Can the Gold Fed Outlook push bullion even higher, or will the next US jobs report finally cool this breakout?

What Does the Gold Fed Outlook Mean for Rates?

The Gold Fed Outlook shifted decisively this week. At the ECB forum in Sintra, Fed Chair Kevin Warsh confirmed inflation risks have “come down” but stopped short of endorsing a pause — a calibrated ambiguity that slashed the probability of a July 29 rate hike to under 30%, per CME FedWatch. That pivot — coupled with falling oil prices and easing geopolitical risk after U.S.-Iran technical talks in Doha — directly lifted gold. Real yields on 10-year TIPS dropped 12 basis points this week, while the U.S. Dollar Index retreated to 101.40. For Wall Street, this means lower opportunity cost for holding non-yielding assets — a structural tailwind for gold through Q3 2026.

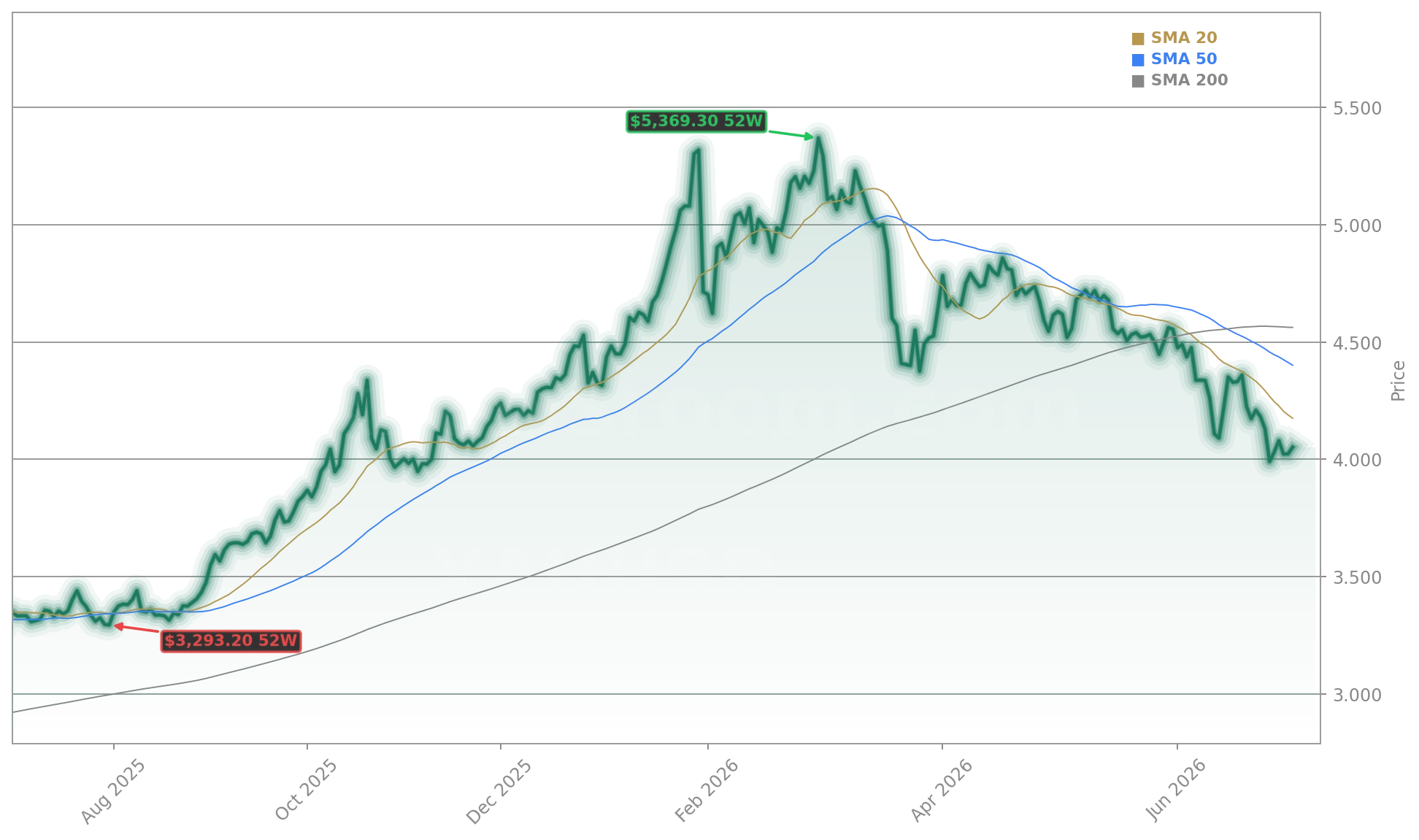

Why Did Gold Break $4,100 Ahead of Jobs Data?

Gold’s $4,120.33 intraday peak wasn’t random — it’s a technical and fundamental inflection point. The ADP report showed just 98,000 private-sector jobs in June — well below the 113,000–118,000 consensus — while Challenger layoffs plunged 53% month-over-month. With the official NFP report due Thursday at 8:30 a.m. ET, traders are pricing in a 4.3% unemployment rate and 110,000–115,000 jobs. A soft print would reinforce the Gold Fed Outlook’s dovish tilt and could trigger a rapid move toward the 200-day moving average near $4,340. Conversely, a strong report may stall momentum — but won’t reverse the trend, per the World Gold Council’s base case of $4,100 ±5% fair value.

How Are Gold Miners Reacting to the Gold Fed Outlook?

Gold equities are outperforming the metal: the NYSE Arca Gold Miners Index (GDX) rose 3.2% this week, led by Barrick Gold and Newmont. Barrick (NYSE: GOLD), which recently settled its Mali dispute and appointed Helen Cai as CFO, benefits from rising margins as gold climbs past $4,100. Newmont, despite reserve-replacement challenges, posted $3.8 billion in Q1 2026 operating cash flow and launched a $6.0 billion share buyback — a direct response to undervaluation amid the Gold