Is Marvell Technology’s record insider selling a red flag for its AI-fueled rally or just profit-taking at the top?

Is Marvell Technology Insider Selling a warning sign?

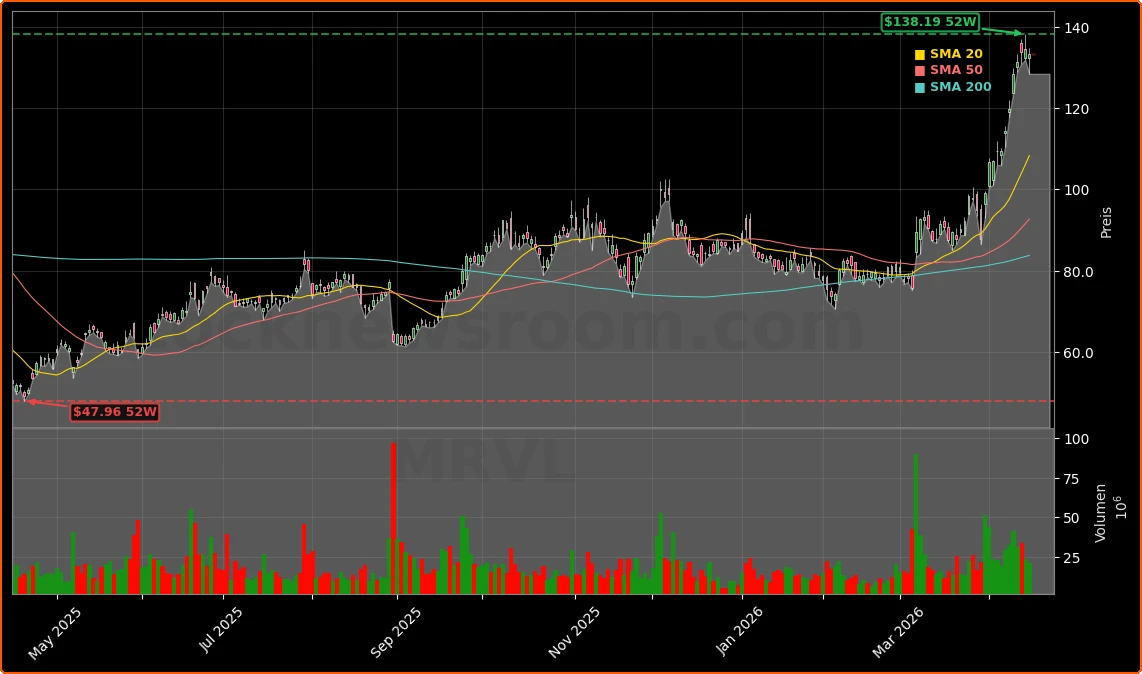

Shares of Marvell Technology, Inc. were recently quoted at $133.37, down 0.91% from the prior NASDAQ close of $132.75, with pre-market indications around $132.98 as of early Friday ET. The stock remains just below its 52-week high of $138.18 and has rallied roughly 149% over the past year, firmly positioning MRVL among the standout AI beneficiaries on the NASDAQ and within the broader S&P 500 technology universe.

Against that backdrop, Marvell Technology Insider Selling has accelerated. Sandeep Bharathi, head of the company’s data center segment, sold 66,892 shares on April 16 at an average price of $130.35, generating proceeds of about $8.7 million. Filings show the sale was executed under a pre-arranged Rule 10b5-1 trading plan and followed the vesting of over 141,000 shares, with part of the position surrendered back to the company to cover tax obligations. After the transaction, Bharathi still holds 55,199 shares directly.

The same week, Chief Financial Officer Willem A. Meintjes sold 30,000 shares on April 15 at an average of $134.01, raising just over $4.0 million. Here, too, the sale was made under a 10b5-1 plan, immediately after nearly 131,000 shares vested and a significant portion was surrendered for tax purposes. Meintjes remains a major shareholder with 230,675 shares. The pattern underscores that Marvell Technology Insider Selling is happening from a position of strength, not from executives abandoning their stakes.

How strong is Marvell Technology’s AI growth story?

