron Record momentum keep defying memory-cycle gravity as AI demand rewrites the valuation story?

Why Is Micron Record Driving Wall Street?

Micron Technology, Inc. became one of the market’s biggest stories this week after a sharp revaluation tied to artificial intelligence infrastructure spending. UBS analyst Timothy Arcuri raised his price target on Micron from $535 to $1,625, the highest target among the firms covering the stock. That call helped propel MU into the trillion-dollar valuation club and reinforced the idea that memory is no longer just a cyclical side story in AI buildouts.

The core of the bullish case is changing contract structure. Arcuri argues that newer multiyear agreements include fixed volumes, longer duration, and partially fixed pricing, giving Micron more visibility than memory companies historically enjoyed. That matters because investors have long discounted memory names for boom-and-bust swings. If earnings become more durable, valuation multiples could expand closer to companies like NVIDIA.

How Strong Is Micron Technology Momentum?

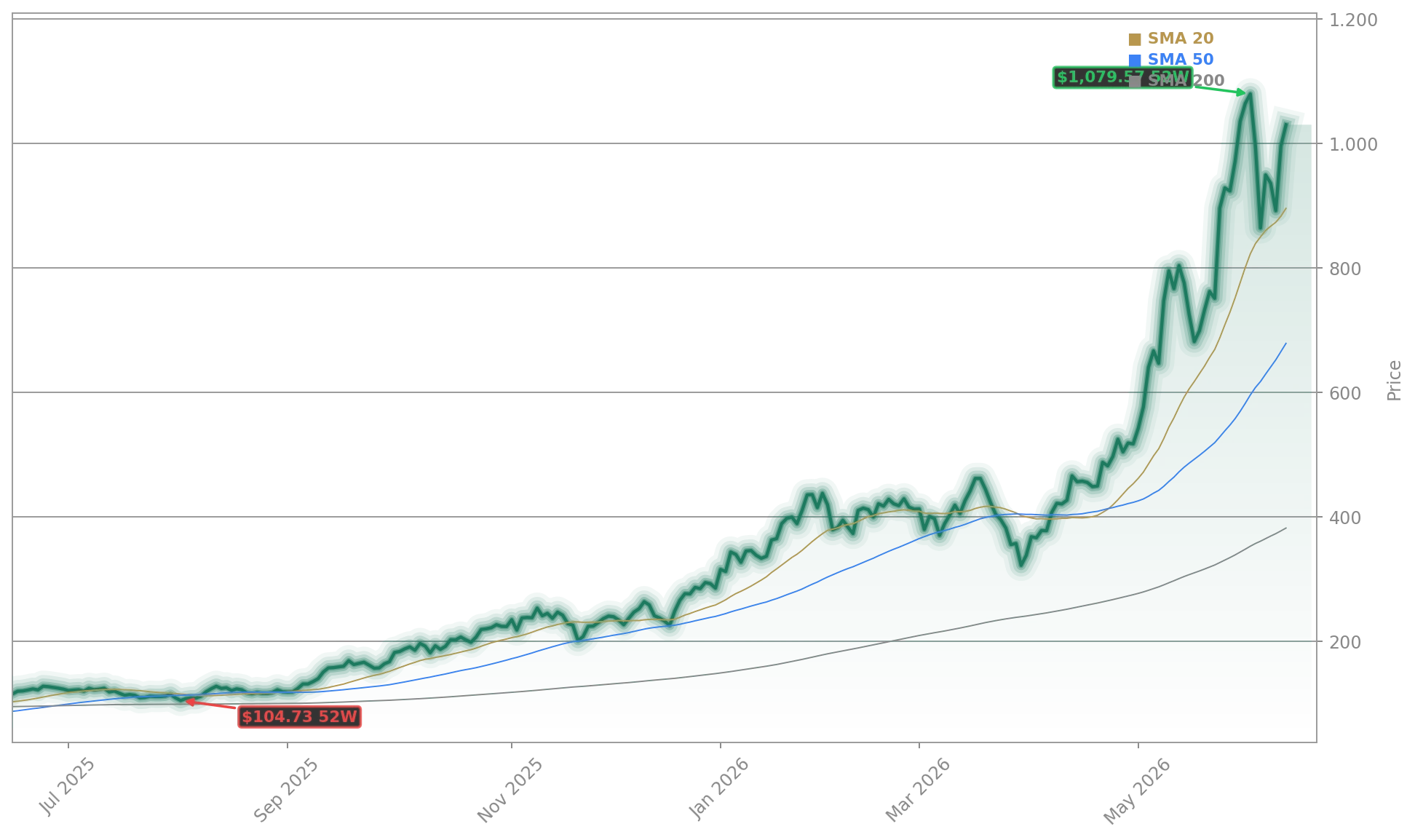

The stock move has been extraordinary even by semiconductor standards. MU is now up sharply year to date and has multiplied over the last 12 months, fueled by high-bandwidth memory demand and broader DRAM tightness. Management has already said its 2026 HBM output is sold out, a sign that hyperscaler demand remains intense as AI data centers expand.

Micron’s recent operating performance helps explain the enthusiasm. Fiscal second-quarter revenue nearly tripled from a year earlier to $23.86 billion, and the company guided for roughly $33.5 billion in fiscal third-quarter revenue. That number alone exceeds what Micron used to generate in some full fiscal years. The company also raised its dividend by 30%, underscoring management confidence in cash generation.

Other banks have also turned more constructive. Citigroup recently raised its target, while broader Wall Street coverage remains heavily tilted toward Buy ratings. Even so, the average target still trails the current share price, showing how fast the Micron Record rally has outrun consensus models.

Can Micron Technology Sustain This AI Premium?

