Can MicroStrategy’s new capital play protect its Bitcoin machine without undermining the very leverage that made MSTR famous?

What triggered MicroStrategy’s capital strategy shift?

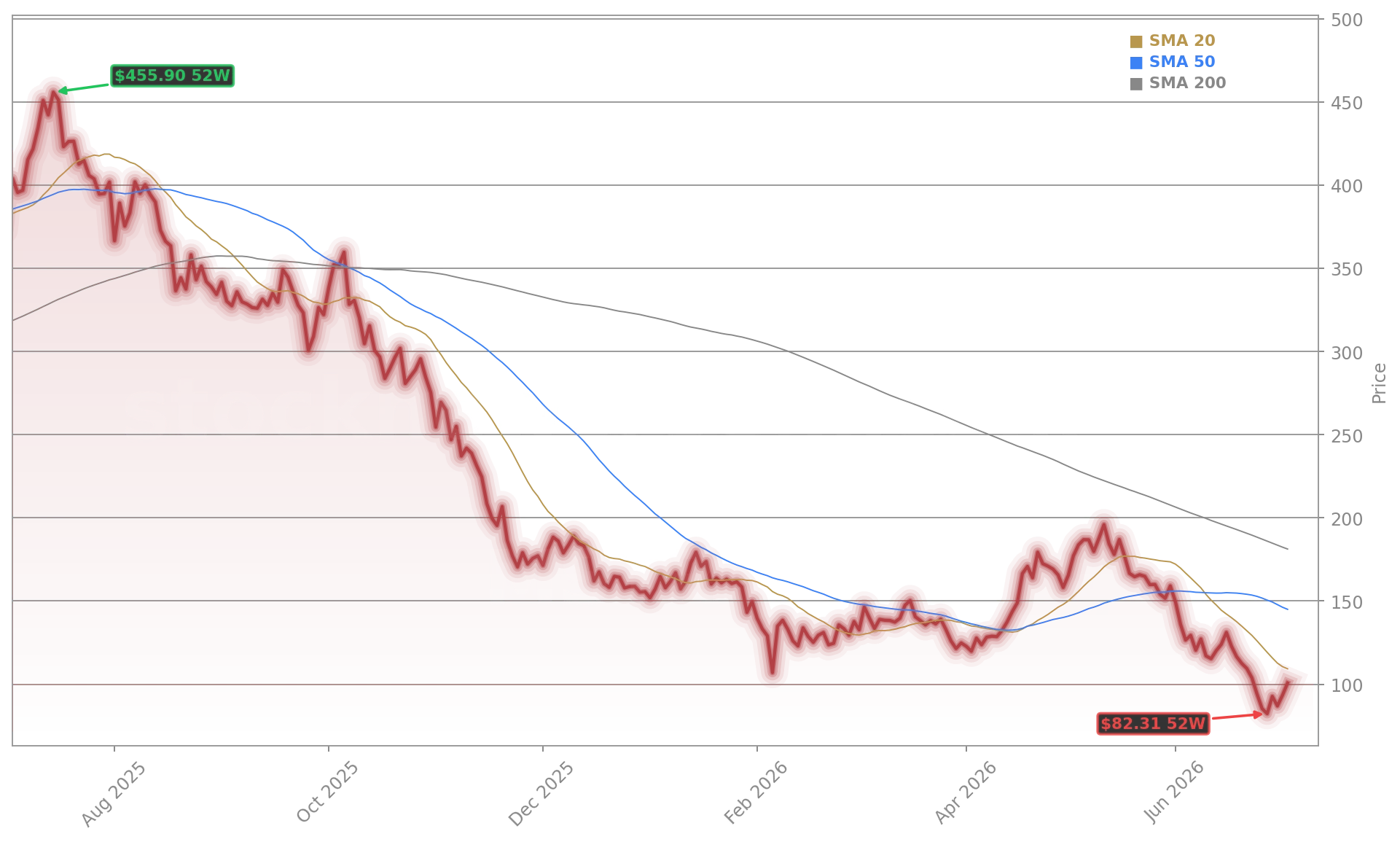

STRC preferred stock — MicroStrategy Incorporated’s primary vehicle for funding Bitcoin purchases — plunged to $71.25 on June 26, its lowest level ever and nearly 30% below par. That collapse threatened the company’s ability to raise low-cost capital for new Bitcoin acquisitions. In response, CEO Phong Le’s revocable trust purchased 11,000 shares of STRC at $90.80 on June 22, while Executive Vice President Thomas Chow bought both STRC and STRK shares days earlier. The insider activity signaled confidence in the new framework, which includes a minimum 12-month cash reserve covering preferred dividends and interest — currently covering 17 months with $2.55 billion on hand.