Fed Outlook shift. RBC Capital Markets upgraded Newmont to ‘Outperform’ this week, citing “improved capital allocation discipline and near-term catalysts in Nevada.” Meanwhile, junior explorer Lahontan Gold — with its Santa Fe project in Walker Lane — gained 18% this week on drill results confirming 35.0 meters at 0.34 g/t Au Eq and strong environmental progress with the BLM.

Gold Fed Outlook: What’s Driving Institutional Demand?

Central banks are the quiet engine behind gold’s resilience. A recent OMFIF survey found 30% of central banks plan to increase gold reserves in H2 2026 — while reducing dollar holdings. That’s not sentiment; it’s strategy. In Q1 2026, global central bank gold purchases hit 290 tonnes — the second-highest quarterly total on record. Meanwhile, physical demand for bars and coins has eclipsed global jewelry demand for the first time since 2013, per Metals Focus. This structural shift — away from consumption and toward strategic reserve accumulation — makes gold less sensitive to consumer cycles and more aligned with sovereign portfolio rebalancing. For U.S. investors, that means gold is no longer just a hedge — it’s a geopolitical asset class.

Is This Rally Sustainable Beyond July?

The firmer currency backdrop […] is prompting investors to reassess positioning after a volatile few weeks.— Neil Welsh, Head of Metals at Britannia Global Markets

Yes — but with caveats. Commerzbank raised its 2026 year-end gold forecast to $4,800 — citing persistent fiscal deficits, elevated geopolitical risk, and continued central bank buying. The firm maintains its $5,200 target for end-2027. Crucially, gold’s 30-day volatility (26.78%) remains near financial crisis highs — signaling opportunity, not instability. And while the ‘Death Cross’ (50-day below 200-day) still looms, the RSI at 39.4 shows gold is not oversold — just consolidating. With oil below $68, inflation likely peaking near 3.9%, and the Fed’s next move increasingly tied to labor data, the Gold Fed Outlook remains the single most influential variable for gold — and for U.S. portfolios balancing tech concentration and rate risk.