The debate now is whether Micron deserves to trade more like an AI infrastructure enabler than a classic commodity chip stock. Bulls point to a global supply bottleneck in HBM, where Micron competes with Samsung and SK Hynix. Analysts increasingly expect shortages to persist into 2027, which could preserve unusual pricing power for the industry’s top producers. That supply backdrop is also benefiting related names such as Apple suppliers, equipment makers, and data-center chip leaders.

The rally has spilled into the broader semiconductor complex. Semiconductor equipment companies and AI-adjacent chipmakers have moved higher as investors bet Micron’s pricing signal reflects stronger capital spending across the ecosystem, including from customers and partners tied to Tesla-style compute ambitions and hyperscale cloud demand. In that sense, the Micron Record move is being treated as a read-through for the entire AI hardware stack.

Still, risks remain. Memory has a long history of oversupply cycles, and some strategists warn that capacity additions could eventually catch up with demand. UBS itself outlined a bearish scenario where a slowdown in HBM demand could send the shares sharply lower. Investors chasing vertical moves in memory stocks should keep that cyclicality in view.

What Comes Next For Micron Technology?

Near term, traders will watch whether MU can hold its pre-market gains and build support closer to the $1,000 level. Just as important will be follow-through from peers like Samsung and SK Hynix, plus further commentary from customers in AI servers and cloud infrastructure. If long-term contracts continue to reshape earnings visibility, Micron’s valuation framework may keep changing.

Related Coverage: For investors looking deeper into the AI memory thesis, our earlier report Micron Forecast +13.2%: UBS Sees Bigger AI Memory Upside examined whether premium multiples for Micron can hold as supply tightens and estimates rise. That piece also explored why the market is starting to treat Micron less like an old-cycle DRAM name and more like a strategic AI bottleneck.

The market will start to put a more normal multiple on the stock and MU will continue to rerate higher.— Timothy Arcuri

The Micron Record story now sits at the center of the AI hardware trade. For investors, the key question is whether tighter supply, stronger contracts, and rising earnings can support this new valuation regime; the next earnings updates and HBM market signals will determine whether Micron can extend its Micron Record run.