How does the new MicroStrategy Capital Strategy work?

The newly announced Digital Credit Capital Framework introduces three pillars: (1) a $1.25 billion Bitcoin monetization program to fund dividends, repurchases, and reserves; (2) $2 billion in authorized repurchases across STRC, STRK, and MSTR common stock; and (3) a USD reserve policy with strict liquidity thresholds. Crucially, the framework allows MicroStrategy Incorporated to sell Bitcoin *only as needed* — not as a strategic reversal. As Bitwise CIO Matt Hougan noted, this is not a retreat from Bitcoin but a maturation of its MicroStrategy Capital Strategy, transforming the firm from a passive treasury vehicle into a flexible, balance-sheet-aware participant. Citigroup’s Peter Christiansen added that the plan ‘buys more time’ for the company until Bitcoin’s price stabilizes — a key catalyst for STRC’s recovery.

Why are Wall Street analysts divided?

While Benchmark Equity Research reiterated its ‘Buy’ rating — calling the framework ‘a positive for shareholders by transforming the company into an active manager of its balance sheet’ — JPMorgan warned the Bitcoin monetization program introduces ‘two-way risk’ that could amplify crypto market volatility. That tension reflects broader uncertainty about how much institutional investors are willing to absorb from a single corporate buyer. Notably, Bitwise expects institutional capital — not MicroStrategy Incorporated — to become Bitcoin’s dominant demand source in the next cycle, reducing MSTR’s outsized influence. Meanwhile, the Rosen Law Firm has launched a securities probe, alleging misleading disclosures around the company’s capital structure — though analysts caution such investigations are common in high-volatility sectors and do not imply guilt.

What does this mean for U.S. portfolios?

MicroStrategy Incorporated remains a top crypto-beta stock on the NASDAQ — more volatile than Tesla or Apple and far more sensitive to Bitcoin’s price action than traditional tech peers like NVIDIA. Its 20% weekly gain — rebounding from $80 to $100.78 — coincides with Bitcoin stabilizing near $61,400 and STRC recovering to $88. Yet the stock’s sensitivity remains extreme: a 5% Bitcoin move can trigger a 12–15% swing in MSTR. For S&P 500 investors, MSTR’s volatility now acts as a transmission line for crypto sentiment — especially as ETF outflows and Fed rate uncertainty weigh on digital assets. The new MicroStrategy Capital Strategy doesn’t eliminate that sensitivity — it institutionalizes it with guardrails, making MSTR less binary and more analyzable for long-term U.S. portfolios.

Related Coverage: Has MicroStrategy finally found a way to tame its Bitcoin risk without breaking the very thesis that made it famous? MicroStrategy Bitcoin Sale +11.8% as Wall Street Reassesses. Meanwhile, Ethereum’s 5.1% surge suggests growing decoupling from Bitcoin — a trend that could reshape how investors allocate across digital asset proxies: Ethereum Market Analysis +5.1%: ETH Shows Resilience.

The volatility in STRC is a natural and important part of the crypto cycle. I think we’re nearing the bottom.— Matt Hougan, Bitwise CIO

MicroStrategy Incorporated’s MicroStrategy Capital Strategy marks a critical inflection point — not just for the company, but for how Wall Street prices crypto-linked equities. It replaces rigid dogma with adaptive discipline, turning balance sheet management into a competitive advantage. For U.S. investors, this means MSTR is no longer just a Bitcoin lever — it’s a test case for corporate capital agility in volatile digital markets. The next quarterly earnings will show whether the framework delivers measurable margin improvement and reduced earnings volatility.