Can Eli Lilly’s explosive GLP-1 demand and raised outlook really justify one of the richest valuations in global pharma?

How big was the Eli Lilly earnings beat?

Eli Lilly and Company turned in Q1 2026 numbers that far exceeded what Wall Street had penciled in. Analysts had expected adjusted EPS around $6.66 to $6.97 and revenue near $17.6–$17.8 billion. Instead, the company reported non‑GAAP EPS of $8.55, up 156% year over year from $3.34, and revenue of $19.8 billion, a 56% jump versus the prior year.

On a reported basis, EPS climbed 170% to $8.26, with net income more than doubling to $7.4 billion. Volume growth of about 65% more than offset a roughly 13% decline from lower realized prices, underscoring how explosive demand for GLP‑1 therapies remains even as the company cuts prices in some markets.

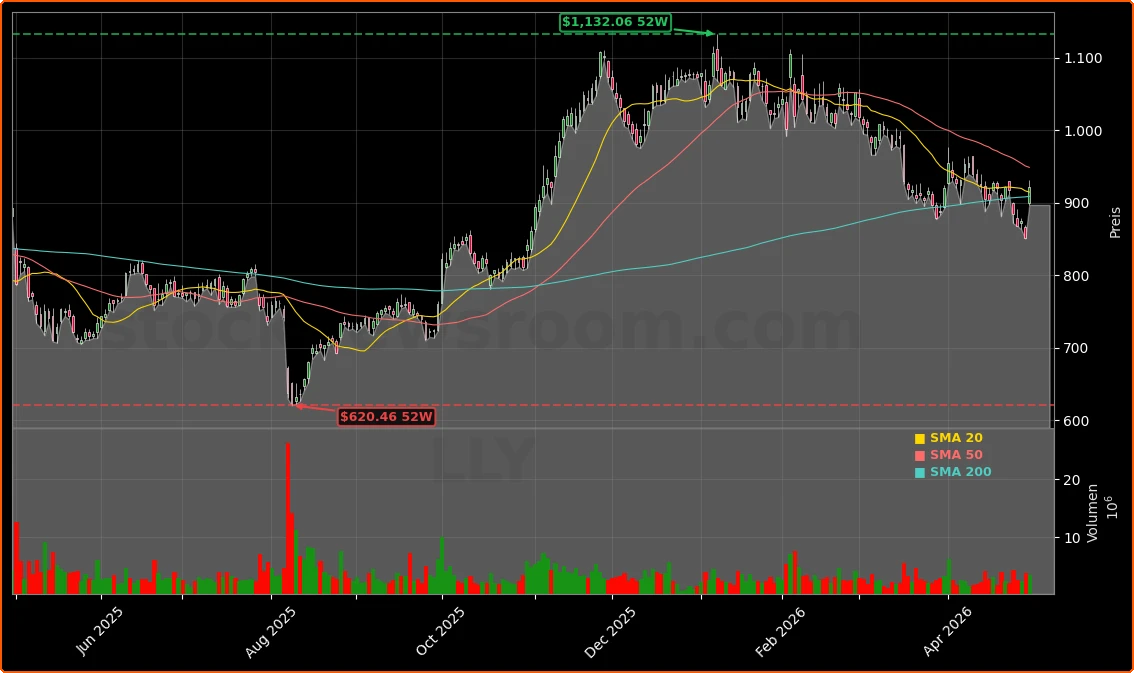

The stock reaction has been emphatic. With shares at $921.61, up 8.27% versus the previous close of $855.49, Eli Lilly is recovering from a pullback that had left the name well below its 52‑week high near EUR 970 on European venues. For S&P 500 and healthcare investors, the latest Eli Lilly Earnings report reaffirms the stock’s role as a key growth driver in large‑cap pharma portfolios.

What drove the surge at Eli Lilly and Company?

The quarter was all about tirzepatide. Diabetes shot Mounjaro generated $8.66 billion in sales, up 125% year over year and ahead of consensus estimates near $7.3 billion. Weight‑loss injection Zepbound added another $4.16 billion, up about 80% from last year and slightly above market expectations around $4.0 billion. Combined, tirzepatide‑based products delivered roughly $12.8 billion in quarterly revenue, more than many entire Big Pharma franchises.

U.S. revenue rose 43% to $12.1 billion, fueled by higher GLP‑1 prescription volumes even as prices declined, while revenue outside the U.S. jumped 81% to $7.7 billion. International demand for Mounjaro more than tripled, with management highlighting strong uptake across Europe, China, Brazil and other populous markets where many patients pay out of pocket.

Margins remained robust despite pricing pressure. Non‑GAAP gross margin increased 54% to $16.4 billion, or 82.6% of revenue, only modestly lower as a percentage of sales than a year ago. Research and development spending climbed 28% to $3.5 billion, reflecting an unusually broad late‑stage pipeline, including next‑generation obesity candidate retatrutide and multiple oncology and immunology assets.

