Is Alphabet’s massive AI funding move a masterstroke for long-term dominance, or an expensive signal that the AI arms race is getting riskier?

What Does Alphabet AI Financing Mean for Investors?

Alphabet Inc. (Google) has executed one of the largest equity financings in tech history — $85 billion raised via a dual-track offering: 80% in common stock and 20% in mandatory convertible preferred shares. The preferred tranches, trading as GOOGM and GOOGN, deliver an immediate yield exceeding 6% — a rare premium in the S&P 500’s mega-cap cohort. Unlike traditional preferred stock, these are structured with asymmetric conversion caps: for Class A, conversion into 0.1126–0.1408 shares of GOOG, tied to a $355–$444 price band. That means upside participation is capped — and downside protection is limited. For U.S. income-seeking portfolios, this isn’t a long-term yield play, but a tactical three-year bridge to 2029, when full conversion occurs.

How Does This Compare to Meta and NVIDIA?

While Meta just launched AI Mode — a direct challenge to Google Search backed by Muse Spark and projected to generate $10 billion annually (per Morgan Stanley analyst Brian Nowak) — Alphabet’s $85 billion Alphabet AI Financing signals a different strategic priority: infrastructure dominance. NVIDIA’s Blackwell platform powers much of this stack, and Alphabet’s capital is flowing into custom AI chips, liquid-cooled data centers, and Project Nimbus expansion. Crucially, Meta’s AI monetization remains nascent and unproven at scale, whereas Alphabet’s ad-tech moat and cloud revenue ($9.2 billion in Q1 2026, up 24% YoY) provide immediate cash flow to absorb AI CapEx. Meanwhile, Citigroup recently raised Alphabet’s price target to $425, citing ‘AI monetization inflection in Search Generative Experience and Vertex AI enterprise adoption.’

Why Are Wall Street Analysts Bullish Despite Caution?

Not all voices are celebratory: Michael Burry’s June 15 warning that ‘it has been ridiculous for a very very long time’ echoes concerns about AI valuations — a sentiment shared by Ray Dalio and Steve Eisman. Yet Wall Street’s consensus remains constructive. RBC Capital Markets upgraded Alphabet to ‘Outperform’ last week, citing ‘accelerated AI spend translating to higher cloud gross margins and improved search ARPU.’ The $85 billion Alphabet AI Financing isn’t just about funding — it’s a signal of commitment. Alphabet’s Q1 2026 operating margin held at 31.2%, outperforming S&P 500 tech peers on margin resilience. That discipline helps justify the capital raise as strategic, not defensive. Importantly, the convertible preferred structure avoids dilution pressure on common shares until 2029 — a key differentiator versus peers like Apple (AAPL), which relies on debt for buybacks.

What’s the Risk for U.S. Portfolio Managers?

The shares are mandatory convertible — all shareholders will see shares convert to their corresponding common stock on May 15, 2029. That 6% yield will only last for the next three years.— Alphabet Inc. (Google) Investor Relations

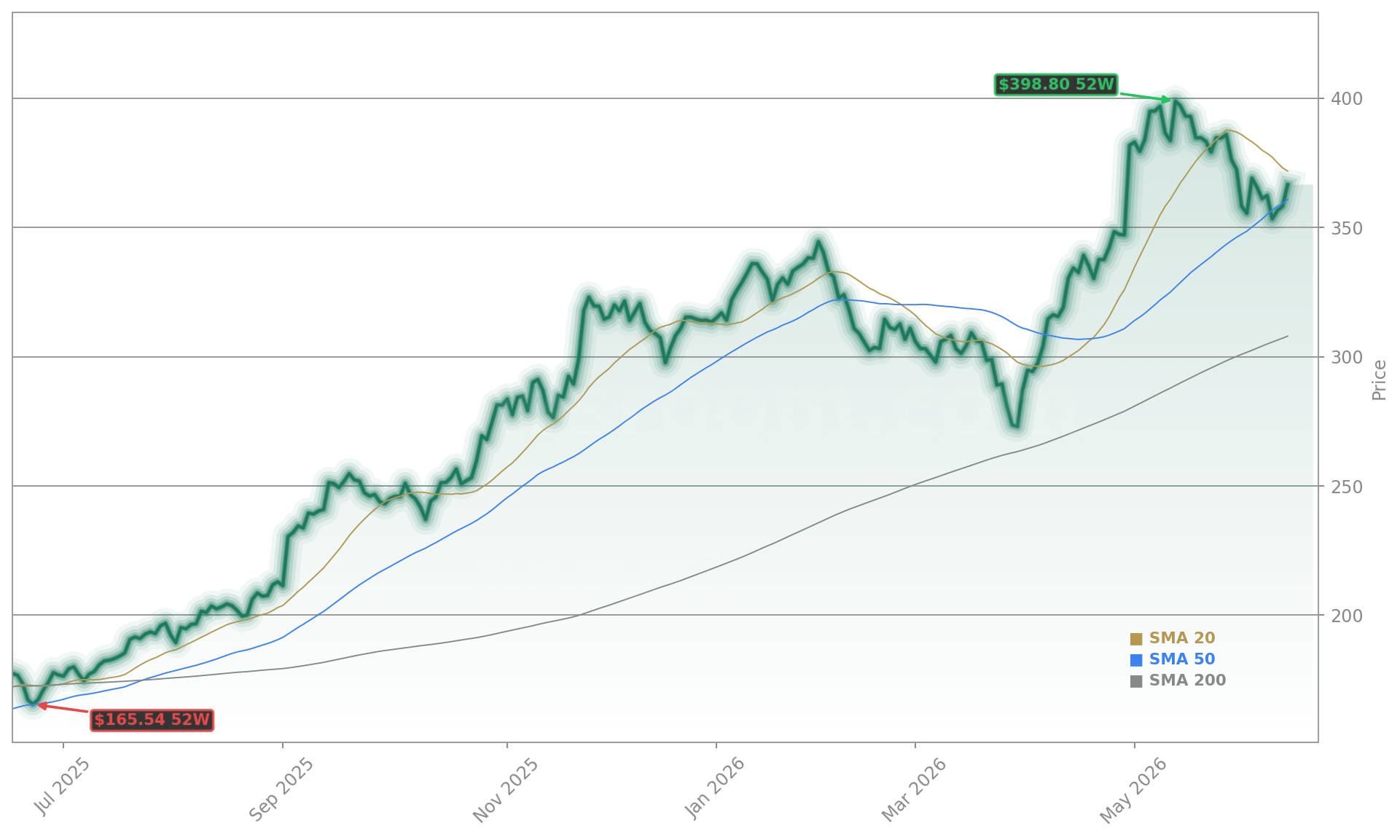

U.S. investors must weigh the 6% yield against three structural constraints: (1) the 2029 mandatory conversion deadline, (2) capped upside participation below $444, and (3) exposure to downside if GOOG falls below $355 — a level just $8 above today’s $367.11 close. The NASDAQ Composite is up 18% YTD, and Alphabet’s rally has outpaced the S&P 500 by 700 basis points — raising valuation sensitivity. Oppenheimer analyst Ed Yang, covering semiconductor enablers, noted that ‘Alphabet’s AI financing reflects the new capital intensity of AI — a trend benefiting Lam Research (LRCX) and Micron (MU) more directly than end-market players.’ That’s a reminder: Alphabet AI Financing may matter more for chip suppliers than for Alphabet’s own earnings in the near term.