Why are central banks buying gold so aggressively now, and what could that mean for the dollar and investors?

Why Are Central Banks Raising Gold Central Bank Reserves?

Central banks added an average of 1,000 tonnes of gold annually over the past four years — double the pace of the prior decade. The World Gold Council’s 2026 survey, conducted between February 5 and May 19, captures sentiment shaped by the Middle East conflict and persistent inflation uncertainty. A commanding 89% of respondents expect global official gold reserves to rise over the next year — with 45% planning to increase their own holdings, the highest percentage since the survey began in 2011. Only 1% anticipate reducing reserves. This isn’t cyclical demand — it’s a deliberate, long-term recalibration away from overreliance on the US dollar, which 74% of central banks expect to hold a lower share of reserves in five years.

How Are Central Banks Funding Gold Purchases?

Half of respondents plan to fund new gold acquisitions through domestic purchase programs in local currency — a move that strengthens monetary sovereignty and reduces foreign exchange exposure. Another 38% intend to sell existing reserve assets — primarily US Treasuries and other sovereign bonds — to finance purchases. This signals not just portfolio rebalancing, but active de-dollarization. Vaulting preferences are also evolving: domestic storage rose to 49% (from 44% in 2025), while the Bank of England remains the top third-party vault at 57%. The Swiss National Bank’s share dropped to 6%, reflecting geopolitical recalculations in storage strategy.

What Does This Mean for Gold Miners Like Barrick Mining?