Fundamentally, the AI narrative around Marvell remains intact. In the most recent reported quarter, revenue climbed 37% year over year to just under $2.1 billion. The data center business, which includes custom accelerators and high-speed connectivity solutions for AI workloads, now accounts for approximately 73% of total company revenue. That concentration makes MRVL highly levered to the same infrastructure trends that have powered names like NVIDIA and, on the systems side, large cloud platforms run by Apple’s fellow mega-cap peers.

Management is guiding for more than 40% revenue growth in the fiscal year 2026, a target that assumes continued ramp-up of custom AI chip programs and integration of the recently acquired Celestial AI. The Celestial deal is aimed at strengthening Marvell’s position in optical interconnects, a critical technology for scaling out large AI clusters and managing bandwidth and power challenges inside hyperscale data centers. The company is currently working on more than 50 active AI chip design projects for 10 major customers, including cloud heavyweights such as Microsoft and Amazon, positioning Marvell as a key enabler of next-generation infrastructure even as other AI beneficiaries like Tesla focus more on in-house compute for autonomous driving.

For US-based investors building AI baskets alongside names like NVIDIA and leading cloud operators, MRVL offers a more infrastructure-centric angle. That context is important when weighing Marvell Technology Insider Selling: the transactions are happening in the middle of a long-term capex cycle in which hyperscalers are still early in deploying AI-centric architectures at scale.

What are Wall Street analysts saying about Marvell Technology?

The latest analyst commentary has largely brushed aside the insider activity. Stifel recently raised its price target on Marvell from $120 to $140 per share while reiterating a “Buy” rating, calling the latest volatility in AI chip stocks a buying opportunity for long-term investors. Stifel’s analysts point to Marvell’s differentiated capabilities in custom silicon and optical connectivity, along with the depth of its AI design pipeline, as key reasons the stock could continue to re-rate higher.

This stance keeps MRVL firmly in the camp of favored AI infrastructure plays alongside the mega-cap leaders. While Marvell does not yet match the scale or margins of giants like Apple or NVIDIA, the company’s revenue mix and guidance suggest it could grow faster from a smaller base. From a valuation perspective, investors must now weigh the implied upside from Stifel’s $140 target against the reality that senior management is monetizing part of its equity just below that level.

For portfolio managers, the key question is whether Marvell Technology Insider Selling signals management caution about near-term upside or simply reflects sensible diversification after a steep run-up. The fact that the trades were executed under 10b5-1 plans, following substantial vesting events and leaving executives with sizable remaining holdings, tilts the interpretation toward planned profit-taking rather than a negative read on fundamentals.

How should investors react to Marvell Technology Insider Selling?

Short term, the concentration of insider sales near the recent high may act as a psychological ceiling and add to volatility around the next earnings report in June 2026, when investors will seek more detail on AI chip volume ramp and Celestial AI integration. If execution remains strong and data center demand holds up, institutional buyers may view any pullbacks tied to Marvell Technology Insider Selling as a chance to add exposure to a high-growth infrastructure name within the S&P 500 technology cohort.

Longer term, the main risk is that AI infrastructure spending proves more cyclical than expected or that hyperscalers increase reliance on fully internal designs, compressing Marvell’s addressable market. On the other hand, if AI workloads keep scaling and bandwidth bottlenecks worsen, Marvell’s optical and custom-silicon portfolio could become even more strategic.

Related Coverage: For a deeper look at how analyst upgrades have already fueled the stock’s move, including the impact of a recent Barclays call, investors can read this detailed breakdown of Marvell Technology’s Barclays-driven AI re-rating. To put sector-wide sentiment in context and compare valuation dynamics across high-growth tech, it is also worth reviewing how cybersecurity peer Zscaler is being treated after its own surge in results in this analysis of Zscaler’s earnings spike and valuation debate.

In the end, Marvell Technology Insider Selling highlights the tension between an overheated share price and a still-compelling AI growth story. For investors, the transactions look more like opportunistic profit-taking than a collapse in confidence, but they do raise the bar for future execution. The next quarterly update will be crucial in determining whether MRVL can justify its premium multiples and keep rewarding shareholders who choose to look past the recent insider activity.