Can MicroStrategy Bitcoin Strategy still work if the company starts treating its Bitcoin pile less like a shrine and more like a funding tool?

What Does Bitcoin Monetization Mean for MSTR?

MicroStrategy Incorporated’s June 29 announcement marks a structural departure from its decade-long ‘buy and hold forever’ doctrine. Under the new framework, the company may sell Bitcoin to fund a U.S. dollar reserve, cover STRC preferred dividend obligations (now raised to 12%), repurchase common stock or digital credit securities, and service interest expenses. While management insists Bitcoin remains its ‘primary treasury reserve asset,’ the shift transforms MicroStrategy from a passive holder into an active treasury manager — a distinction that matters profoundly for investors using MSTR as a pure Bitcoin beta vehicle. Notably, the $2 billion repurchase authorization applies across both STRC and class A common shares, signaling liquidity support that could mute volatility — but only if execution matches intent.

How Does This Compare to Bitcoin Miners Like Riot and Marathon?

Unlike publicly traded Bitcoin miners such as Riot Platforms or Marathon Digital, MicroStrategy Incorporated generates no operating revenue from mining infrastructure, energy arbitrage, or hash rate deployment. Its entire valuation rests on Bitcoin’s price action and accounting treatment under ASC 820 fair-value rules. That divergence explains why the CoinShares Valkyrie Bitcoin Miners ETF (WGMI), up 47.6% year-to-date through July 6, 2026, explicitly excludes MSTR — not for size, but by mandate. As Barron’s recently noted, WGMI’s performance underscores how operational leverage (mining margins, power cost efficiency) can decouple from pure treasury exposure. For U.S. investors seeking crypto-equity exposure, this forces a choice: operational upside or treasury leverage — not both.

Is MicroStrategy Bitcoin Strategy Still a Viable S&P 500 Proxy?

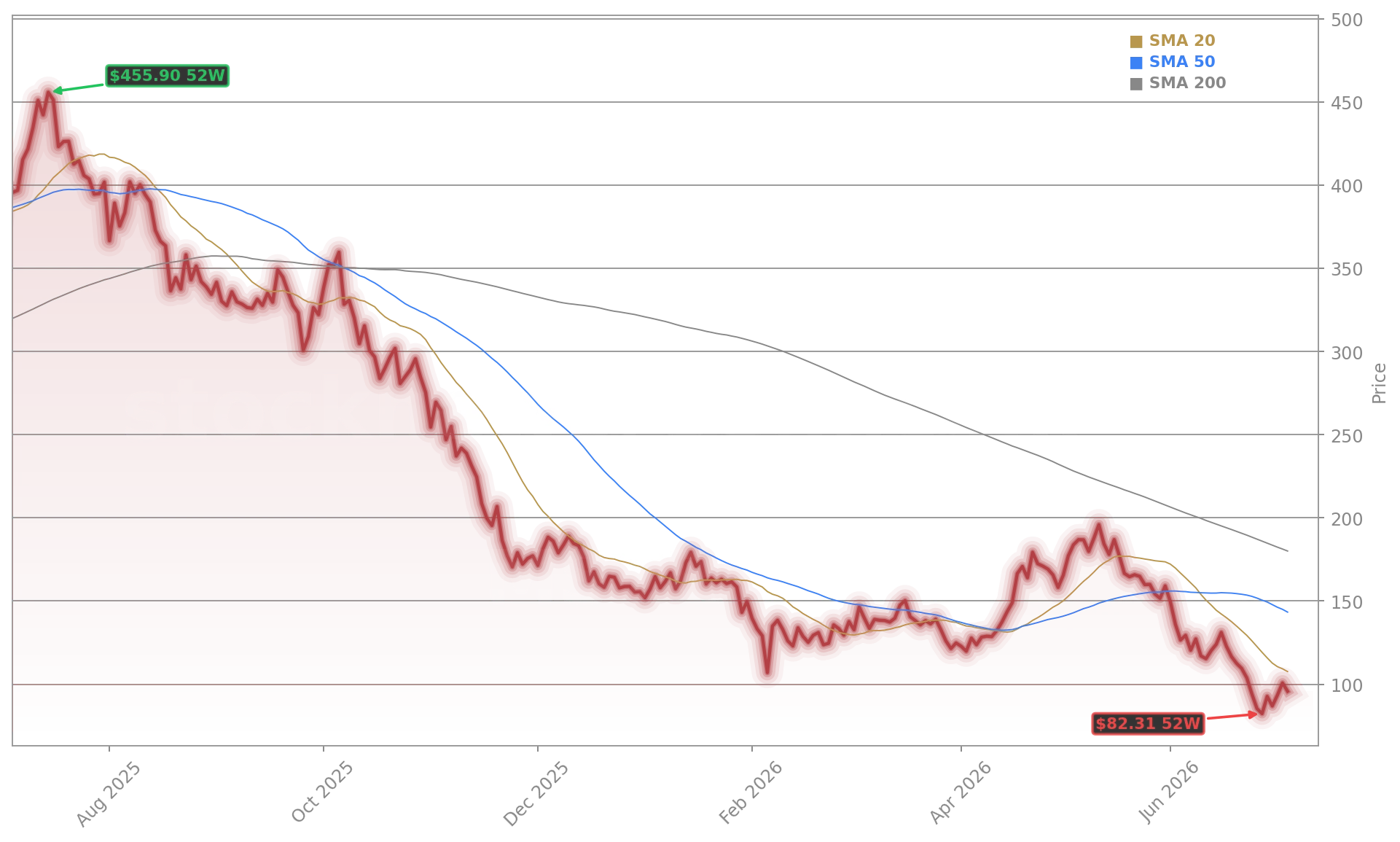

With MSTR down 33.7% year-to-date and trading at $95.92 — 4.8% lower than Monday’s close — the stock’s correlation to Bitcoin has weakened amid mounting liquidity concerns. While Bitcoin itself is down 28% in 2026, MSTR’s 75% one-year plunge reflects compounding pressures: $7.37 billion in Q1 2026 ATM equity offerings, STRC yield compression, and rising scrutiny from the Rosen Law Firm over disclosures. Analysts remain divided: Benchmark Equity Research reiterated its ‘Buy’ rating, citing improved capital discipline, while Citigroup downgraded MSTR to ‘Neutral’ with a $82 price target, warning that monetization ‘erodes the very scarcity narrative that underpins its premium.’ For NASDAQ-listed tech portfolios, MSTR no longer behaves like a high-beta software stock — it trades more like a structured credit instrument backed by BTC.

What’s Next for MicroStrategy Bitcoin Strategy?

This is not a retreat from Bitcoin — it’s the evolution of our treasury strategy into a dynamic, shareholder-first capital engine.— Michael Saylor, Executive Chairman, MicroStrategy Incorporated

With 818,334 BTC still on its balance sheet — acquired at an average cost near $75,500 — MicroStrategy Incorporated retains immense optionality. But the company’s ability to execute its new monetization program hinges on two near-term variables: Bitcoin’s price stability above $55,000 (critical for avoiding margin calls on STRC collateral) and investor confidence in its $1.2 billion annual STRC dividend obligation. If Bitcoin rebounds sharply in Q3 2026, MSTR could rally on buyback execution and reduced dilution pressure. If not, the monetization program risks becoming a liquidity drain rather than a stabilizer. As RBC Capital Markets observed in its July 3 note, ‘The framework is sound — but credibility is now collateral.’ Wall Street will watch Q3 disclosures closely for actual BTC sales volume and USD reserve accumulation, not just policy announcements.