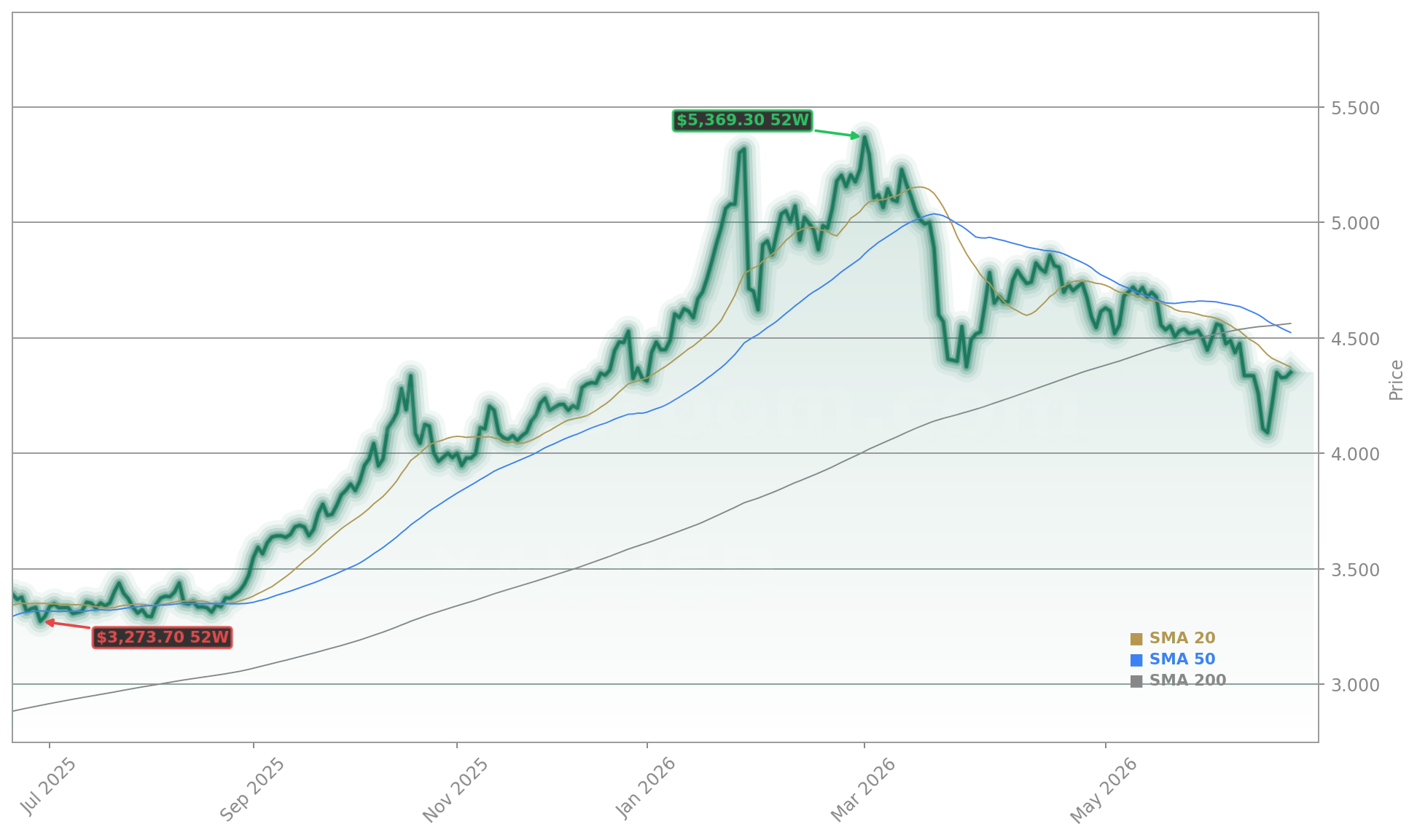

Strong central bank demand is amplifying fundamentals for gold producers. Barrick Mining, Agnico Eagle, and DRC Gold are benefiting from both rising bullion prices and falling input costs — oil’s recent decline has materially lowered mining energy expenses before gold itself rallies. With the World Gold Council reporting 863 tonnes of central bank gold purchases in 2025 alone, margins are expanding even at current $4,327 levels. J.P. Morgan forecasts gold could reach $6,000 per ounce in a full-cycle upswing, while Deutsche Bank echoes that view, citing reserve diversification as a multi-year tailwind. Importantly, this isn’t just an EMDE story: advanced economy central banks share the same outlook — 84% anticipate gold’s share of reserves rising meaningfully in five years.

Is Gold Outperforming Tech Stocks in 2026?

Yes — and the rotation is accelerating. After years of AI-driven euphoria, NVIDIA, Tesla, and Apple face mounting pressure from stretched valuations, slowing earnings growth, and fading KI-driven revenue catalysts. Meanwhile, gold has surged 18% year-to-date on Wall Street, outpacing the S&P 500 and NASDAQ. Analysts at Citigroup highlight gold’s role as a ‘geopolitical hedge with yield-like stability’ in volatile markets, while RBC Capital Markets upgraded gold mining equities to ‘Overweight’, citing improved free cash flow visibility and underappreciated US-based assets like those in Nevada. Lahontan Gold — trading at just 134 million CAD — exemplifies the opportunity: low valuation, US jurisdiction, and exposure to rising gold prices. With tech’s KI hype fading and gold’s institutional demand hitting record highs, investors are reallocating capital toward tangible, uncorrelated assets.

Gold Central Bank Reserves: What’s Next for Investors?

Gold remains the ultimate strategic asset — not just for crisis insurance, but for long-term reserve diversification in an era of fragmented monetary systems.— Juan Carlos Artigas, Head of Research, World Gold Council

Gold Central Bank Reserves are no longer a defensive footnote — they’re a primary driver of price, liquidity, and sector performance. The convergence of record central bank buying, declining USD dominance, falling energy costs for miners, and a broad-based rotation out of tech creates a powerful multi-year catalyst. Morgan Stanley notes that gold’s correlation with US Treasury yields has weakened significantly since 2024, signaling a new regime where gold trades more on reserve demand than just inflation or rate expectations. For portfolios exposed to NASDAQ volatility, adding exposure to gold miners — particularly those with US assets and low-cost production — offers asymmetric upside. The next catalyst? The Federal Reserve’s July FOMC meeting — with markets pricing in a 72% chance of a September rate cut, gold’s appeal as a non-yielding asset is set to intensify.