Can FuelCell Energy’s $225 million raise fund real growth, or did the market just price in a much tougher road ahead?

What Does the FuelCell Energy Offering Mean for S&P 500 Clean Energy Exposure?

The FuelCell Energy Offering is not just a financing event — it’s a market-wide litmus test for investor appetite in pre-profitability clean infrastructure names. At $225 million, the raise is the largest for any U.S.-listed fuel cell company this quarter and represents a 50% increase over the original $150 million target. Underwritten by Citigroup and Barclays, the offering is earmarked for manufacturing capacity expansion and working capital — critical enablers for fulfilling the 380-megawatt pipeline with Fit Energy and scaling Siemens-integrated projects. Yet its timing — just days after Q2 FY2026 results revealed $35.59 million in revenue (down 5% YoY) and a $42.57 million non-cash impairment — has sharpened scrutiny. For S&P 500-focused energy ETFs and NASDAQ-focused clean tech funds, FCEL’s post-offering price action is now a key volatility proxy alongside Bloom Energy and Plug Power.

How Does the Siemens Partnership Change the Competitive Landscape?

Siemens Corporation’s memorandum of understanding with FuelCell Energy marks a strategic inflection: it shifts the company from a standalone stack supplier to a systems-integrated solutions partner. Siemens will design and supply electrical balance-of-plant (EBOP) systems — a critical bottleneck in rapid data center deployment. This directly competes with integrated offerings from NVIDIA-aligned power infrastructure providers and positions FuelCell Energy to bid on hyperscaler microgrid tenders where speed-to-power matters more than lowest cost per watt. Unlike Bloom Energy’s Oracle deal — delivered in 55 days — FuelCell Energy’s Siemens-backed approach targets >100 MW commercial deployments with repeatable engineering. Still, analysts at RBC Capital Markets caution that ‘integration execution remains unproven at scale,’ citing delays in prior U.S. utility projects.

Why Did the FuelCell Energy Offering Trigger a Sector-Wide Pullback?

FuelCell Energy’s 11% intraday drop — leading a broad fuel cell selloff that dragged Bloom Energy down 8% and Plug Power down 6% — reflects more than dilution. It signals recalibration of the AI power thesis. With the HYDR ETF holding 29% of its net assets in FCEL, BE, and PLUG, Friday’s move exposed concentration risk. The $21.00 offering price — set 19% below Tuesday’s $25.96 close — became an immediate psychological and technical threshold. When shares breached $21.00 midweek, momentum traders exited en masse, pushing FCEL 13% lower into Wednesday’s close. That break coincided with RSI dropping to 49.50 — a neutral reading confirming loss of upward thrust. For Wall Street portfolios, the FuelCell Energy Offering has become a stress test for AI infrastructure valuations amid rising interest rate uncertainty.

Is the Data Center Pipeline Enough to Offset Dilution Risk?

The Fit Energy agreement — for up to 380 MW across four phases — remains FCEL’s strongest near-term catalyst. But only the first 30 MW phase is contractually committed, with deliveries due by year-end. The remaining 350 MW are options contingent on milestone-based deposits — a structure that de-risks Fit Energy but leaves FCEL’s revenue visibility thin. That contrasts with Bloom Energy’s $25 billion AI infrastructure partnership, which includes firm commitments and staged milestones. Meanwhile, FuelCell Energy’s trailing EPS stands at -$6.20, and its $225 million loss over the past 12 months underscores the capital intensity of scaling. Yahoo Finance analysts estimate fair value at $8.24 — 64% below current levels — citing ‘unproven commercial scalability’ despite strong technical momentum.