How did guidance change after Eli Lilly earnings?

The scale of the beat gave management room to raise the bar for 2026. Full‑year revenue guidance was lifted by $2 billion to a new range of $82–$85 billion, from $80–$83 billion previously. Non‑GAAP EPS is now expected between $35.50 and $37.00, up from $33.50–$35.00. At the midpoints, that represents an incremental $2 per share of earnings and a clear signal that momentum is expected to persist.

Credit markets are taking notice as well. S&P Global Ratings upgraded Eli Lilly’s issuer rating to AA‑ with a positive outlook, citing expectations that revenue could top $100 billion by 2028 and leverage fall below 1x, even as the company executes an increasingly aggressive M&A strategy in oncology, neuroscience and immunology. RBC Capital Markets, which already rates the stock “outperform” with a $1,250 price target, described the quarter as a “blowout” and argued that international Mounjaro sales alone could make the company’s updated guidance look conservative.

For diversified U.S. investors, this latest Eli Lilly Earnings update effectively de‑risks near‑term growth assumptions and helps justify the premium valuation relative to peers like Novo Nordisk and broader healthcare names in the S&P 500.

Where does Foundayo and the pipeline fit in?

Beyond the headline Q1 numbers, the story is increasingly about what comes next in GLP‑1s. Oral obesity pill Foundayo, recently approved by the U.S. Food and Drug Administration, did not contribute to first‑quarter revenue because its launch began in the second quarter. Management indicated early prescription trends are encouraging, with roughly 20,000 prescriptions in the first 20 days and more than 80% of users new to the GLP‑1 class.

CEO Dave Ricks emphasized that building Foundayo will be a multi‑quarter branding and education effort, not an overnight spike, but stressed that a convenient once‑daily pill without food or water restrictions should expand the addressable market beyond injectable‑tolerant patients. That positioning is critical as Eli Lilly faces competition from Novo Nordisk’s oral Wegovy pill, which enjoyed a roughly three‑month head start. TIME recently highlighted Novo Nordisk in its list of the most influential companies for its obesity work, underscoring how central this therapeutic area has become for global healthcare.

At the same time, Eli Lilly is reinforcing its long‑term growth profile with dealmaking. The planned $7.8 billion acquisition of Centessa Pharmaceuticals will broaden its neuroscience pipeline, while agreements to buy Orna Therapeutics, Kelonia Therapeutics and Ajax Therapeutics deepen oncology and genetic medicine capabilities. For investors, these transactions are designed to ensure the GLP‑1 cash engine today seeds diversified revenue streams once current obesity and diabetes products eventually face tougher competition and patent expirations.

How should investors view Eli Lilly versus other U.S. growth leaders?

On a day when mega‑cap tech names such as Apple, NVIDIA and Tesla often dominate headlines, the latest Eli Lilly Earnings print shows that biopharma can still deliver tech‑like growth at scale. With shares now rebounding and up sharply intraday, Eli Lilly is again behaving like a core secular growth holding rather than a defensive healthcare play.

For U.S. and global investors benchmarking against the S&P 500 or NASDAQ, the key question is whether today’s valuation fully discounts long‑term GLP‑1 penetration and the company’s ambitious pipeline. Analysts at Evercore ISI and Cantor Fitzgerald note that current guidance may still understate international tirzepatide uptake, while S&P’s base case sees free cash flow compounding fast enough to support both aggressive capital returns and continued deal flow.

That mix of strong current fundamentals, a visible multi‑year runway in obesity and diabetes, and active portfolio expansion leaves Eli Lilly positioned as one of the few large‑cap healthcare names that can plausibly compete with leading tech stocks for growth exposure in diversified portfolios.

Related Coverage

For a deeper look at how M&A fits into the broader strategy, investors can read Eli Lilly Acquisition Boom: $2.3B Ajax Oncology Shock, which explores whether the Ajax Therapeutics deal marks a smart oncology pivot or an expensive side bet. Taken together with today’s results, that analysis helps frame how the company is using its GLP‑1 windfall to build a more diversified, oncology‑heavy future.

“What we’re seeing now is basically organic demand, which is pretty strong to us,” Eli Lilly CEO Dave Ricks said about the early launch of the Foundayo obesity pill.— Dave Ricks, CEO of Eli Lilly and Company

In summary, the latest Eli Lilly Earnings confirm that the GLP‑1 wave is still building, not cresting, for this Indianapolis heavyweight. For investors, the combination of outsized growth, stronger guidance and an expanding obesity and neuroscience pipeline keeps Eli Lilly and Company squarely on the radar as a long‑term compounder. The next few quarters of Foundayo adoption and international GLP‑1 launches will show just how far this leadership position can extend.