Can Micron AI Memory justify Wall Street’s soaring targets, or is the market racing ahead of reality?

Why is Micron AI Memory driving Wall Street now?

The latest move in Micron AI Memory reflects more than momentum. Wall Street is increasingly treating memory as a critical layer of AI infrastructure, not just a cyclical commodity segment. That shift has helped push Micron close to a $1 trillion market capitalization after a dramatic run in 2026, making it one of the strongest performers in the S&P 500 this year.

Several firms have turned more constructive. UBS lifted its price target to above $1,600, while DA Davidson raised its target to $1,500. Mizuho Securities also increased its Micron target to $1,150 from $800 and kept an Outperform rating, arguing that agentic AI will require far more DRAM and high-bandwidth memory over the next several years. That matters because next-generation AI servers tied to NVIDIA platforms are expected to carry more memory content per system, expanding Micron’s opportunity well beyond a standard PC or smartphone cycle.

Can Micron hold its edge against rivals?

Micron still trails Asian competitors in one crucial segment. Counterpoint Research estimated that in the fourth quarter of 2025, SK Hynix controlled about 57% of the global HBM market, compared with 22% for Samsung and 21% for Micron. Even so, Micron’s share is large enough to keep it central to the AI buildout, especially as hyperscalers and enterprise customers diversify supply chains.

That helps explain why investors are looking past old semiconductor playbooks. Long-term supply agreements with financial commitments are improving visibility, even if the industry remains cyclical. Some portfolio managers still warn that semiconductors do not stop being cyclical just because AI demand is strong. But the market is clearly rewarding the companies with the best leverage to AI memory pricing, packaging, and volume growth.

The company’s strategic relevance also extends beyond hardware sales. Micron participated in a recent funding round for Anthropic, reinforcing the increasingly tight links among AI model developers, chipmakers, and cloud platforms. That broader positioning matters for investors comparing Micron with names such as Apple, Tesla, and NVIDIA, where ecosystem control increasingly shapes long-term multiples.

Is valuation becoming the biggest risk?

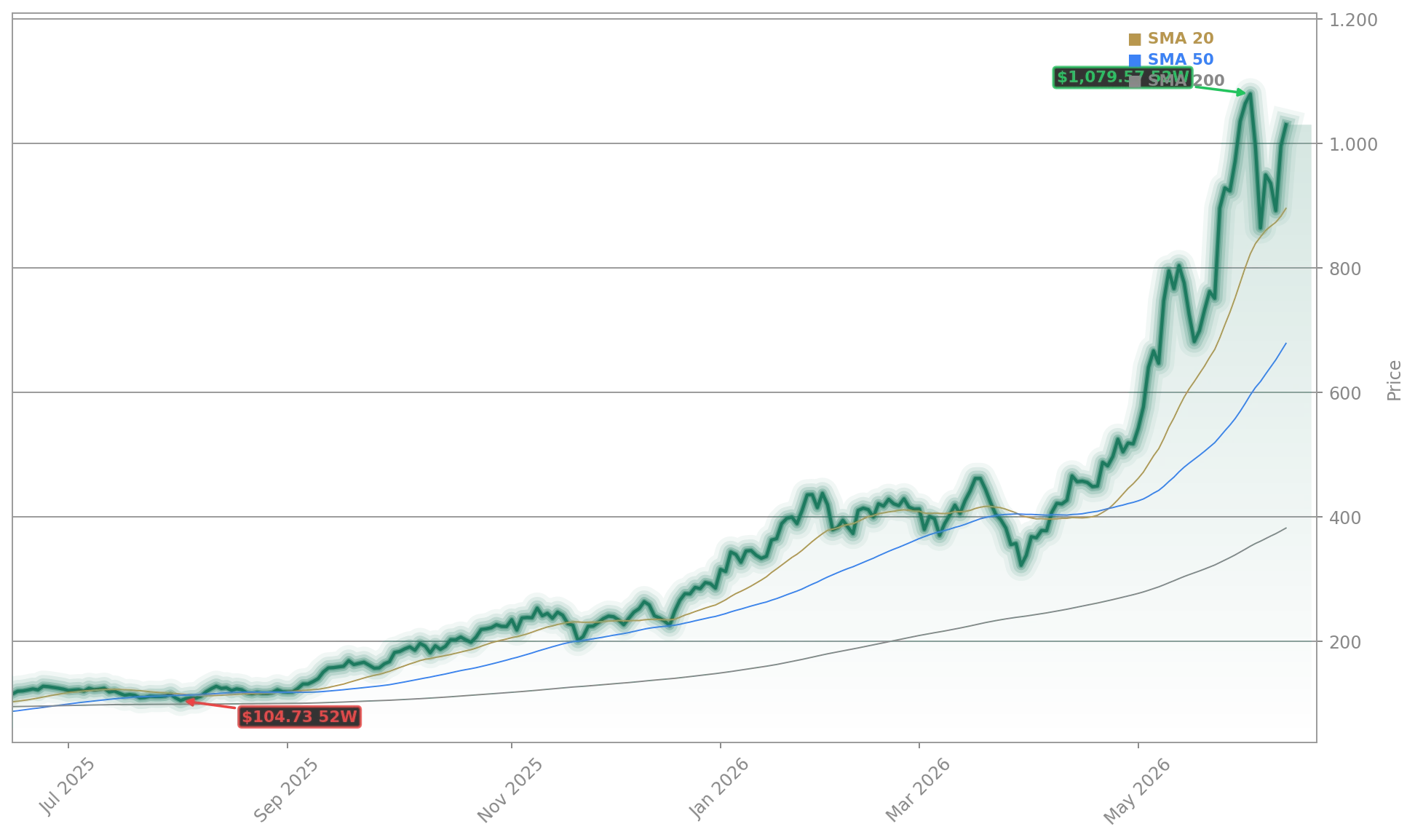

The bullish case is powerful, but valuation is getting harder to ignore. Yahoo Finance Singapore highlighted that Micron’s market value has moved beyond $1 trillion on surging HBM demand, while one fair-value framework sits far below the current share price. TipRanks also noted that Blackstone increased its stake, even as technical conditions look overbought after a gain of more than 200% year to date.

That tension defines the setup. On one side, Micron trades at a relatively modest earnings multiple near 10, suggesting that earnings power could still be underestimated if AI memory demand holds. On the other, the chart has become steep enough that even bullish traders are watching for climactic behavior, especially after record options activity and repeated gap-like advances.

Options dynamics are adding fuel. As Micron approaches the psychologically important $1,000 level, delta hedging tied to call positions can amplify upside moves. That kind of gamma-driven support has become part of the near-term bull thesis, though it can work in reverse if momentum fades.

What should investors watch next at Micron?

The next key question is whether demand remains broad enough to justify even higher estimates. Mizuho sees strong DRAM and HBM expansion through 2027, while Barchart recently argued that the AI semiconductor trade remains attractive through diversified exposure to names like Micron, AMD, and NVIDIA. TradingView also highlighted Micron as a standout AI-related memory winner, underscoring how firmly it has entered the elite group of US market leaders.

Related Coverage: Investors following this breakout may also want to read Micron Record: AI Memory Boom Reshapes the Valuation Case. That analysis digs deeper into whether the company’s AI memory story can finally soften the boom-and-bust pattern that has historically defined the memory industry, and it adds useful context for judging how sustainable today’s premium really is.

Micron AI Memory remains one of the market’s most important AI infrastructure trades. If HBM demand, contract visibility, and analyst support continue to build, the path toward $1,000 stays in play, and the next earnings cycle could determine whether Micron deserves an even larger role in growth-oriented portfolios.

Fazit folgt.