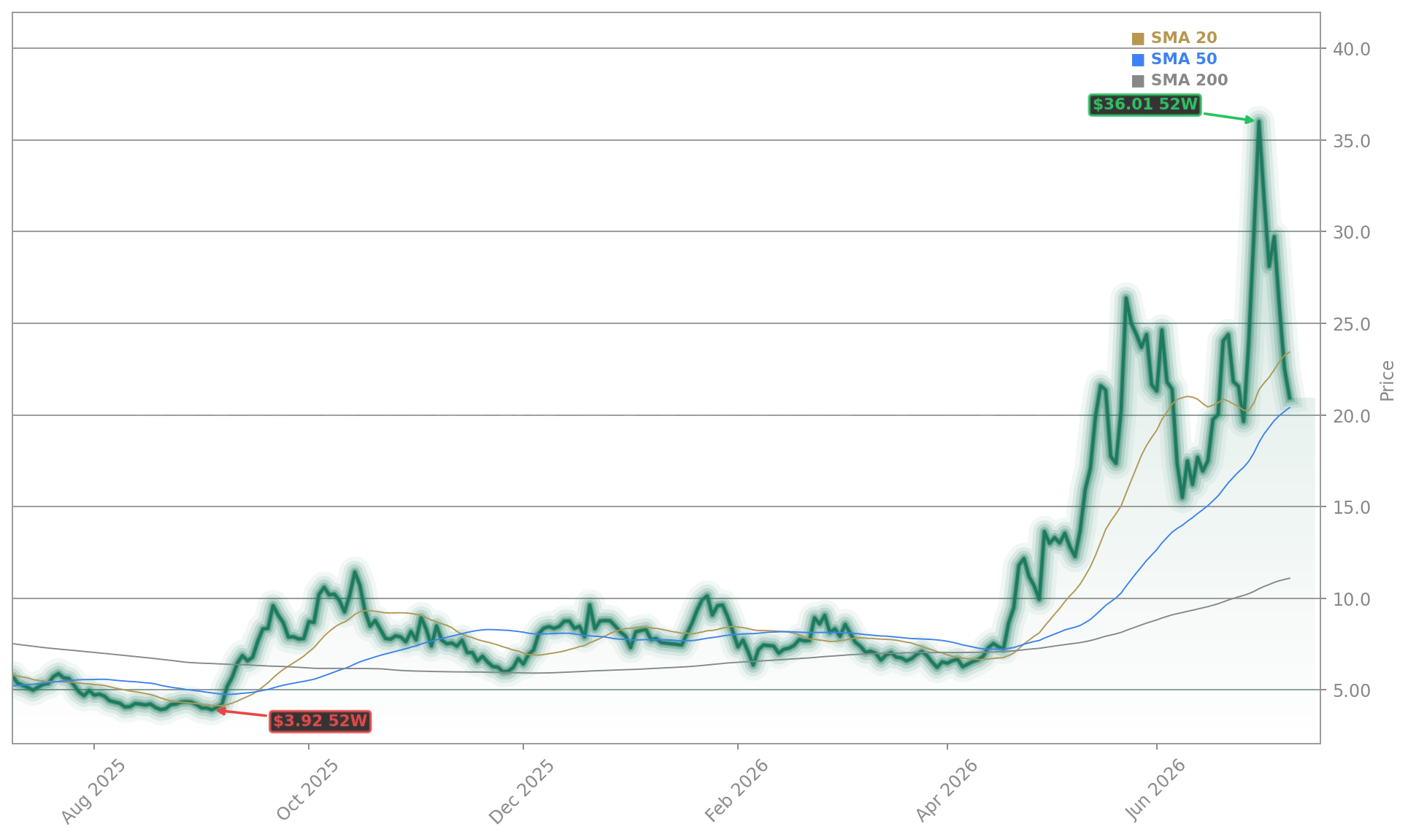

What’s Next for FuelCell Energy’s Technical Setup?

The Siemens collaboration is a validation of our technology’s readiness for commercial scale — but execution, not announcements, will drive the next leg up.— Jason Few, CEO of FuelCell Energy

Friday’s premarket rebound to $23.38 — up 1.65% — suggests short-term stabilization, but the chart tells a more nuanced story. FCEL remains 11.9% above its 50-day SMA ($20.44) and 106.1% above its 200-day SMA ($11.10), preserving its golden cross from October 2025. Yet it now trades 2.8% below its 20-day SMA ($23.53), indicating consolidation after June’s swing high. Key support sits at $18.50 — a level where buyers previously stepped in. A break below that would invalidate the longer-term bullish structure and trigger deeper portfolio rebalancing. For investors, the next catalyst is not another offering — it’s delivery proof: first 30 MW to Fit Energy, first Siemens-integrated project commissioning, and Q3 revenue execution.